Parametric insurance — also called index-based insurance — is a type of coverage that pays out a pre-agreed sum automatically when a specific, measurable event (the "trigger") occurs, regardless of actual loss suffered. Unlike traditional indemnity insurance, which requires loss assessment, surveyor visits, and lengthy documentation, parametric insurance uses objective data — rainfall levels, wind speed, seismic magnitude, satellite imagery — to determine whether a claim is due.

The concept is simple: you and the insurer agree upfront on (a) the index to be measured, (b) the threshold that constitutes a trigger, and (c) the payout amount. If the index breaches the threshold, payment is made — automatically, in days.

In India, parametric insurance is gaining rapid traction across agriculture, aviation, marine, energy, and catastrophe risk — driven by IRDAI's push for innovative products and the government's experience with the Pradhan Mantri Fasal Bima Yojana (PMFBY), one of the world's largest parametric crop insurance schemes.

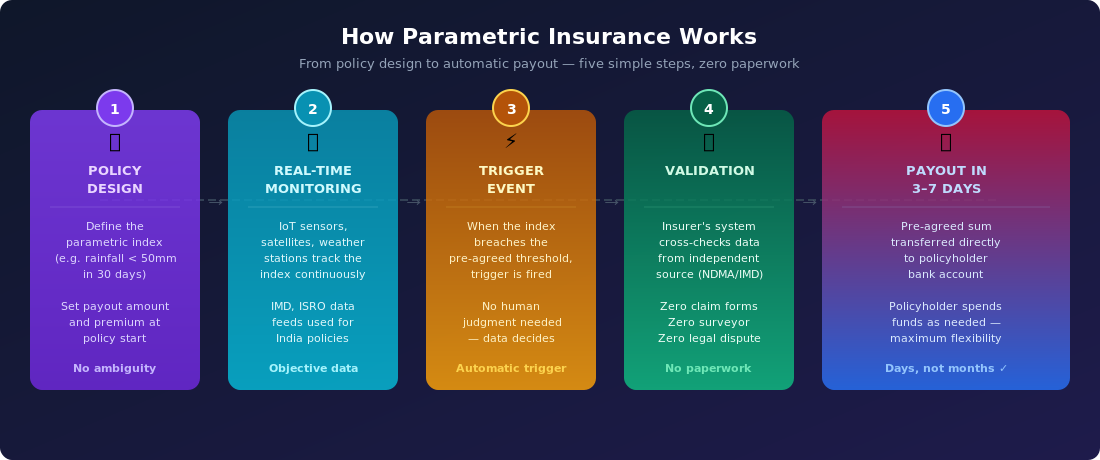

How Parametric Insurance Works

The mechanics of parametric insurance are elegantly straightforward. The entire process — from policy inception to payout — flows through five clear steps with no human subjectivity at any stage.

At Step 1, the policy is designed: the insured and insurer agree on the parametric index (say, cumulative rainfall below 50 mm in a 30-day window), the trigger threshold, and the payout sum. There are no ongoing negotiations about loss extent — everything is settled at inception. At Step 2, real-time data feeds from IMD weather stations, ISRO satellites, or IoT sensors monitor the index throughout the policy period. When the index breaches the agreed threshold (Step 3), the trigger fires automatically. An independent data validation (Step 4) cross-checks the trigger against a third-party source — NDMA, IMD, or the USGS for earthquakes. At Step 5, the pre-agreed sum is transferred directly to the policyholder's bank account within three to seven days.

The policyholder then uses the funds as needed — to replace crop inputs, cover business interruption costs, or manage emergency liquidity. There is no requirement to prove how the money is spent, which gives maximum financial flexibility during a crisis.

