What is Group Health Insurance and Why Companies Need It

21 May 2026 | 8 min read

Give your team the health cover they deserve — IRDAI-approved group mediclaim for Indian companies of every size

No medical examination, pre-existing diseases covered from day one — a single group policy protects your entire workforce at 30–50% less than individual retail cover.

In June 2024, a mid-sized Bengaluru IT firm made headlines not for a product launch, but for an attrition crisis. Three senior engineers resigned in the same week, citing one reason above all others: their new employer offered a group health insurance cover of ₹10 lakh per family, while the old one offered nothing. The company's HR director later told Economic Times that replacing those three engineers cost the firm ₹28 lakh in recruitment and onboarding — ten times what a group health policy for the entire team would have cost.

That story plays out quietly across thousands of Indian workplaces every year. Group health insurance — also called Group Mediclaim or Employee Health Insurance — has moved from a perk that large companies offered to a baseline expectation that candidates across sectors use as a filter before accepting any offer. India's group health insurance market crossed ₹30,000 crore in gross written premium in FY2024 and is growing at roughly 20 percent annually, driven by rising medical inflation, post-COVID awareness and a competitive talent market where healthcare benefits are now table stakes.

This guide explains what group health insurance is, what it covers, how it is structured under IRDAI's framework, and why — for every Indian employer from a 10-person startup to a 10,000-employee conglomerate — it is no longer optional.

What is Group Health Insurance?

Group health insurance is a single insurance policy that covers a defined group of people — typically a company's employees and, under extensions, their dependants — under a master policy held by the employer. The insurer agrees to cover all eligible members without individual medical underwriting, in exchange for a group premium calculated on the basis of the collective risk profile.

In India, group health insurance is regulated by the IRDAI under the Group Insurance Guidelines and is typically structured as a one-year renewable contract between the employer (the policyholder) and an IRDAI-licensed general or health insurer. The policy is renewed annually, with premiums recalculated based on the previous year's claims experience, group size changes and medical inflation adjustments.

Unlike individual health policies, group plans do not require members to submit to individual medical examinations at inception. Pre-existing diseases are typically covered from day one — a significant advantage over retail policies that impose two-to-four year waiting periods. This makes group health insurance particularly valuable for employees who have chronic conditions like diabetes, hypertension or thyroid disorders, who would otherwise struggle to get affordable individual cover.

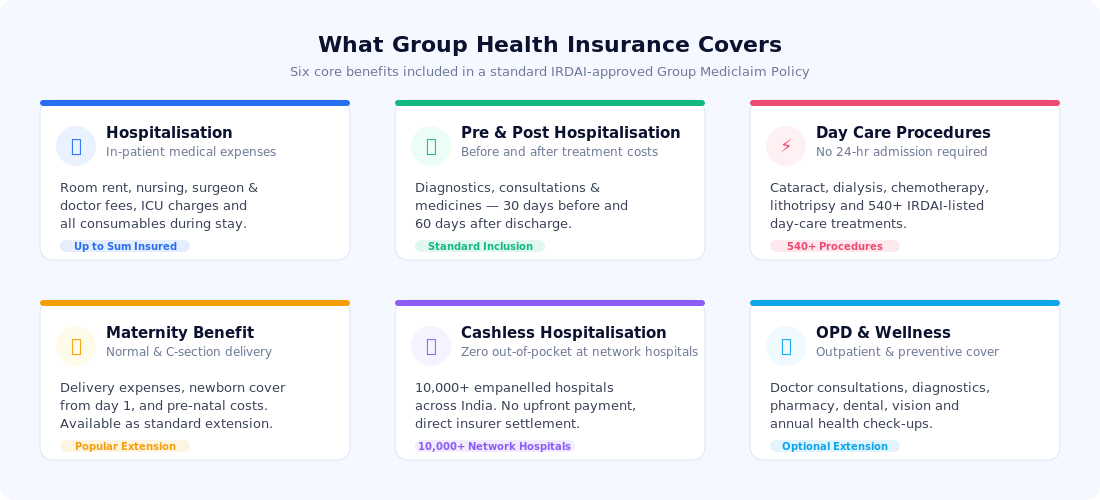

What Does a Group Health Insurance Policy Cover?

A standard IRDAI-approved Group Mediclaim Policy covers six core areas of healthcare expense, with a range of optional extensions that employers can add to build a more comprehensive benefit:

In-patient hospitalisation: Room rent, nursing charges, surgeon and anaesthetist fees, ICU charges, medicines, blood, oxygen and all consumables incurred during an admitted hospital stay of more than 24 hours.

Pre- and post-hospitalisation: Diagnostic tests, consultations and medicines incurred 30 days before admission and 60 days after discharge — covering the full episode of illness, not just the hospital stay.

