What is Commercial General Liability (CGL) Insurance?

Commercial General Liability (CGL) insurance is the foundational liability policy for any business operating in India. It protects your company from financial losses arising from third-party claims of bodily injury, property damage, and advertising or personal injury caused by your business operations, products, or employees. When a customer slips at your premises, a contractor damages a client's property, or a competitor sues you for defamation in an advertisement — CGL steps in to cover legal defence costs, compensation, and court awards.

In India, CGL is often confused with Public Liability Insurance. While Public Liability (covered under the Public Liability Insurance Act, 1991) is a narrower, statutory requirement for hazardous industries, CGL is a broader, voluntary commercial policy available across all sectors. An IRDAI-compliant CGL policy provides three-section coverage: Bodily Injury and Property Damage Liability (Section I), Personal and Advertising Injury Liability (Section II), and Medical Payments (Section III).

Without CGL, a single significant liability claim — a customer hospitalised after a fall at your store, or a manufacturing defect that damages a client's equipment — can expose your business to crores of rupees in uninsured losses. For most Indian businesses, CGL is not just prudent risk management. It is a prerequisite for tendering, contracting with multinational clients, operating in commercial properties, and securing trade finance.

What Does a CGL Policy Cover?

A standard CGL policy covers four main areas, which together address the most common liability exposures that Indian businesses face in their day-to-day operations.

Bodily Injury Liability (BIL) covers claims when a third party — a customer, visitor, delivery person, or passer-by — suffers physical injury due to your business operations or at your premises. The policy pays for the claimant's medical treatment, hospitalisation, rehabilitation, and any compensation awarded by a court. In India, slip-and-fall cases in retail stores, food poisoning claims in restaurants, and visitor injuries at construction sites are the most common bodily injury claims under CGL policies.

Property Damage Liability (PDL) covers claims when your business operations or employees cause damage to third-party property. A plumbing contractor who accidentally causes a flood at a client's building, an IT company whose technician damages a client's server room, or a logistics company whose warehouse fire spreads to an adjacent facility — all are covered under PDL. The policy pays for the cost of repair, replacement, or loss of use of the damaged property.

Personal and Advertising Injury Liability covers non-physical injury claims, including defamation (libel and slander), copyright infringement, false arrest, malicious prosecution, and wrongful eviction arising from your advertising, publications, or business conduct. In India's growing digital marketing and e-commerce environment, advertising liability claims — particularly relating to social media content, comparative advertising, and influencer campaigns — are an increasingly significant exposure for consumer brands.

Medical Payments is a no-fault coverage that pays immediate medical expenses for third parties injured on your premises, regardless of whether your business is legally liable. The purpose is to provide quick, goodwill-based medical assistance to injured parties without waiting for legal determination of fault — which often prevents minor incidents from escalating into full liability lawsuits. This section is especially valuable for retail outlets, hospitality businesses, and educational institutions in India.

What is NOT Covered by CGL?

Understanding CGL exclusions is as important as understanding what is covered. Standard CGL policies in India exclude the following:

Professional liability — errors or omissions arising from professional services (e.g., an architect's design fault, a doctor's medical negligence, a CA's accounting error) are not covered. These require a separate Professional Indemnity (PI) or Medical Malpractice policy.

Employer's liability / workmen's compensation — injuries to your own employees are excluded from CGL. These are covered under a Workmen's Compensation (WC) or Employer's Liability policy.

Own property damage — CGL only covers damage to third-party property. Damage to your own building, machinery, or stock is covered under a Property All Risk (PAR) or Industrial All Risk (IAR) policy.

Intentional acts — deliberate or wilful acts causing injury or damage are excluded from CGL coverage globally.

Contractual liability — liability assumed under a contract that exceeds your statutory liability is generally excluded unless specifically endorsed.

Pollution liability — gradual or sudden pollution events require a separate Environmental Liability policy in India.

Cyber liability — data breaches, ransomware events, and cyber-related business interruption require a standalone Cyber Insurance policy.

Which Indian Businesses Need CGL Insurance?

