What is Fire Insurance and Why It's Essential for Your Property

2 May 2026 | 6 min read

Fire Insurance India

A fire can destroy years of investment in minutes. India's STFI policy and its allied perils extensions protect your building, stock and business — here's everything you need to know.

On 25 February 2023, a fire at a garment factory in Surat ripped through five floors in under forty minutes, destroying stock worth ₹8 crore and leaving 200 workers jobless for three months. The owners carried a basic third-party liability policy — fire insurance had lapsed three weeks earlier. The factory never fully reopened.

Fire is India's single most common cause of insured property loss. IRDAI data shows that fire and allied perils claims account for over 40% of all non-life claims by value — yet millions of residential, commercial, and industrial properties either carry no cover or are critically under-insured. If you own property, stock, plant, or machinery in India, this blog is the most important insurance read you will have this year.

What is Fire Insurance?

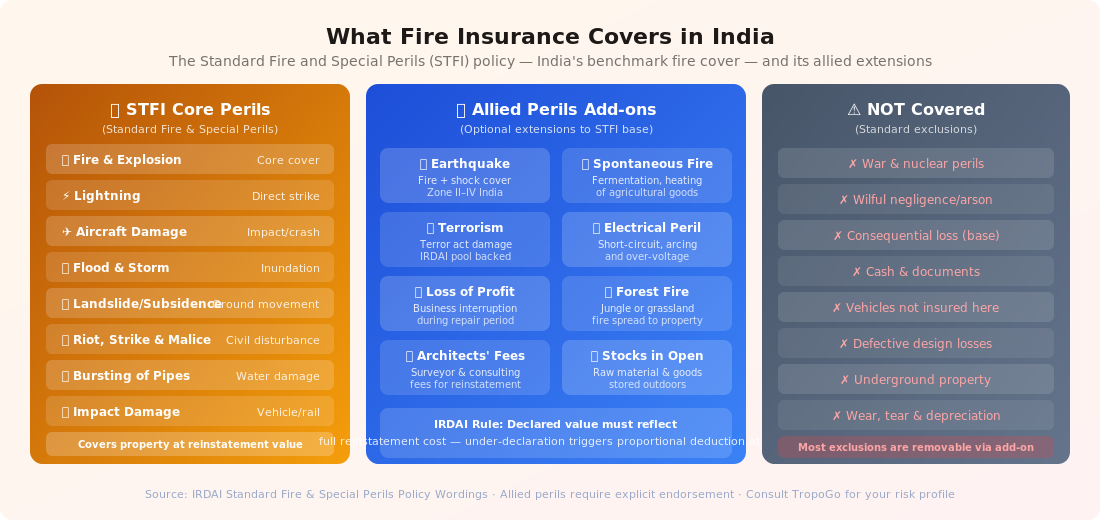

Fire insurance is a property insurance policy that compensates the insured for financial loss or damage to property caused by fire and related perils. In India, the benchmark product is the Standard Fire and Special Perils (STFI) Policy, governed by IRDAI tariff guidelines and issued by all licensed general insurers. The STFI policy is not limited to fire alone — it covers a schedule of eleven standard perils including lightning, explosion, aircraft damage, riot and strike, storm, cyclone, flood, landslide, subsidence, bursting of pipes, and impact damage by vehicles or trains.

Critically, fire insurance is an indemnity contract: it restores you to the financial position you were in before the loss, not better. The sum insured must therefore reflect the current market value (for older structures) or reinstatement value (rebuild cost) of the insured property. Getting this wrong — a very common mistake — leads to under-insurance, which triggers the average clause and dramatically reduces your claim settlement.

What Does the STFI Policy Cover?

The STFI policy covers three broad asset classes: the building or structure, the contents (plant, machinery, furniture, fixtures), and stock (raw materials, work-in-progress, finished goods). Each is declared separately at the time of policy inception and must be updated annually. The core perils and allied add-ons are extensive — understanding what you have versus what you need is the most important step in structuring a fire insurance programme.