Day care procedures: 540+ IRDAI-listed procedures that do not require 24-hour admission — including cataract surgery, dialysis, chemotherapy, lithotripsy and laparoscopic procedures.

Domiciliary treatment: Medical treatment taken at home when hospitalisation would otherwise have been required — relevant for elderly dependants or remote locations with limited hospital access.

Cashless hospitalisation: Direct billing between the insurer and any empanelled network hospital — 10,000+ hospitals across India — so the employee pays nothing out-of-pocket during a medical emergency.

Ambulance charges: Road ambulance costs for emergency transfers to hospital, typically up to ₹2,000–₹5,000 per event depending on the policy schedule.

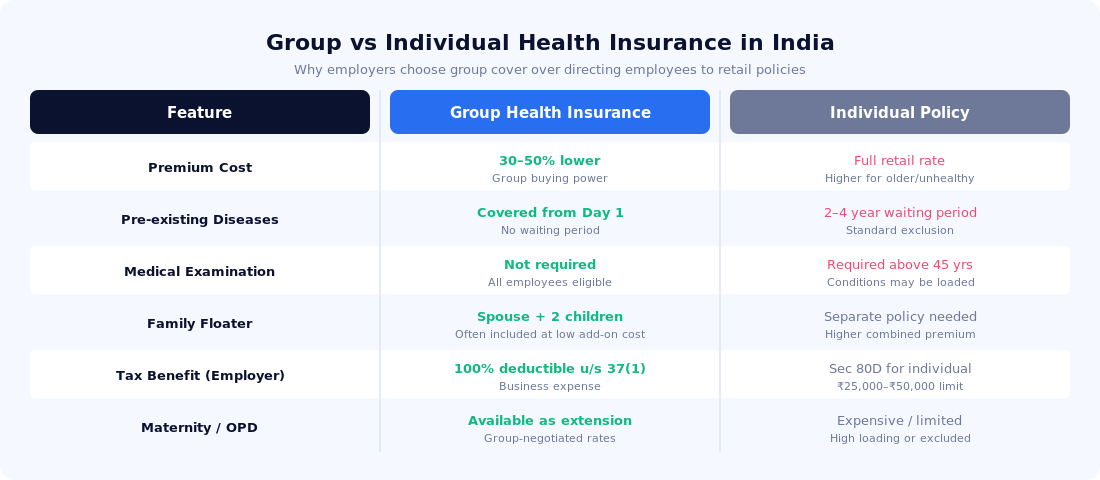

Group vs Individual Health Insurance — Why the Comparison Matters

Indian HR teams are frequently asked by employees: "Why can't you just give me a stipend so I buy my own policy?" The answer lies in the structural advantages that group buying delivers — advantages that are simply not available to an individual purchasing retail cover.

The most significant structural difference is the treatment of pre-existing diseases. A 42-year-old employee with Type 2 diabetes who tries to buy an individual policy will either face a loading of 30–50 percent on his premium or a two-to-four year exclusion on diabetes-related claims. Under a group policy, he is covered for diabetes from day one, at the same base premium as a 28-year-old without any health conditions. The insurer manages that adverse selection risk across the entire group, not individual by individual.

The second structural advantage is premium efficiency. A group of 100 employees buying cover collectively will typically pay 30–50 percent less per person than if each of those same individuals purchased equivalent individual cover. The insurer's administrative cost, distribution cost and adverse-selection risk are all lower in a group arrangement.

Key Benefits of Group Health Insurance for Indian Employers

Talent attraction and retention: FICCI-EY surveys consistently rank health cover among the top three factors influencing job acceptance decisions in India, alongside salary and job title. In sectors like IT, BFSI and pharma, the absence of group health cover is a disqualifier for many senior candidates.

Tax efficiency for the employer: Premiums paid by a company for employee group health insurance are fully deductible as a business expense under Section 37(1) of the Income Tax Act. For a company in the 22% tax bracket, a ₹50 lakh annual premium costs effectively ₹39 lakh after tax.

No GST on employee benefit: Employer-paid group health premiums are not treated as a taxable perquisite for employees, unlike many other non-cash benefits. The employee receives ₹5 lakh of health cover without it adding to their gross salary for tax purposes.

Productivity and morale: Employees who are not anxious about uninsured medical expenses are demonstrably more productive. A 2023 Aon Benefits Survey found that 68% of Indian employees said financial stress from healthcare costs affected their on-the-job focus.

Compliance and ESG: Several states' Shops and Establishments Acts and the ESIC framework require certain categories of employer to provide health coverage. Group health insurance supplements or replaces ESIC obligations and strengthens the company's ESG reporting on employee welfare.

