Imagine spending ten days in hospital after a surgery. Your health insurance covers the surgeon's fees, the room charges, and the medicines. But it doesn't pay your salary for those ten missed days. It doesn't cover your EMI that fell due on the fifth day. It doesn't put food on the table for your family while you're recovering. That gap — the income gap — is exactly what Hospicash insurance is designed to fill.

Hospicash insurance, also called Hospital Daily Cash Insurance, is a fixed-benefit health product regulated by the IRDAI that pays you a pre-agreed daily cash amount for every day you are hospitalised — regardless of your actual medical bills. The money lands directly in your bank account, no receipts required, no third-party verification of bills. It is arguably one of the simplest and most underutilised financial safety nets available to Indian families today.

What Exactly Is Hospicash Insurance?

Unlike a standard mediclaim or health insurance policy, which is an indemnity product (it reimburses actual expenses up to your sum insured), Hospicash is a defined-benefit product. You choose a daily benefit amount at the time of purchase — say ₹1,000 per day — and that amount is paid for every full day you remain hospitalised, irrespective of what the hospital charges you.

If you are admitted for six days, you receive ₹6,000. If you are in the ICU, most policies pay double the daily benefit — ₹2,000 per day in this example. Many policies also include a convalescence benefit — a lump sum paid at the end of a prolonged stay — and some include a bonus for every claim-free year.

The trigger is simple: hospitalisation of 24 hours or more. The document you need is equally simple: your discharge summary. There are no bills to collect, no itemised invoices to submit, no arguments about co-pays or sub-limits. The insurer calculates days × daily benefit and transfers the money.

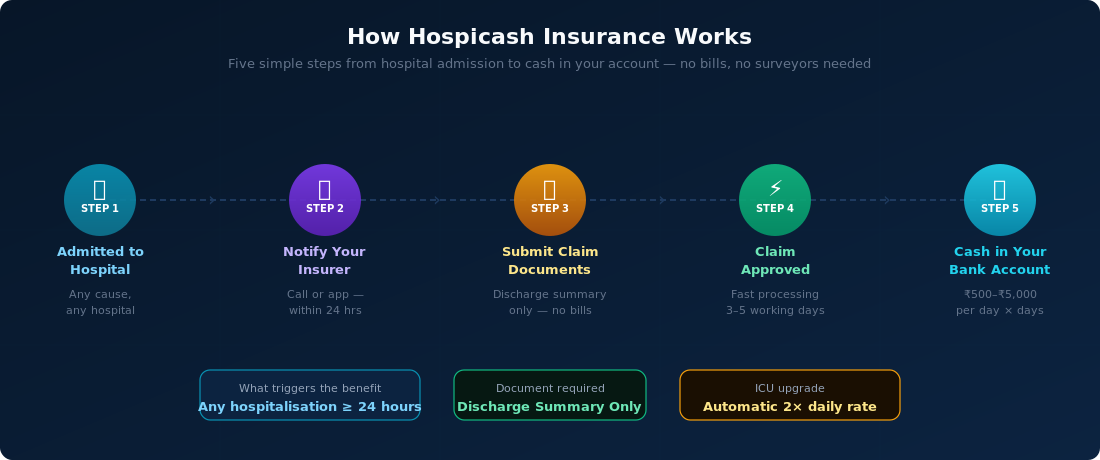

How Hospicash Insurance Works in Practice

The claims process is refreshingly straightforward for Indian policyholders used to navigating the complexity of cashless health claims:

Step 1 — Admission: You or a family member is admitted to any registered hospital in India for a condition covered under your policy (most causes are covered, including surgery, illness, and accidents).

Step 2 — Notify your insurer: Most insurers require notification within 24–48 hours of admission, either via their app, helpline, or website. This is a pre-authorisation step, not a cashless approval — it simply registers your claim.

Step 3 — Submit discharge summary: Once discharged, you submit your hospital discharge summary (the document summarising your diagnosis, treatment, and discharge date). No bills, no pharmacy receipts, no diagnostic reports.