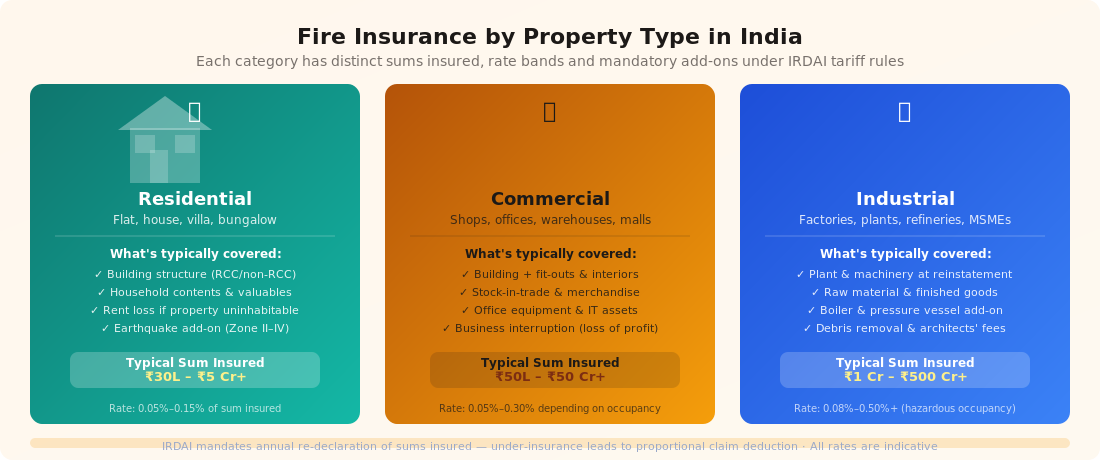

Types of Property Covered

Fire insurance in India is available across three broad property categories, each with distinct premium rates, sum insured requirements, and typical add-on profiles. Residential properties carry the lowest base rates; industrial properties — especially those handling hazardous materials — attract the highest, with fire occupancy class directly influencing the premium calculation.

The Average Clause: India's Most Misunderstood Fire Insurance Rule

Under the average clause, if your property is insured for less than its actual value, any claim is settled proportionally. The formula is simple but painful:

Claim settlement = (Sum Insured ÷ Actual Value) × Assessed Loss

Example: Your factory building is worth ₹5 crore but insured for ₹2.5 crore (50% under-insured). A fire causes ₹1 crore in loss. Under the average clause, you receive only ₹50 lakh — half of your actual loss — because you were only 50% insured. The other ₹50 lakh is your uninsured burden. This is why IRDAI strongly recommends annual revaluation, and many large corporates hire independent property valuers to ensure accurate declaration.

Key Add-Ons That Every Property Owner Should Consider

The base STFI policy has deliberate exclusions that add-ons address. The most important add-ons for different property types include:

Earthquake Cover (Fire + Shock): India has significant seismic risk — Zone II (low), Zone III (moderate), Zone IV (high) and Zone V (very high, including North-East, Himalayan regions, Gujarat coast). Properties in Zone III and above should carry earthquake add-on as a non-negotiable.

Loss of Profit / Business Interruption: Compensates for lost gross profit during the period your business is unable to operate due to a covered fire event. The indemnity period is set at policy inception (typically 6, 12, or 24 months) — choose conservatively because rebuilding a fire-damaged factory in India takes longer than most owners expect.

Terrorism Cover: Backed by the IRDAI-mandated terrorism pool, this add-on is compulsory for properties with sum insured above ₹50 crore in notified cities. For smaller properties in high-risk locations, it is strongly advisable.

Electrical Installation Peril: Covers damage from short-circuit, arcing and over-voltage — the most common ignition source in Indian industrial and commercial properties. Not covered under the base STFI, yet responsible for a significant proportion of fire losses.

Spontaneous Combustion: Essential for agricultural storage, cotton ginning, jute baling, paper mills, and other industries where raw material self-heating is a documented risk.

Architects', Surveyors' and Consulting Engineers' Fees: Post-fire reinstatement requires professional oversight. This add-on covers their fees, which can amount to 3–5% of the reinstatement cost on large projects.

How Fire Insurance Premiums Are Calculated in India

The premium for a fire insurance policy is calculated as a percentage of the sum insured, based on the Occupancy Rate — a tariff classification that reflects the fire hazard associated with how the insured premises is used. A residential flat in a concrete building (non-hazardous occupancy) attracts a base rate of 0.05–0.10% of sum insured, while a fireworks manufacturer or chemical storage facility (highly hazardous) may attract 0.50–1.50% or more.

Key factors affecting premium: construction type (RCC, load-bearing, wood-framed), occupancy hazard class, fire suppression systems (sprinklers and hydrants attract discounts of 15–30%), past claims history, location (proximity to water source, fire station response time), and the specific add-ons chosen. A well-structured fire safety programme can significantly reduce premiums while improving actual risk management.

Is Your Property Adequately Insured Against Fire?

Under-insurance is India's silent property risk — millions of properties are insured at a fraction of their true rebuild cost. TropoGo's fire insurance specialists help you calculate the right sum insured, choose the correct add-ons, and ensure your STFI policy is structured to pay in full when it matters.

