In May 2023, the Indian Army inducted the SWITCH MARK-2 UAV from ideaForge — the largest domestic defence drone procurement order in India's history at that point. Months later, Bharat Forge's Nagastra-1 loitering munition completed its user trials and was formally inducted into service. The Defence Research and Development Organisation is simultaneously running parallel programmes on the Tapas-BH medium-altitude long-endurance UAV, the ALFA-S autonomous flying vehicle, and the Archer-NG high-altitude pseudo-satellite. At any given moment, dozens of drone prototypes from iDEX winners, DRDO establishments, and public sector aerospace divisions are being put through their paces at air force stations, army firing ranges, and naval test facilities from Chandipur to Bengaluru. Each of these trial flights carries a risk that standard aviation insurance was never designed to absorb: the risk of losing a one-of-a-kind prototype or first-batch production system that represents years of research and tens of crores in development investment. Defence Testing & Trial Insurance exists to protect precisely this gap.

What is Defence Testing & Trial Insurance?

Defence Testing & Trial Insurance is a specialist form of aviation hull and liability cover designed for unmanned aerial systems that are undergoing formal military evaluation, government acceptance trials, or official airworthiness certification testing — before they are formally inducted into service. It is distinct from both standard commercial drone insurance (which covers civilian operations) and in-service defence equipment insurance (which covers serial-production assets already inducted into the armed forces). Trial insurance bridges the critical gap between "prototype completed in the factory" and "asset formally accepted into the armed forces inventory."

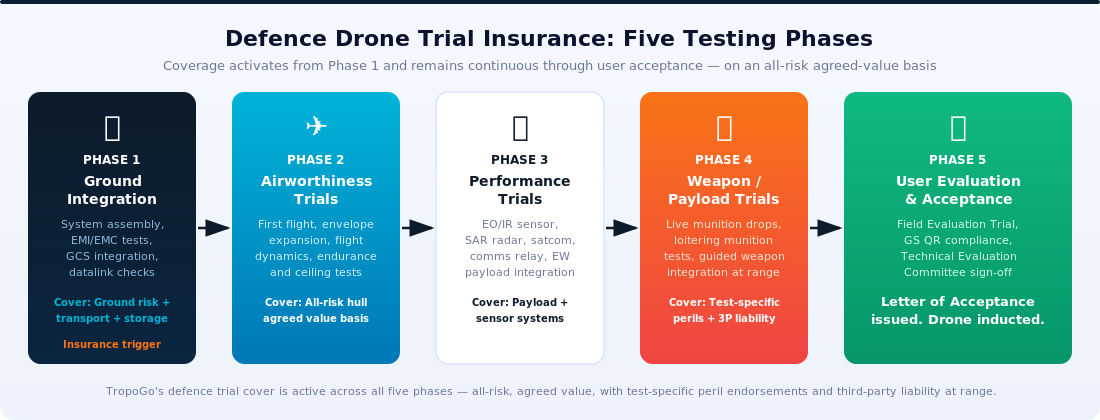

The subject of insurance is typically a drone system in one of five stages: pre-flight ground testing and system integration; initial airworthiness and flight envelope expansion; performance and endurance trials under the user's evaluation criteria; live payload or weapon trials for armed or weapon-equipped systems; and final user evaluation trials before a Letter of Acceptance or a government supply order is signed.

How Defence Drone Trial Insurance Works

A Defence Testing & Trial policy is structured as an all-risk hull and liability policy, with specific endorsements for the testing environment. Coverage activates from the moment the drone leaves the manufacturer's facility for a designated trial site — typically an Air Force station, an Army range complex, or a naval airfield — and remains continuous through the entire formally documented trial programme.

The policy's key technical parameters differ substantially from standard drone insurance:

Agreed value basis: Trial drones are prototypes or first-batch units with no established market value. Cover is issued on agreed value — the manufacturer and insurer agree a value upfront (typically the full development cost plus a margin for intellectual property), and this amount is paid without dispute in a total loss. This is non-negotiable for defence trials: a prototype lost during an envelope expansion test is irreplaceable, not replaceable with a market equivalent.