Step 4 — Claim processed: The insurer counts the number of qualifying days (usually full calendar days from admission to discharge) and processes payment — typically within 3–5 working days.

Step 5 — Cash credited: The daily benefit × number of days is transferred directly to your registered bank account. ICU days are credited at the enhanced rate automatically.

The payout is yours to use however you need — pay your EMI, cover a family member's travel costs to be by your side, buy the medicines not covered by your health plan, or simply keep the household running while your income is paused.

What Hospicash Insurance Typically Covers

While policy terms vary by insurer, a standard IRDAI-approved Hospicash plan in India covers the following:

Daily cash benefit: A fixed amount — typically ₹500 to ₹5,000 per day — for every 24-hour period of hospitalisation.

ICU benefit: An enhanced rate (usually 2× the daily benefit) for days spent in the intensive care unit.

Convalescence benefit: A lump sum (often 5–10× the daily benefit) paid if hospitalisation exceeds a threshold — typically 10 or 15 continuous days.

Surgical benefit: Some plans pay an additional amount if a surgical procedure is performed during the stay.

Children's education bonus: A few comprehensive plans include a one-time education grant for dependent children if the policyholder is hospitalised for an extended period.

Ambulance benefit: A fixed reimbursement for ambulance costs incurred during the hospitalisation event.

The benefit period — the maximum number of days payable in a single hospitalisation and in a policy year — varies by plan. Entry-level plans may cap at 30 days per event and 60 days per year; premium plans can go up to 90 days per event and 180 days per year.

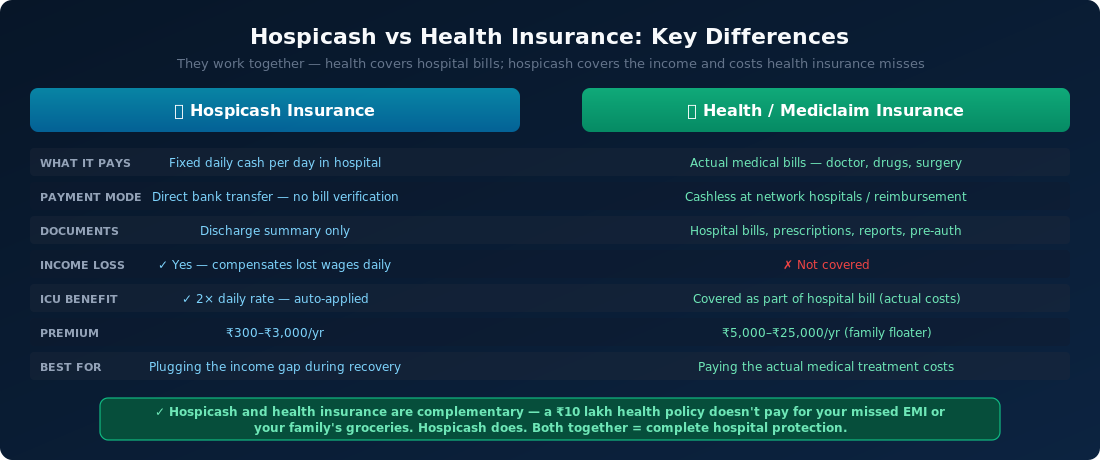

Hospicash vs Health Insurance: Why You Need Both

A common misconception is that a comprehensive health insurance policy makes Hospicash redundant. It does not — the two products solve fundamentally different problems.

Your mediclaim policy covers the hospital's invoice. When you leave the hospital, that invoice is settled — either through the cashless network or through reimbursement. But the following costs are never on the hospital invoice:

Your lost salary for the days you could not work.

A family member's travel and accommodation costs if they came from another city.

The cost of at-home nursing or physiotherapy during recovery after discharge.

The EMI that fell due while you were in the ward.

The items your health insurer excluded — consumables, diagnostic charges above limits, medicines not in the formulary.