Common Challenges and Things to Watch

Sum insured adequacy: Many Indian companies offer a sum insured of ₹2–3 lakh per employee, which was reasonable in 2015 but is insufficient in 2026. A single CABG (bypass surgery) in a Tier 1 city private hospital costs ₹4–7 lakh. Employers should review their sum insured benchmarks annually against medical inflation (12–15% per year in India).

Claims ratio and renewal loading: If a group's claims in Year 1 exceed 60–70% of premium, most insurers will apply a loading at renewal. HR teams should monitor claims frequency and severity during the year — not just at renewal — to anticipate and manage the renewal discussion.

Employee awareness gaps: Even well-designed group policies fail employees if no one knows how to use them. TPA helpline numbers, cashless hospital lists and pre-authorisation processes are often not communicated at onboarding. Companies with strong benefit utilisation programmes see 18–22% higher employee satisfaction scores.

Dependent definition: Standard policies cover spouse and up to two dependent children. Parents are excluded unless a specific "parents cover" extension is purchased — which typically adds 40–80% to the base premium depending on the parents' age band. Employees frequently discover this only at claim time.

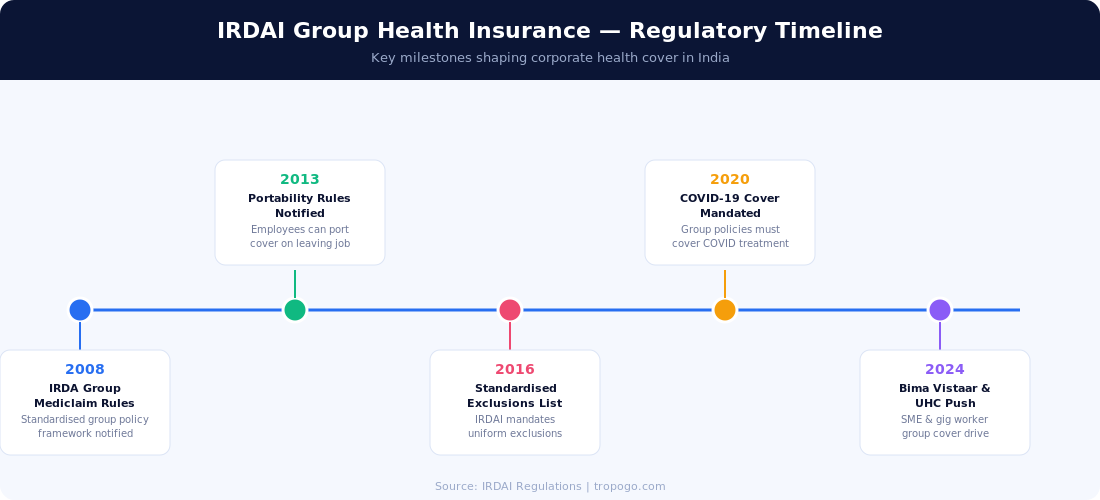

IRDAI Regulatory Framework — Key Milestones

Group health insurance in India operates under a well-established IRDAI regulatory framework that has evolved significantly over the past 15 years, most recently in the direction of standardisation, portability and wider access:

The most impactful recent development for Indian employers is the IRDAI's Bima Vistaar initiative, which aims to extend insurance access to the informal sector and SMEs. Under Bima Vistaar's architecture, group health cover is expected to be available as a standardised product for groups as small as five members — breaking the traditional floor of 20 employees that many insurers applied. This opens group health insurance to India's 63 million MSMEs, most of which currently provide no formal health coverage to their employees.

₹30,000+ croreIndia's group health insurance gross written premium in FY2024 — growing at ~20% annually as post-COVID awareness drives corporate health spend

Give your team the health cover they deserve

IRDAI-approved group health insurance for Indian companies of all sizes — startups to enterprises. No medical examination, pre-existing diseases covered from day one.

How to Structure a Group Health Insurance Programme

TropoGo's specialist group health insurance programme for Indian employers is built around six modules, each addressing a distinct coverage need:

Base hospitalisation cover (₹3–25 lakh sum insured): The core policy covering in-patient hospitalisation, day care procedures, pre/post-hospitalisation and ambulance. Sum insured should be benchmarked against current surgical procedure costs in the cities where your employees are based.

Family floater extension (spouse + 2 children): Adds dependant cover at a marginal additional premium — typically 40–60% above the base employee-only premium. The most cost-effective way for employees to insure their families compared to purchasing a separate retail policy.

Maternity benefit extension: Covers normal delivery (₹25,000–₹75,000 sub-limit) and C-section (₹50,000–₹1.5 lakh sub-limit), newborn cover from day one, and pre-natal OPD expenses. A 9-month or 12-month waiting period typically applies at inception.