The short answer: any business that interacts with the public, occupies premises, or produces goods needs CGL insurance. The risk profile and appropriate cover limits vary by sector, but the fundamental need for liability protection is universal.

Manufacturing companies face product liability risk whenever their products reach end consumers. A consumer goods company whose product causes injury, or an auto parts manufacturer whose component failure causes an accident, faces potentially enormous third-party claims. CGL — often supplemented by a standalone Product Liability policy — is the minimum risk management requirement for any manufacturing enterprise in India.

Retail and hospitality businesses — malls, restaurants, hotels, supermarkets, and entertainment venues — face constant slip-and-fall, food poisoning, and premises liability exposure. In India, with rising consumer awareness and increasing use of consumer courts, liability claims against retail and hospitality businesses have grown significantly over the last decade. Major mall operators and hotel chains now mandate CGL as a standard lease requirement for their tenants and vendors.

IT and technology companies based in Bengaluru, Hyderabad, Pune, and Chennai regularly visit client premises and operate in co-working or client-provided facilities where third-party injury or property damage is a real risk. Beyond physical risks, technology companies in product and advertising roles face advertising liability exposure from content and marketing activities. Most multinational IT clients in India require their Indian vendors to maintain CGL coverage as a contract condition.

Construction and contracting firms face the broadest range of liability exposures: site accidents injuring sub-contractors (who may be treated as third parties), damage to adjacent structures during demolition or piling, and public injury from construction activity in occupied urban areas. In India, RERA-registered developers and infrastructure contractors tendering for government contracts are increasingly required to demonstrate CGL coverage.

Aviation and UAM operators — airlines, air taxi companies, drone operators, MRO facilities, and FBOs — face unique and potentially catastrophic liability exposures. Third-party bodily injury from aviation incidents, property damage from UAV operations, and ground handling accidents all fall within the CGL framework, typically supplemented by aviation-specific liability extensions. TropoGo specialises in liability insurance for India's emerging aviation and urban air mobility sector.

How Much CGL Coverage Does Your Business Need?

CGL policy limits in India are structured as per-occurrence limits (maximum payout for any single claim) and aggregate limits (maximum payout across all claims in a policy year). The appropriate coverage level depends on your business sector, revenue, client contractual requirements, and the severity of potential claims. As a general guide for Indian businesses:

Small businesses (turnover below ₹5 crore): ₹1–5 crore per occurrence / ₹2–10 crore aggregate is typically adequate.

Mid-size companies (₹5–50 crore turnover): ₹5–25 crore per occurrence / ₹10–50 crore aggregate, depending on sector.

Large enterprises (₹50 crore+ turnover, or with multinational clients): ₹25 crore+ per occurrence is common; some global client contracts specify USD 1–5 million limits.

Aviation and high-risk sectors: limits are typically set at USD 10–50 million per occurrence, aligned with DGCA requirements and IATA standards.

Premiums for CGL coverage in India typically range from 0.05% to 0.5% of the insured limit, depending on the business sector, claims history, turnover, and specific risk factors. A small IT company might pay ₹15,000–30,000 per year for ₹2 crore of CGL coverage. A mid-size manufacturer with ₹10 crore of coverage might pay ₹1–2 lakh annually.