Hospicash fills this gap. The daily cash is unrestricted — you spend it where the financial pressure is greatest. Think of it as your hospital pay cheque: it keeps arriving for as long as you are admitted, regardless of what your health insurer approves or rejects.

For self-employed professionals, daily wage workers, and small business owners, the income gap can be catastrophic. A week in hospital is a week of zero revenue. Hospicash at ₹2,000 per day over seven days means ₹14,000 — enough to cover a week of household expenses, loan EMI, or staff wages.

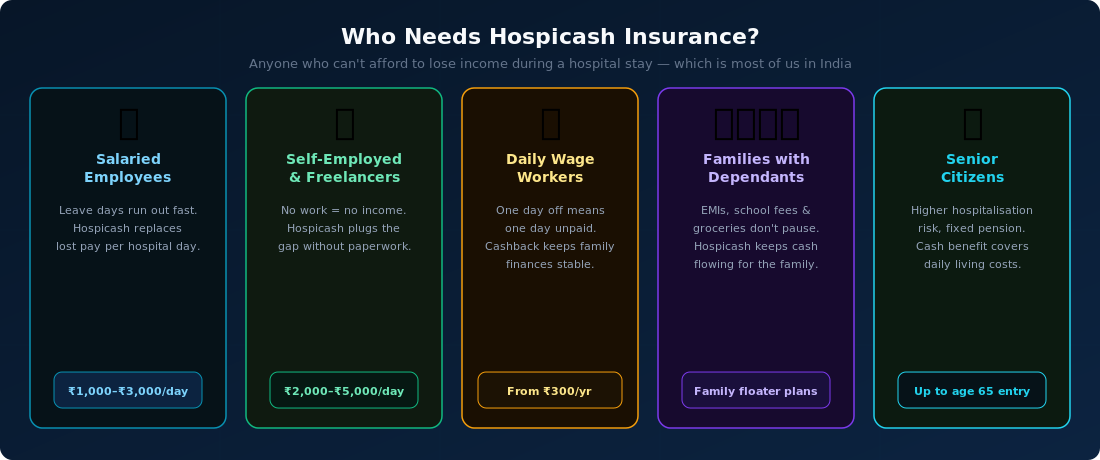

Who Needs Hospicash Insurance Most?

Hospicash is relevant to almost every earning adult in India, but it is essential for certain groups:

Salaried employees on paid leave: Most companies offer 10–15 days of sick leave. An extended hospitalisation burns through this quickly, and loss of pay can follow. Hospicash bridges the remaining income gap.

Self-employed and freelancers: No work means no income — with no sick leave to fall back on. Hospicash provides a guaranteed daily income stream through the stay.

Daily wage and gig workers: Even a two-day hospital stay means two days of zero earnings. A basic Hospicash plan at ₹500 per day costs as little as ₹300–₹500 per year — the most affordable income protection available.

Families with EMIs and dependants: School fees, home loan EMIs, and utility bills don't pause for medical emergencies. Cash in the bank keeps the household stable.

Senior citizens on pension: With a higher risk of hospitalisation and a fixed pension income, seniors benefit enormously from a guaranteed daily cash flow during illness or surgery.

Hospicash is also highly complementary to group health insurance provided by employers. Group policies often have room rent sub-limits, co-payments, or network hospital restrictions. Hospicash sidesteps all of these — it pays regardless of which hospital you chose or what your group policy approved.

How to Choose the Right Hospicash Plan

When comparing Hospicash plans from different IRDAI-regulated insurers in India, evaluate the following parameters:

Daily benefit amount: Choose an amount that at minimum covers your daily household expenses — typically 30–50% of your daily net income. Plans range from ₹500 to ₹5,000 per day.

ICU multiple: Verify whether ICU days are paid at 2× or 1.5×. Most standard plans pay 2×.

Waiting period: Most plans have a 30-day initial waiting period and a 1–2 year waiting period for pre-existing conditions. Ensure you check this before purchase.