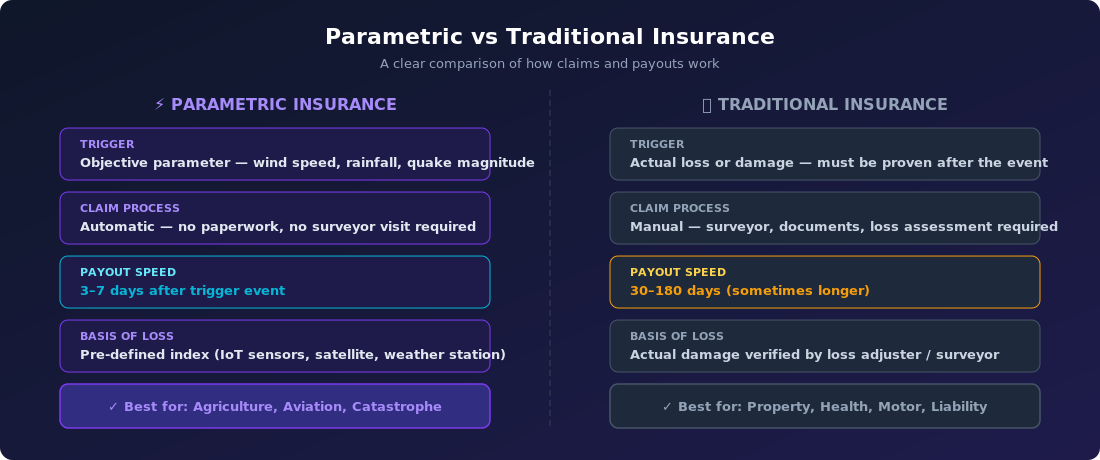

Parametric vs Traditional Insurance

The most important distinction between parametric and traditional indemnity insurance lies in the basis of settlement. Traditional insurance compensates for actual loss — a figure that must be verified by a loss adjuster or surveyor, which takes time, creates disputes, and often results in under-settlement. Parametric insurance compensates based on a pre-defined index — an objective number that cannot be disputed.

This distinction matters enormously in India's context. Traditional agricultural insurance claims can take six to eighteen months to settle — long after the next sowing season has begun. A small farmer in Vidarbha or a fishing community in coastal Odisha cannot afford to wait. Parametric insurance, with its three-to-seven day settlement, provides liquidity precisely when it is most needed: immediately after a catastrophe.

There is, however, a concept called basis risk — the possibility that the parametric trigger fires without the policyholder actually suffering a loss (or vice versa). For example, a farmer two kilometres outside the weather station's measurement zone may experience drought while the station records adequate rainfall. Basis risk is the primary limitation of parametric insurance, and good product design — through denser sensor networks and smaller geographic trigger zones — works to minimise it.

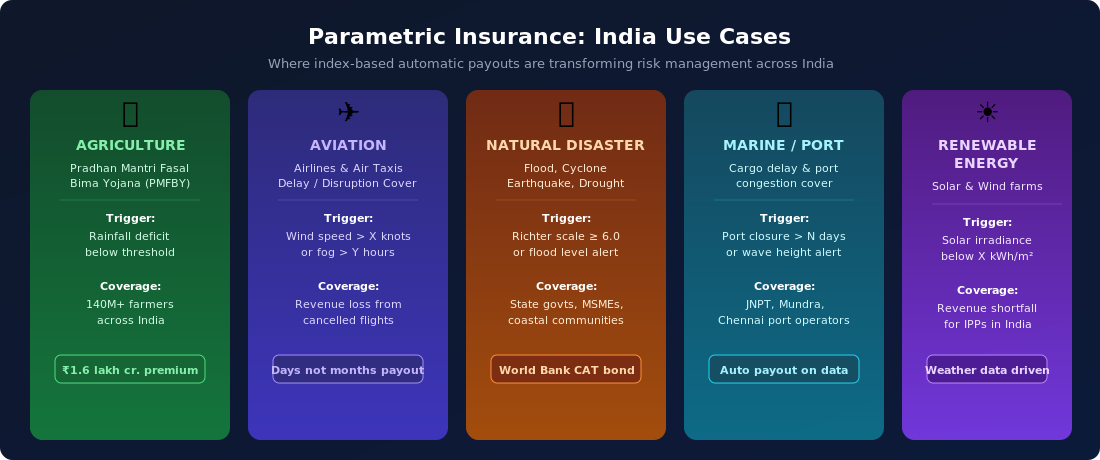

Parametric Insurance in India: Sectors and Use Cases

India's diverse climate, geography, and economic structure make it one of the most fertile markets globally for parametric insurance. The technology is already deployed at scale in several sectors.

Agriculture is the oldest and largest application. PMFBY uses a combination of area-based and parametric triggers — crop-cutting experiments supplemented by rainfall and temperature indices measured by IMD's network — to cover over 140 million farmers across kharif and rabi seasons. The total premium collected under PMFBY has exceeded ₹1.6 lakh crore since inception. Private insurers like ICICI Lombard and AIC have launched standalone weather-based parametric products for horticulture, floriculture, and aquaculture.

Aviation is an emerging application, especially relevant as India's air taxi and eVTOL ecosystem grows. Airlines and air taxi operators face revenue losses when flights are cancelled due to fog, cyclones, or crosswinds exceeding safe limits. A parametric policy tied to visibility below 800 metres at a specific airport, or wind speed above 35 knots, pays out automatically — providing immediate liquidity without any claims adjudication. TropoGo's parametric aviation products are purpose-built for India's unique weather and regulatory environment.