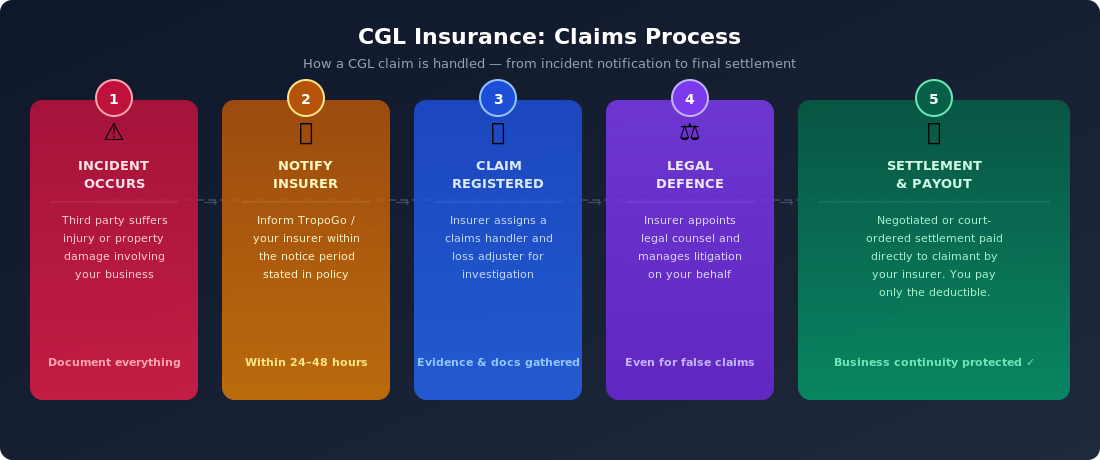

How the CGL Claims Process Works in India

Understanding how a CGL claim flows from incident to settlement helps business owners appreciate the true value of the policy — which lies not just in the eventual payout, but in the legal defence and claims management that your insurer provides throughout the process.

When an incident occurs, the first priority is documentation: preserve CCTV footage, photograph the scene, collect witness statements, and retain any incident reports. Within 24–48 hours, notify your insurer (or TropoGo as your broker). The insurer registers the claim, assigns a claims handler, and — if the claim is significant — appoints a loss adjuster to investigate.

If the claimant files a lawsuit, your insurer appoints legal counsel and manages the litigation entirely on your behalf. This is one of the most valuable aspects of CGL coverage: your business can continue operating normally while the insurer's legal team handles the case. If the claim is settled — either through negotiation or court order — the insurer pays the compensation directly to the claimant, up to your policy limit. You are responsible only for the deductible (typically ₹25,000–2 lakh depending on the policy terms).

IRDAI mandates that General Insurance companies in India acknowledge claims within 15 days and make claim decisions within 30 days of receiving all required documentation, though complex liability cases involving court proceedings typically take longer to reach final settlement.

CGL vs. Other Liability Policies: Building Your Coverage Stack

CGL is the foundation of a commercial liability programme, but it is not the only liability cover most Indian businesses need. A well-structured liability insurance programme typically layers CGL with complementary policies:

CGL + Professional Indemnity (PI): Essential for IT companies, management consultants, architects, and financial advisors. CGL covers physical risks; PI covers financial loss from professional errors.

CGL + Product Liability: Required for manufacturers and importers whose products reach end consumers. Product Liability extends CGL's product coverage to include product recall costs and broader consumer claims.

CGL + Directors and Officers (D&O): Recommended for listed companies and PE-backed firms. D&O covers personal liability of board members; CGL covers the entity's operational liability.

CGL + Cyber Liability: Increasingly important for tech companies, fintechs, and e-commerce businesses handling customer data. Cyber coverage addresses data breach costs that CGL explicitly excludes.

CGL + Umbrella / Excess Liability: For large corporates and aviation operators, an Umbrella policy provides additional limits above the CGL policy for catastrophic claims exceeding underlying limits.

Why CGL is Non-Negotiable for India's Growing Businesses

India's legal landscape for commercial liability is evolving rapidly. Consumer protection under the Consumer Protection Act, 2019 has significantly expanded the rights of consumers to seek compensation for defective products and services. The Competition Act and SEBI regulations have increased corporate liability exposure for Indian businesses. And as Indian companies scale — taking on institutional clients, listing on exchanges, and entering international markets — the liability risks they face grow proportionally.

A ₹5 crore liability claim — not uncommon in today's environment — can be existential for a small or mid-size Indian business without CGL coverage. Legal defence costs alone in a complex liability case can exceed ₹50 lakh. With CGL, your insurer absorbs these costs and provides expert legal management, allowing your business to continue operating and growing while the claim is resolved.

TropoGo offers CGL policies for Indian businesses across manufacturing, IT, retail, construction, aviation, logistics, and professional services sectors. Our CGL products include the following key specialist covers:

Premises and Operations liability — covering third-party injury and property damage arising from your business premises and day-to-day operations.

Products and Completed Operations — extending CGL coverage to claims arising from products you have manufactured, sold, or supplied after they have left your premises.