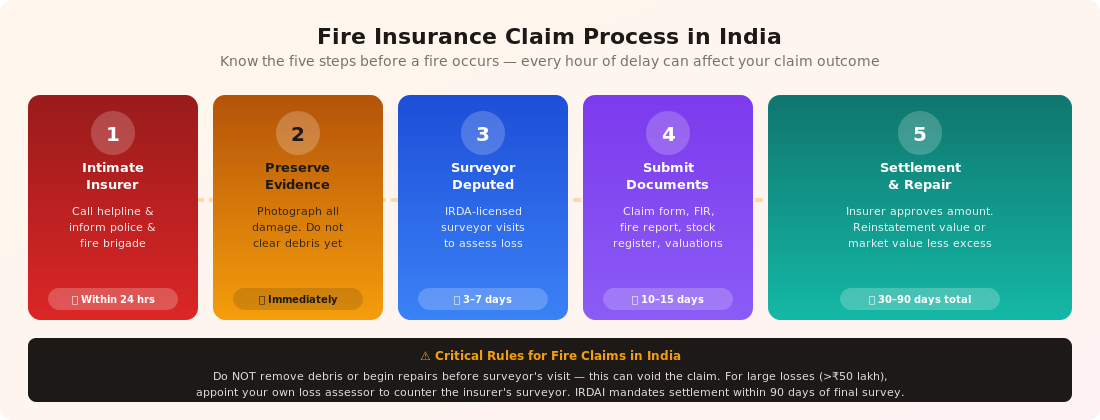

The claims process for fire insurance is more document-intensive than most other insurance lines — and the timeline matters enormously. Key missteps, like removing debris before the surveyor visits or delaying FIR filing, can result in claim repudiation. Know the process before a fire occurs.

Why TropoGo for Fire Insurance?

Fire insurance is not a commodity product — the difference between a well-structured policy and a poorly-structured one can be tens of crores at claim time. TropoGo's fire insurance platform brings specialist underwriting expertise to residential, commercial, and industrial clients across India. Key covers available include:

STFI Base Policy: Full Standard Fire and Special Perils cover for buildings, contents and stock, with accurate sum insured calculation support to eliminate under-insurance risk.

Earthquake Add-On: Zone-specific earthquake (fire + shock) endorsement covering the full spectrum of seismic risk across India's five earthquake zones.

Business Interruption / Loss of Profit: Gross profit protection for the indemnity period needed to rebuild and resume operations — with proper turnover and standing charges calculation.

Electrical Installation Peril: Short-circuit and arcing cover for commercial and industrial properties where electrical failure is the primary ignition risk.

Terrorism Pool Cover: IRDAI-backed terrorism endorsement, compulsory for large properties and recommended for any commercially-significant insured location.

Industrial All-Risk (IAR): Comprehensive package for large industrial clients combining fire, machinery breakdown, business interruption and liability covers under a single policy.

Frequently Asked Questions

What is the Standard Fire and Special Perils (STFI) policy in India?

The STFI policy is India's standard fire insurance product, governed by IRDAI tariff rules. It covers eleven named perils: fire, lightning, explosion, aircraft damage, riot/strike/malicious damage, storm/cyclone/typhoon/tempest/hurricane/tornado/flood/inundation, impact damage, subsidence and landslide, bursting of pipes, and missile testing operations. Coverage can be extended via add-ons for earthquake, terrorism, loss of profit, and other specific risks.

What is the average clause in fire insurance and how does it affect claims?

The average clause applies when a property is under-insured. If you insure for less than the actual value and suffer a partial loss, your claim is settled proportionally: (Sum Insured ÷ Actual Value) × Assessed Loss. For example, if your ₹4 crore factory is insured for ₹2 crore and suffers ₹80 lakh in fire damage, you receive only ₹40 lakh. Annual revaluation of sums insured is the only protection against this clause.

Does fire insurance cover electrical short-circuit damage?

Damage from electrical short-circuit, arcing, or over-voltage is excluded from the standard STFI policy. However, it can be added via the Electrical Installation Peril endorsement. This add-on is essential for commercial and industrial properties where electrical faults are the most common fire cause — ask your insurer or broker to include it explicitly.

Is earthquake covered under fire insurance in India?

Earthquake cover is not part of the standard STFI base policy — it must be added as an endorsed extension (Earthquake Fire + Shock). Given India's seismicity — large parts of Gujarat, Rajasthan, Maharashtra, Delhi-NCR and the entire North-East fall in Zones III–V — earthquake add-on is strongly recommended for any property with a significant rebuilding cost.

What documents are required to file a fire insurance claim?

The core document set for a fire insurance claim includes: completed claim form, FIR from police, fire brigade report, surveyor's loss assessment report, photographs of damage, stock register and purchase records, valuation reports, repair/rebuilding estimates, and the policy document. For business interruption claims, audited accounts for the prior 3 years are also required. Always notify your insurer within 24 hours of a fire — delay can provide grounds for claim reduction.

How do I get the best fire insurance coverage for my property?

Start with an accurate reinstatement value — the cost to rebuild or replace your property at today's prices, not the original purchase price or market value. Identify your key risks: earthquake zone, electrical hazard, stock type, business interruption exposure. Choose add-ons accordingly. Install fire suppression systems (sprinklers, hydrants) for 15–30% premium discounts. Review and update your sum insured every year. TropoGo's fire insurance specialists can help you structure the right programme for your property type and risk profile.

Fire insurance is not a regulatory checkbox — it is the financial foundation that determines whether your property, business, and livelihood survive a fire event. A correctly structured STFI policy with the right add-ons costs a fraction of a percent of your property's value. The cost of not having one, as the Surat factory owners discovered, can be everything.