All-risk hull coverage: Covers physical damage or total loss of the drone airframe, payload systems, ground control stations, and associated data links caused by any peril — including test-induced structural failure, unexpected weather at trial sites, and control anomalies during limit testing. Unlike standard drone policies that exclude "testing" as a peril, defence trial policies explicitly include it.

Third-party liability: Trials take place at restricted military ranges, but the liability exposure to range personnel, adjacent civil infrastructure, and other aircraft remains real. Third-party liability cover is mandatory under most MoD trial protocols and is required before range access is granted. Without it, the range commandant will not clear the drone for flight.

Test-specific peril endorsements: Explicit coverage for loss during live weapon or payload deployment tests, classified signal environment testing (EW trials), and high-altitude operations outside the DGCA's standard regulatory ambit under the CAR Section 1 Series X Part I military exemption.

India's Defence Drone Ecosystem — Who Needs Trial Cover?

India's defence drone sector has broadened dramatically since the Innovations for Defence Excellence (iDEX) programme was launched in 2018. The entities that need trial insurance span the full defence value chain:

DRDO Establishments. The Aeronautical Development Establishment (ADE) in Bengaluru leads India's military UAS programmes, including Tapas-BH (MALE UAS), ALFA-S (autonomous flying vehicle), and the Rustom series. The Defence Research and Development Laboratory (DRDL) in Hyderabad handles missile and guided weapon payloads that integrate with drone platforms. Every prototype that leaves an ADE hangar for range testing needs trial cover — and DRDO's own insurance framework requires it.

Hindustan Aeronautics Limited (HAL). HAL is developing the Rustom-2 MALE UAS and the CATS Warrior loyal wingman platform for the Indian Air Force. These are high-value, multi-year development programmes with no market equivalent. Trial insurance at agreed value is the only mechanism that provides meaningful financial protection during evaluation flights.

Bharat Forge (Kalyani Group). The Nagastra-1 loitering munition, India's first domestically produced loitering ammunition system, was inducted into the Indian Army in 2024 after completing full user trials. Every trial sortie that preceded induction — including live warhead tests at Army firing ranges — was a period of maximum financial exposure. Without all-risk agreed value cover, the entire investment could have been wiped out in a single failed test.

ideaForge Technology. The SWITCH MARK-2 and SWITCH UAV family are India's most battle-tested domestic drones. But before the Army's landmark induction order was signed, ideaForge had to complete multiple rounds of user evaluation trials at altitude, in extreme temperature, and in high-wind conditions at Himalayan border deployments. Each trial flight was an insurable event.

iDEX Winners and Defence Startups. The iDEX programme has issued over 75 drone-related challenges since 2018. Every winner must complete field evaluation trials before a procurement order can be signed. Most iDEX winners are startups with limited balance sheets — a total loss during trials could be existential without insurance. TropoGo structures trial cover specifically for the iDEX lifecycle: from prototype funding through to LoA issuance.

Benefits of Defence Trial Insurance

Protects years of R&D investment in a prototype that has no market replacement value

Mandatory for range access — MoD trial protocols require proof of insurance before any trial drone is cleared for flight at designated ranges

Enables bank financing of trial programmes — lenders require insurance as security before funding prototype development

Agreed value means zero dispute on total loss settlement — critical for prototypes with no market comparables

Test-specific peril endorsements cover risks that standard aviation policies explicitly exclude

Challenges in Defence Trial Insurance

Classified operations: Many trial parameters, payloads, and operational scenarios cannot be disclosed to standard underwriters, requiring specialist insurers with appropriate security clearances and confidentiality frameworks

No loss history: New drone types have no actuarial loss data, making risk assessment a specialist underwriting exercise rather than a formula application

High agreed values vs limited track record: A ₹15 crore prototype from a two-year-old iDEX startup requires underwriters comfortable with defence risk who can assess technical maturity, not just financial history

Multi-range complexity: A single trial programme may span DGCA-regulated civilian airspace, MoD-controlled ranges, and high-altitude Himalayan test sites — each with different regulatory and insurance requirements

India's MoD Regulatory Framework for Defence Drone Trials

India's defence procurement framework creates specific insurance requirements at each stage of the trial lifecycle:

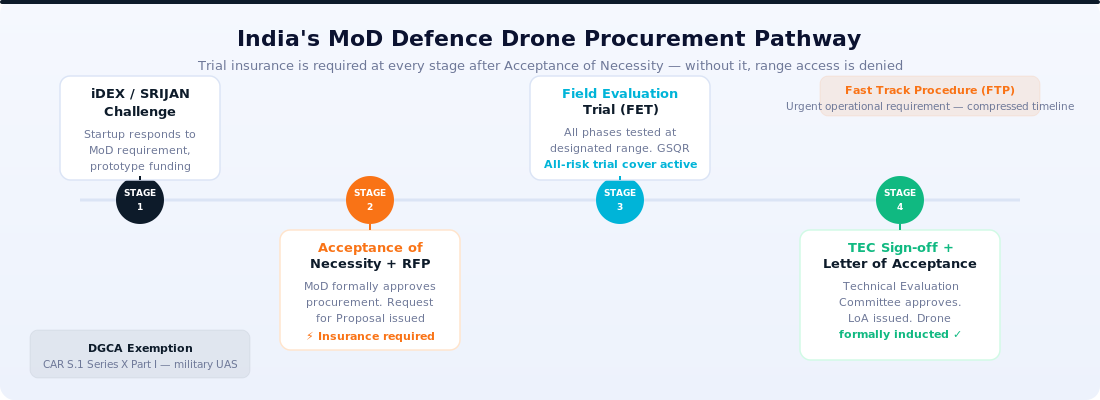

iDEX and SRIJAN Challenges. The Innovations for Defence Excellence (iDEX) and the Self-Reliance in Individual Items & Systems (SRIJAN) portals are the entry points for defence startups into India's procurement system. When a startup wins an iDEX challenge and receives MoD prototype funding, it enters a structured trial cycle that requires insurance before any range activity begins.

Acceptance of Necessity and RFP Stage. The Ministry of Defence formally approves procurement through the Acceptance of Necessity (AoN) mechanism. Once AoN is issued and a Request for Proposal is released, vendors submitting drone systems for evaluation must demonstrate adequate insurance as part of their technical proposal. This is when TropoGo's cover is most commonly activated.

Field Evaluation Trial (FET) Stage. The FET is the formal military evaluation of a drone system against the user service's General Staff Qualitative Requirements (GSQR). At this stage, the drone must be fully insured under an all-risk trial policy — without it, the range commandant will not grant flight clearance. The FET covers all the testing phases from airworthiness through payload integration.

DGCA Exemption for Military UAS. Military drone operations are exempt from standard DGCA regulations under CAR Section 1, Series X, Part I. This means trial drones operating at Army ranges, Air Force stations, and naval airfields do not require the UIN registration, remote pilot licence, or flight clearances that apply to civilian drones. However, MoD's own operational safety requirements — including mandatory insurance — apply in full.

Fast Track Procedure (FTP). For urgent operational requirements — such as rapid induction of counter-drone systems or border surveillance drones — the MoD invokes the Fast Track Procedure, which compresses the timeline from AoN to LoA. FTP drones still require full trial insurance, but the cover must be structured and issued on an accelerated basis. TropoGo can issue FTP-compliant trial cover within 48 hours of receiving a complete proposal.

Every trial flight is an uninsured risk waiting to happen — unless you have specialist defence cover in place before range clearance is requested.

TropoGo's defence trial policy is designed for the full spectrum of Indian defence drone programmes — from iDEX prototype flights to DRDO MALE UAS field evaluations. Six core covers are included:

All-Risk Hull Cover — Agreed Value Basis: Total loss or damage to the drone airframe from any peril during the trial programme, settled at the pre-agreed value without reference to market value or depreciation. Covers test-induced failures, weather events, control anomalies, and envelope expansion incidents.

Payload and Weapons System Cover: EO/IR sensor arrays, SAR radar systems, electronic warfare suites, guided munition interfaces, and loitering munition warheads — all covered during integration testing and live deployment trials at designated ranges.

Ground Control Station and Datalink Cover: GCS hardware, satellite communication terminals, RF link equipment, encrypted datalink systems, and associated ground infrastructure at the trial site, including transit cover between facilities.

Third-Party Liability at Range: Liability to range personnel, adjacent military and civil infrastructure, and other aircraft arising from trial operations — at the limits required by MoD range standing orders and the relevant service headquarters.

