What is Directors & Officers (D&O) Liability Insurance?

Directors and Officers (D&O) liability insurance is a management liability policy that protects the individual directors, officers, and senior executives of a company from personal financial loss arising from claims of wrongful acts committed in their capacity as corporate decision-makers. When a shareholder sues your board for a business decision that eroded the company's value, when SEBI investigates a director for disclosure violations, or when the Resolution Professional pursues a former director under the Insolvency and Bankruptcy Code (IBC), D&O insurance steps in to fund legal defence costs, settlements, and court-ordered compensation — protecting the personal assets of the individuals named.

Unlike Commercial General Liability (CGL), which covers physical injury and property damage to third parties, D&O covers the financial consequences of alleged wrongful management decisions. And unlike property or vehicle insurance, D&O's most important feature is the protection it extends to individuals personally — not just to the company entity.

In India, D&O exposure has grown dramatically over the last decade. The Companies Act 2013, SEBI's Listing Obligations and Disclosure Requirements (LODR) regulations, the IBC 2016, and increasingly activist shareholders have collectively created an environment where being a director of an Indian company — listed or unlisted — carries meaningful personal financial risk. A well-structured D&O policy is no longer a luxury for large corporates. It is a fundamental component of responsible corporate governance.

The Three Sides of a D&O Policy: Side A, B and C

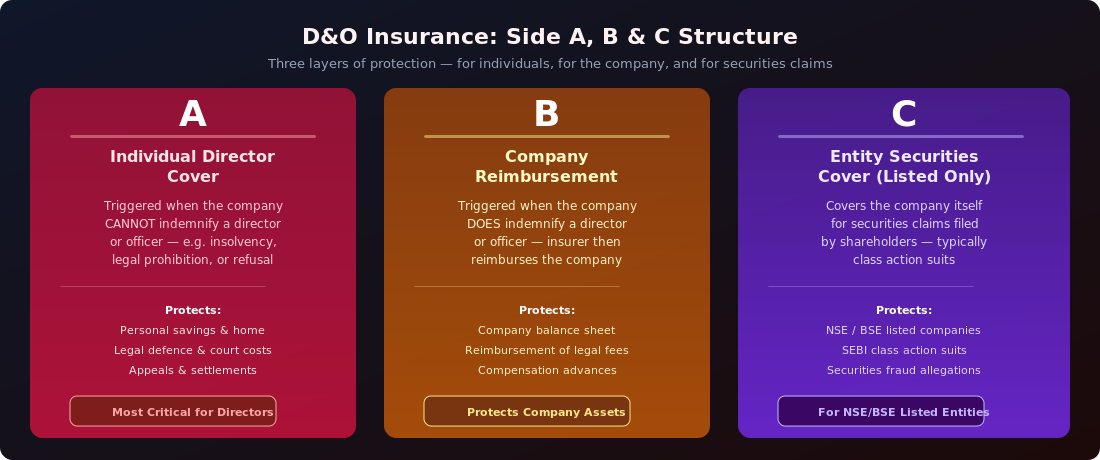

D&O insurance is structured in three distinct coverage sections, each triggered by different circumstances. Understanding which "side" applies in any given claim situation is essential for both individual directors and company risk managers.

Side A — Individual Director Cover is the most critical section for a director personally. It is triggered when the company cannot indemnify a director or officer — because the company is insolvent, legally prohibited from indemnifying, or refuses to do so. Side A pays defence costs and compensation directly to the individual, protecting their personal savings, home, and family assets from being used to satisfy a judgment. For any director sitting on an Indian board, Side A is the section that truly matters at a personal level.

Side B — Company Reimbursement is triggered when the company does indemnify a director or officer. In these cases, the company pays the director's legal costs and then seeks reimbursement from the D&O insurer. Side B protects the company's balance sheet from being depleted by the cost of defending its leadership against lawsuits.

Side C — Entity Securities Cover applies only to listed companies and covers the company entity itself against securities claims filed by shareholders — typically class action suits alleging misleading disclosures or market manipulation. In India, with SEBI's growing enforcement activity on NSE and BSE-listed companies and the increasing use of class action remedies under the Companies Act 2013, Side C has become an important component of D&O for listed Indian companies.