Annual benefit cap: Look for plans with at least 90 days per event and 180 days per year, especially if you have a chronic condition.

Pre-existing disease cover: After the waiting period (usually 2–3 years), hospitalisation for pre-existing conditions should be covered. Confirm the PED waiting period explicitly.

Renewal age: Opt for plans that offer lifetime renewability. Plans that cap renewal at 65–70 leave you exposed exactly when hospitalisation risk is highest.

Standalone Hospicash plans are offered by most major Indian health insurers including Star Health, HDFC ERGO, Bajaj Allianz, Care Health, and Niva Bupa. Many insurers also offer Hospicash as an add-on rider to their base health or personal accident policies — often the most cost-effective route if you already have a base health plan.

Protect Your Income When Hospitalisation Strikes

TropoGo's Hospicash Insurance plans are IRDAI-regulated, straightforward to claim, and start from as little as ₹300 per year. Get daily cash paid directly to your bank for every day you spend in hospital — no bills, no arguments, no delays.

What is the minimum hospitalisation required to claim Hospicash?

Most IRDAI-approved Hospicash plans require a minimum continuous hospitalisation of 24 hours (one full day) to trigger a claim. Day-care procedures that do not require an overnight stay are generally not covered under standard Hospicash plans, though some premium products extend cover to day surgeries. Always confirm the minimum stay requirement in your policy wording before purchase.

Can I have both health insurance and a Hospicash policy simultaneously?

Yes — and you should. Health insurance and Hospicash are complementary products. Your health policy covers the actual medical bills (doctor fees, room rent, drugs, surgery). Hospicash covers your income loss and household expenses during recovery. Having both means you are financially protected on every front when hospitalisation occurs. Many people add Hospicash as a rider to their existing health or personal accident policy for maximum coverage at a lower combined premium.

Does Hospicash cover hospitalisation for pre-existing conditions?

Hospicash plans typically include a waiting period of 1–4 years before pre-existing diseases (PEDs) are covered. For example, if you have diabetes and are hospitalised for a diabetes-related condition within the first two years of the policy, that claim may be declined. After the PED waiting period has passed, all covered conditions — including pre-existing ones — trigger the daily benefit. The initial waiting period (usually 30 days) applies to all conditions, including new illnesses.

How much daily benefit should I choose?

A common rule of thumb is to choose a daily benefit equal to 30–50% of your daily net income. If you earn ₹50,000 per month, your daily income is roughly ₹1,667 — a daily benefit of ₹1,000–₹1,500 is appropriate as a baseline. Factor in your fixed monthly obligations (EMI, school fees, rent) and divide by 30 to find the minimum daily benefit needed to keep those obligations funded during a hospital stay. Higher-benefit plans (₹3,000–₹5,000 per day) are worth considering for urban professionals with higher fixed costs.

Is Hospicash insurance available for senior citizens?

Yes, most major Indian health insurers offer Hospicash plans for individuals up to 65 years of age at entry, with lifetime renewability thereafter. Senior citizens benefit most from Hospicash because their hospitalisation risk is significantly higher, their recovery periods are longer, and their income (typically pension) is fixed and limited. ICU benefits at 2× the daily rate are particularly valuable for seniors, who are more likely to require intensive care during hospitalisation. Premiums are higher for older entry ages but remain affordable compared to standard health insurance for seniors.

How do I get the best Hospicash plan for my needs in India?

TropoGo's specialist advisors compare IRDAI-regulated Hospicash plans from all major Indian insurers — including daily benefit amounts, ICU multiples, waiting periods, and renewal terms. Rather than navigating dozens of policy documents yourself, get a comparison tailored to your income, existing health cover, and family obligations. Explore Hospicash plans with TropoGo and get covered in minutes.

Don't let a hospital stay drain your savings, miss your EMIs, or leave your family financially stranded. Hospicash insurance is the simplest, most affordable income protection you can add to your financial plan — and it costs less than a monthly mobile recharge.