Natural catastrophe covers are critical for India, which faces cyclones along its 7,516-kilometre coastline, earthquakes in the Himalayan belt, and floods across the Indo-Gangetic plain annually. India has participated in World Bank catastrophe bond (CAT bond) structures and NDMA has explored sovereign parametric covers for state government fiscal resilience. Individual businesses — hotels, logistics companies, power plants — can purchase parametric covers triggered by cyclone track intersection or flood gauge levels.

Marine and port operations represent a growing market. JNPT, Mundra, and Chennai port operators face business interruption losses during port closures due to cyclones or heavy seas. Parametric triggers based on wave height alerts from the Indian National Centre for Ocean Information Services (INCOIS) can automatically compensate for lost port revenue.

Renewable energy is the newest frontier. India's 300+ GW renewable capacity target by 2030 creates billions of dollars of solar and wind farm investment exposed to weather variability. A solar farm in Rajasthan whose production drops below projected levels due to prolonged cloud cover can receive automatic compensation based on solar irradiance data from the National Institute of Wind Energy (NIWE) or satellite feeds. Wind farm operators can hedge generation shortfall risk against wind speed indices measured at hub height.

Benefits of Parametric Insurance

The advantages of parametric insurance over traditional indemnity covers are substantial, particularly for India's underserved market segments.

Speed of payout — three to seven days versus thirty to one hundred eighty days for traditional claims. This is transformative for small farmers and SMEs who need immediate liquidity after a disaster.

Zero paperwork — no claim forms, no documents, no surveyor visits. The data speaks for itself.

Transparency — both parties know exactly what will trigger a payout and how much will be paid. There are no surprises, no disputes, and no under-settlement.

Lower distribution cost — because the product is standardised, it can be sold digitally at low cost, making it viable for micro-insurance coverage at the ₹500–₹2,000 premium bracket.

Flexibility of use — the payout is unrestricted. Farmers can use it to buy seeds, repay micro-loans, or cover living expenses — not just documented crop losses.

Scalability — the same parametric product can cover a small farmer in Punjab and a large agri-processing company in Andhra Pradesh, with only the payout sum varying.

Challenges and Limitations

Parametric insurance is not a universal solution. Several challenges limit its applicability and penetration in India.

Basis risk — the most fundamental limitation. If the parametric index does not correlate perfectly with actual losses at the individual level, policyholders may feel shortchanged or may receive payouts without having suffered a loss.

Data infrastructure gaps — reliable, granular, real-time data is essential. India's IMD network has improved significantly, but hyperlocal data — particularly for remote agricultural areas — remains incomplete.

Product complexity — designing a parametric product that minimises basis risk while remaining affordable requires actuarial and meteorological expertise that few Indian insurers currently possess.

Consumer awareness — most Indian policyholders — including SME owners and farmers — are unfamiliar with parametric triggers. Mis-selling risk is high if sales channels do not explain the product clearly.

IRDAI regulatory framework — while IRDAI has begun issuing sandboxed approvals for parametric products, a comprehensive regulatory framework for index-based insurance products is still evolving in India.

IRDAI's Regulatory Approach to Parametric Insurance

The Insurance Regulatory and Development Authority of India (IRDAI) has acknowledged parametric insurance as a priority innovation area. Under IRDAI's Regulatory Sandbox mechanism (launched in 2019), multiple insurers have received approval to pilot parametric products across agriculture, weather, and health segments. IRDAI's vision document for 2025 — "Insurance for All" — explicitly identifies index-based parametric products as a vehicle for expanding coverage to underserved rural populations.

For aviation and specialty risks, IRDAI allows parametric structures under the General Insurance framework subject to product file-and-use approvals. Reinsurers like Munich Re, Swiss Re, and GIC Re play a critical role in backing India's parametric products, having developed deep expertise in index-based risk transfer through global deployments. As India's IoT infrastructure — from ISRO satellite networks to the National Data and Analytics Platform (NDAP) — matures, IRDAI is expected to formalise a dedicated parametric insurance guideline by 2026–27.

Why Parametric Insurance is the Future of Risk Management in India

Climate change is making extreme weather events more frequent and more severe across India. The 2023 monsoon produced both extreme floods in Himachal Pradesh and severe drought in parts of Maharashtra simultaneously — a bifurcated risk environment that traditional insurance products struggle to price and settle efficiently. Parametric insurance, with its ability to pay out rapidly and objectively based on measured conditions, is structurally better suited to India's climate risk profile than loss-adjusted indemnity products.

For businesses in high-risk sectors — airlines, logistics companies, agri-processors, renewable energy developers, coastal hoteliers — parametric insurance is evolving from a niche product to a core component of enterprise risk management. A well-designed parametric policy, combined with traditional property and liability covers, creates a layered risk management structure where the parametric layer provides immediate liquidity and the traditional layer covers residual, harder-to-quantify losses.