Ground Risk Cover: Damage during transport to the trial site, storage at range facilities, and pre-flight assembly and integration activities — critical for prototype drones that travel long distances between manufacturer facilities and remote test ranges.

Test-Specific Peril Endorsements: Explicit coverage for loss during live weapon deployment tests, classified signal environment (EW) trials, high-altitude operations, and envelope expansion manoeuvres — the exact perils that standard aviation policies exclude and defence trial policies must include.

India's defence drone market is projected to reach ₹1.5 lakh crore over the next decade, driven by the Aatmanirbhar Bharat initiative, the iDEX programme's expanding reach, and the tri-services' rapidly growing appetite for unmanned systems across surveillance, logistics, combat, and anti-drone roles. The Indian Army, Navy, and Air Force are simultaneously running procurement programmes across at least 25 distinct drone categories — from micro-drones for infantry platoons to MALE UAS for maritime patrol and high-altitude ISR.

For India's defence drone manufacturers — whether established PSUs or first-generation iDEX startups — the trial phase is where the financial exposure is greatest and the insurance market is thinnest. Companies that secure specialist trial cover from a partner with genuine defence underwriting experience will be better positioned to move through evaluation cycles quickly, secure range access without delay, and present credible risk management frameworks to MoD evaluators. Those that don't will find themselves grounded — literally — waiting for insurance that could have been arranged weeks earlier.

Frequently Asked Questions

What is the difference between defence trial insurance and standard drone insurance?

Standard drone insurance covers civilian or commercial operations — deliveries, surveys, photography — under DGCA regulations, with policies based on market value and standard aviation perils. Defence trial insurance covers military evaluation operations at MoD ranges, on an agreed value basis, with explicit endorsements for test-specific perils including live weapon trials and envelope expansion. The two products are structurally different and cannot substitute for each other.

Does the MoD require insurance for Field Evaluation Trials?

Yes. MoD range standing orders require vendors to present proof of valid insurance before a trial drone is cleared for flight at any designated military range. The range commandant's flight clearance is withheld until adequate third-party liability cover — at the minimum limits specified by the relevant service headquarters — is confirmed in writing. All-risk hull cover at agreed value is additionally required by most MoD procurement process documents.

How is the insured value determined for a prototype drone?

Prototype drones have no market value — they are unique assets built to specifications that may not exist anywhere else. TropoGo insures prototypes at agreed value, which is determined by the manufacturer's documented development cost, the cost to recreate the prototype, the value of the intellectual property embedded in the system, and any strategic value assigned by the MoD programme office. The agreed value is fixed at policy inception and paid in full on total loss, without depreciation or market reference.

Are weapon and payload systems covered under the trial policy?

Yes. TropoGo's defence trial policy explicitly covers payload and weapons systems — including EO/IR sensors, SAR radar, electronic warfare suites, guided munition interfaces, and loitering munition warheads — during integration testing and live deployment trials at designated ranges. Standard drone policies routinely exclude weapons and munitions as a class of payload. TropoGo's defence-specific endorsements remove this exclusion for authorised military trial operations.

What happens if the drone is destroyed during a classified trial?

TropoGo's defence trial policies include confidentiality provisions that allow claims to be processed without disclosing classified trial parameters, operational specifications, or payload details to non-cleared personnel. The agreed value settlement is triggered by the physical loss of the insured asset, not by public disclosure of the cause. Our defence underwriting team operates under appropriate confidentiality frameworks for classified programme coverage.

How do I get Defence Testing & Trial insurance from TropoGo?

Visit TropoGo's Defence Testing & Trial Insurance page. Provide details of the drone system (type, dimensions, agreed value), the trial programme (MoD programme reference, range location, trial phases), and your organisation's profile. TropoGo can issue FTP-compliant cover within 48 hours for urgent trial programmes. For iDEX-funded trials, we have a streamlined proposal process aligned with MoD timelines.

India's defence drone sector is entering its most ambitious decade — from Chandipur to Bengaluru, from Himalayan ranges to naval test facilities. The manufacturers who will succeed are those who treat trial insurance as mission-critical infrastructure, not an afterthought, because the MoD range commandant will not grant clearance without it.