What Events Trigger D&O Claims in India?

India's legal and regulatory environment creates a wide range of scenarios where directors face personal liability. These are not theoretical risks — they are documented, recurring scenarios that TropoGo's D&O specialists encounter in the Indian market.

Breach of fiduciary duty is the most common D&O trigger globally and in India. Under Section 166 of the Companies Act 2013, directors owe specific fiduciary duties to the company and its shareholders — to act in good faith, avoid conflicts of interest, and not exploit corporate opportunities. When a director approves a related-party transaction at above-market rates, acquires a business in which they hold a personal interest, or votes against an acquisition that would benefit all shareholders to protect their own position, they expose themselves to personal liability under Section 166 and to shareholder derivative suits.

SEBI investigations have become an increasingly significant D&O risk for directors of listed Indian companies. SEBI's enforcement division regularly issues show-cause notices to individual directors for alleged insider trading, misrepresentation in IPO documents (DRHP), failure to make timely disclosures under LODR, and violations of the SEBI (Prohibition of Insider Trading) Regulations 2015. Even when a company-level violation is found, SEBI often proceeds against the specific directors who were in charge during the period of violation — making personal D&O coverage essential.

IBC and insolvency claims have emerged as one of the most significant D&O exposures for Indian directors since 2016. When a company enters insolvency proceedings, the Resolution Professional (RP) appointed by the National Company Law Tribunal (NCLT) has the power to investigate the conduct of former directors. Directors found to have made fraudulent transfers, engaged in preferential payment to related parties, or concealed company assets face personal liability under Sections 66 and 67 of the IBC. Lenders and operational creditors may also pursue former directors personally.

Ministry of Corporate Affairs (MCA) and ROC inquiries are a perennial risk for directors of Indian companies. The Registrar of Companies routinely investigates directors for non-compliance with the Companies Act 2013 — including failure to file annual returns, breaches of the disclosure requirements for related-party transactions, and violations of board meeting attendance requirements. In serious cases, MCA can initiate prosecution of individual directors, which requires expensive legal defence regardless of outcome.

Employment practices liability — particularly claims under the POSH Act (Sexual Harassment of Women at Workplace Act, 2013) — is a growing D&O exposure for Indian companies. Senior executives personally named in harassment complaints, or directors who are found to have failed in their statutory obligation to constitute an Internal Complaints Committee (ICC), face personal liability and reputational risk. D&O policies with Employment Practices Liability (EPL) extensions cover these claims.

Tax and GST personal liability is a frequently overlooked D&O risk in India. Section 179 of the Income Tax Act and Section 89 of the CGST Act both contain provisions that hold directors personally liable for tax defaults of the company if they were in charge of the company's affairs during the period of default. The Income Tax department and GST authorities can — and do — pursue individual directors for recovery of unpaid tax dues, making this a real, quantifiable personal financial risk.

Who Needs D&O Insurance in India?

The short answer: any individual who sits on a board of directors or holds an officer-level position in an Indian company should be covered by D&O insurance. The risk profile varies significantly by company type and sector.

NSE and BSE listed companies face the broadest D&O exposure. SEBI's enforcement activity has intensified significantly post-2019: the regulator's annual enforcement reports show hundreds of show-cause notices issued to directors annually. Listed company directors also face shareholder class action suits — a mechanism available under Section 245 of the Companies Act 2013 — and continuous disclosure obligations under LODR that create ongoing compliance-related personal liability. All three D&O sides (A, B, and C) are appropriate for listed entities.

PE and VC-backed startups are among the fastest-growing buyers of D&O insurance in India. Most institutional investors — Sequoia Capital, Accel, Softbank, Tiger Global — include D&O insurance as a standard condition of their investment term sheets. Founder-directors, independent directors, and investor-nominated board members all need protection. As Indian startups approach IPO, D&O exposure increases substantially because the IPO process — including DRHP preparation — creates SEBI-related personal liability for directors.