TropoGo specialises in designing parametric insurance solutions for India's unique risk environment — combining regulatory expertise, reinsurance relationships, and data partnerships to deliver transparent, fast-paying parametric covers for aviation, weather, and specialty risks. Our parametric products include the following specialist covers:

Aviation weather disruption — automatic payout when wind speed, visibility, or precipitation triggers exceed agreed thresholds at designated airports.

Cyclone track parametric — payout triggered when a named cyclone's centre passes within a defined radius of the insured location at agreed wind speed intensity.

Rainfall deficit cover — for agri-businesses, agri-logistics, and input companies whose revenues are correlated with monsoon performance.

Renewable energy generation shortfall — parametric cover for solar and wind IPPs against irradiance or wind speed deficits below P90 projections.

Earthquake intensity cover — automatic payout when peak ground acceleration or Modified Mercalli Intensity exceeds a defined threshold at an agreed location.

Port disruption parametric — covers marine operators and port businesses for revenue loss during government-declared port closures triggered by adverse sea conditions.

The Road Ahead for Parametric Insurance in India

India's parametric insurance market is at an inflection point. The convergence of better data infrastructure, a more innovation-friendly IRDAI, and growing climate risk awareness among India's corporate and agricultural sectors creates the conditions for rapid market development. Global reinsurers are investing in India-specific parametric product development, and insurtech startups are building digital distribution platforms that can deliver parametric micro-insurance at scale.

By 2030, parametric insurance in India is projected to become a multi-thousand crore segment — covering not just agriculture but aviation, renewable energy, coastal real estate, and supply chain resilience. Businesses and individuals who understand and adopt parametric insurance early will gain a meaningful competitive advantage: the ability to recover quickly and predictably from climate and catastrophe events, without waiting months for a surveyor's report.

Ready for Automatic Payouts?

TropoGo designs bespoke parametric insurance products for aviation, weather, and specialty risks in India — with payouts in days, not months.

What is the difference between parametric and traditional insurance?

Traditional insurance compensates for actual, verified losses after a surveyor assesses the damage — a process that can take weeks or months. Parametric insurance pays out a pre-agreed sum automatically when a measurable index (rainfall, wind speed, seismic intensity) breaches a defined threshold — regardless of the actual loss incurred. The trade-off is basis risk: the index may not perfectly reflect individual losses.

How quickly does parametric insurance pay out in India?

Parametric insurance typically pays out within three to seven business days of the trigger event being confirmed by the agreed data source (IMD, ISRO, USGS, INCOIS, or an IoT sensor network). This compares favourably with traditional agricultural insurance under PMFBY, which has historically taken 30–180 days — and sometimes longer — to settle claims.

What is basis risk in parametric insurance?

Basis risk is the gap between the parametric trigger and the actual loss experienced. It occurs in two directions: the trigger fires but the policyholder hasn't suffered significant loss (over-insurance), or the policyholder suffers loss but the index doesn't breach the threshold (under-insurance). Good product design — using denser sensor networks, smaller trigger zones, and multi-parameter indices — minimises basis risk.

Is parametric insurance regulated by IRDAI in India?

Yes. IRDAI regulates parametric insurance products under its General Insurance framework. Under IRDAI's Regulatory Sandbox mechanism, insurers can pilot innovative parametric structures before applying for standard file-and-use approval. IRDAI's "Insurance for All by 2047" vision explicitly identifies parametric products as a key tool for expanding agricultural and rural insurance coverage.

Can small businesses and farmers buy parametric insurance in India?

Yes — and this is precisely where parametric insurance has the greatest impact. Because parametric products are standardised and can be distributed digitally, they are viable at very low premium levels (₹500–₹5,000 for micro-covers). PMFBY already covers 140+ million farmers with a parametric-hybrid structure. Private parametric weather products for horticulture, floriculture, and aquaculture are available through several IRDAI-licensed insurers.

How do I get a parametric insurance quote for my aviation or weather risk in India?

TropoGo specialises in bespoke parametric insurance solutions for aviation, weather, renewable energy, and catastrophe risks in India. Our team combines regulatory expertise, reinsurance partnerships, and data capabilities to design transparent, fast-paying parametric covers. Visit our parametric insurance page to understand your options and speak with a specialist.

Parametric insurance is not the future — it is already transforming risk management for India's farmers, airlines, port operators, and renewable energy developers. If your business faces weather, climate, or catastrophe risk, a parametric insurance structure could provide the certainty and speed of payout that traditional indemnity covers cannot. Explore TropoGo's specialist parametric products and find out how automatic payouts can protect your business when you need it most.