OPD and wellness extension: Outpatient consultations, pharmacy, diagnostics, dental, vision and annual preventive health check-ups. Increasingly expected by employees in the IT and professional services sectors. Managed via an OPD wallet with a defined annual limit.

Critical illness top-up: A separate fixed-benefit layer that pays a lump sum (₹10–50 lakh) on diagnosis of listed conditions — cancer, stroke, heart attack, kidney failure, major organ transplant. Complements the hospitalisation base by providing income replacement during recovery.

Group personal accident extension: Covers accidental death, permanent total disability and permanent partial disability — providing financial protection for employees whose incomes are entirely dependent on their ability to work. Often added as a rider to the group health master policy at minimal incremental cost.

Outlook — What's Next for Corporate Health Benefits in India

Three trends will reshape group health insurance in India over the next three years. First, the rise of mental health benefits: IRDAI's 2023 guidelines require all health policies — including group policies — to cover mental illness treatment on par with physical illness. Progressive employers are building dedicated employee assistance programmes (EAPs) and therapy reimbursements into their group cover frameworks.

Second, the gig economy challenge: India's 7.7 million platform workers (cab drivers, delivery riders, freelancers) have no employer to aggregate them into a traditional group policy. Several insurtechs are building association-based group models that aggregate gig workers through platform companies, using Bima Vistaar's smaller group thresholds as the enabling regulatory structure.

Third, data-driven wellness: Insurers are beginning to price group renewals based not just on historical claims but on real-time wellness programme participation. Companies that can demonstrate lower claims through structured wellness interventions — step challenges, biometric screenings, dietary programmes — are negotiating 8–15% premium discounts at renewal. By 2027, wellness-linked group health pricing is expected to become mainstream in India's corporate insurance market.

Frequently Asked Questions

Is group health insurance mandatory for Indian companies?

There is no universal statutory mandate requiring all Indian employers to provide group health insurance. However, the Employees' State Insurance (ESI) Act requires employers with 10 or more employees earning below ₹21,000 per month to contribute to ESIC health coverage. For employees above this threshold — particularly in the IT, BFSI and professional services sectors — group health insurance is a market-driven expectation rather than a legal obligation. Several state-level Shops and Establishments Acts also impose health-related obligations on certain categories of employer.

How many employees do I need to qualify for a group health policy?

Most IRDAI-approved insurers will issue a group health policy for groups of 7 or more employees, though some products go as low as 5 members. The IRDAI's Bima Vistaar framework is expected to extend access to even smaller groups. Below a certain threshold (typically under 20 members), the policy may be treated as a group plan but priced with limited experience-rating flexibility. TropoGo structures group health programmes for companies of all sizes, including early-stage startups.

Are pre-existing diseases covered in a group health policy?

Yes — one of the most important structural advantages of group health insurance over individual retail policies. Under a standard IRDAI-approved group health policy, pre-existing diseases are covered from day one of the policy, without any waiting period. This includes chronic conditions like diabetes, hypertension, thyroid disorders, asthma and cardiac conditions. The insurer manages this exposure across the entire group rather than penalising individual members.

What happens to an employee's cover when they leave the company?

An employee's group health coverage ends on their last working day. However, under IRDAI's Health Insurance Portability guidelines, departing employees have the right to port their group cover to an individual or family floater policy without losing credit for waiting periods already served. This "portability on exit" right must be exercised within 30 days of leaving — after which the employee must undergo fresh underwriting as a new retail customer.

Can I include parents in my company's group health policy?

Yes, but it is an optional extension and typically the most expensive one. Parent cover adds 40–80% to the base premium, depending on the parents' age band. Many employers offer it as a voluntary benefit where the employee pays the additional premium through a payroll deduction. Some companies offer a tiered structure where they subsidise employee and spouse cover and offer parents cover at cost to the employee. IRDAI regulations do not place any restrictions on including parents as dependants in a group policy.

How do I get group health insurance for my company in India?

TropoGo offers IRDAI-approved group health insurance for Indian companies of all sizes — from 7-person startups to multi-location enterprises. Our programmes include base hospitalisation, family floater, maternity, OPD, critical illness and personal accident extensions — all tailored to your headcount, city locations, employee demographics and budget. Get a quote or speak to a specialist at TropoGo Group Health Insurance.

Group health insurance is no longer a benefit that progressive companies offer — it is the minimum that talented employees expect. In a country where a single hospitalisation can cost ₹3–10 lakh, leaving your team uninsured is not just a welfare failure: it is a retention and productivity risk with a measurable cost. TropoGo's specialist group health programme ensures your cover is correctly sized, correctly structured and correctly communicated — so it actually protects the people who build your business.