Personal and Advertising Injury — protecting against defamation, copyright infringement, and false advertising claims arising from your marketing and communications activities.

Medical Payments — no-fault coverage for immediate medical expenses of third parties injured on your premises or by your operations.

Aviation Ground Liability — specialist CGL extension for airlines, air taxi operators, MRO facilities, and airports covering third-party bodily injury and property damage on the ground.

Contractual Liability endorsement — covering liability assumed under contracts with clients or landlords, making TropoGo's CGL usable for vendor agreements with multinational clients.

The Bottom Line

A single third-party liability claim — a visitor injured at your premises, a product that causes property damage, a defamatory social media post — can cost your business more than years of CGL premiums. Commercial General Liability insurance is not a regulatory formality or a box-ticking exercise. It is the financial backbone that allows Indian businesses to take on clients, scale operations, and compete without the existential risk of an uninsured liability claim.

Whether you are a Bengaluru startup, a Mumbai manufacturer, a Chennai logistics company, or a Hyderabad IT services firm, TropoGo's CGL specialists can design the right coverage structure for your business risk profile. Get a quote today and protect the business you have built.

Is Your Business Shielded Against Liability Claims?

TropoGo designs CGL insurance for Indian businesses across all sectors — from IT firms and manufacturers to airlines and construction companies.

CGL is not mandated by law for most businesses in India — unlike motor insurance or workmen's compensation. However, it is effectively mandatory for companies that contract with multinational clients, occupy commercial leases in Grade-A properties, tender for government infrastructure projects, or operate in regulated sectors like aviation (where DGCA requires third-party liability coverage). Most large corporates treat CGL as a minimum enterprise risk management requirement regardless of regulatory compulsion.

What is the difference between CGL and Public Liability Insurance in India?

Public Liability Insurance (PLI) under the Public Liability Insurance Act, 1991 is a statutory requirement specifically for businesses handling hazardous substances — factories, chemical plants, and industries listed under the Environment Protection Act. CGL is a broader voluntary commercial policy covering bodily injury, property damage, and advertising liability for any type of business. CGL includes all PLI coverages and significantly more, making it the preferred choice for businesses that need more comprehensive protection than the statutory PLI minimum.

Does CGL cover my employees if they are injured at work?

No. CGL explicitly excludes injury to your own employees. Employee injuries at the workplace are covered under a Workmen's Compensation (WC) or Employer's Liability policy, which is mandatory under the Employees' Compensation Act, 1923 for businesses employing workers in scheduled industries. For a comprehensive liability programme, businesses need both CGL (for third-party claims) and WC/EL (for employee claims).

How much does CGL insurance cost for a small business in India?

CGL premiums in India typically range from 0.05% to 0.5% of the insured limit, depending on sector, turnover, claims history, and risk profile. A small IT or services business seeking ₹2 crore coverage might pay ₹15,000–30,000 annually. A mid-size manufacturer seeking ₹10 crore coverage might pay ₹1–2 lakh per year. Premiums are significantly lower for low-risk sectors (professional services, education) and higher for high-risk sectors (construction, chemical manufacturing, aviation).

Does CGL cover product liability for manufacturers in India?

Standard CGL policies include a Products and Completed Operations section that covers claims arising from products you have manufactured or sold after they leave your premises. However, for manufacturers with significant product distribution — particularly in pharmaceuticals, FMCG, automotive components, and consumer electronics — a standalone Product Liability policy with broader limits and specific product recall coverage is often recommended in addition to CGL.

How do I get a CGL insurance quote for my business in India?

TropoGo specialises in commercial liability insurance for Indian businesses across all sectors. Our specialists can assess your liability exposure, recommend appropriate coverage limits, and source competitive CGL quotes from IRDAI-licensed general insurers. Visit our CGL insurance page to learn more and speak with a liability specialist.

Whether you are protecting a small retail outlet or a multi-city construction operation, CGL insurance is the cornerstone of sound commercial risk management in India. Do not wait for the first liability claim to discover your exposure — get a CGL quote today and give your business the protection it deserves.