Large private companies with significant debt obligations, turnover above ₹100 crore, or complex related-party structures face meaningful IBC and creditor exposure. The IBC has been used extensively since 2016, and the personal liability provisions of the Code have been actively invoked against directors of companies admitted to the Corporate Insolvency Resolution Process (CIRP). Private companies with bank debt — particularly those in cyclical sectors like real estate, infrastructure, and manufacturing — should treat D&O as non-negotiable.

Banks, NBFCs, and fintech companies face dual regulatory exposure — from RBI for prudential and governance violations, and from SEBI for those that are listed. RBI's Prompt Corrective Action (PCA) framework and its enforcement of fit-and-proper director criteria create specific personal liability risks for banking directors. Post-pandemic NPA pressures have led to increased personal scrutiny of credit decision-makers.

Government-owned enterprises and PSUs require a different D&O structure — typically through government-backed indemnity arrangements supplemented by commercial D&O for government-appointed independent directors who lack personal indemnity from the state. CAG scrutiny, parliamentary committee investigations, and CBI inquiries create meaningful personal liability for directors of CPSEs and state-level enterprises.

What Does a D&O Policy Not Cover?

Understanding D&O exclusions prevents coverage gaps and avoids claim disputes. Standard D&O policies in India exclude the following categories of claims:

Fraud and dishonesty — if a court or regulatory authority establishes that a director committed actual fraud or deliberate dishonest conduct, D&O coverage is excluded. However, critically, D&O covers legal defence costs until fraud is actually proven — not merely alleged.

Personal profit — claims arising from a director's illegal personal gain (e.g., receiving secret commissions or bribes) are excluded once the illegal profit is judicially confirmed.

Prior claims and known circumstances — claims arising from circumstances known to the insured before the policy inception date are typically excluded under D&O's "claims-made" structure.

Bodily injury and property damage — physical injury and property damage claims are covered under CGL, not D&O.

Insured vs. insured — claims brought by one insured director against another (e.g., a board faction suing another) are generally excluded, though exceptions exist for certain employment-related claims.

Pollution liability — environmental contamination claims require a separate Environmental Liability policy.

D&O Insurance and Corporate Governance in India

SEBI's Corporate Governance framework — particularly its requirements for independent directors under LODR — has made D&O insurance a governance priority for Indian listed companies. Independent directors are particularly vulnerable to D&O claims because they typically lack the indemnity protections that executive directors receive through employment contracts. In 2020, the resignation of multiple independent directors from listed Indian companies citing inability to obtain adequate D&O coverage highlighted how critical the policy has become for board quality.

Under Section 197(13) of the Companies Act 2013, companies are permitted to pay D&O insurance premiums for their directors — and these premiums are not treated as managerial remuneration. SEBI's LODR regulations require listed companies to disclose D&O insurance arrangements in their annual reports. The National Stock Exchange (NSE) and Bombay Stock Exchange (BSE) have both incorporated D&O insurance into their corporate governance guidelines.

For Indian companies attracting international investors, D&O is increasingly a minimum governance threshold — foreign institutional investors (FIIs) and global private equity funds routinely check D&O coverage as part of due diligence before board appointment or investment.

TropoGo's D&O Insurance for Indian Boards

TropoGo specialises in structuring D&O programmes for Indian companies at every stage — from pre-IPO startups to NSE/BSE-listed corporates to aviation and specialty sector boards. Our D&O products provide the following specialist covers for Indian directors and officers:

Side A standalone cover — pure individual director cover, functioning independently of the company policy and providing direct protection when the company cannot or will not indemnify.

Side B company reimbursement — reimbursing the company when it indemnifies directors, protecting the company's balance sheet from management defence costs.

Side C entity securities cover — for listed companies, covering SEBI class action suits and shareholder securities claims against the company entity.

Employment Practices Liability (EPL) extension — covering POSH Act claims, wrongful termination suits, and workplace discrimination allegations against senior management.

Regulatory investigation cover — advancing defence costs for SEBI, MCA, RBI, IRDAI, CCI, and Income Tax investigations, even before any formal legal proceeding is initiated.

IBC / insolvency cover extension — specifically structured to respond to claims brought by Resolution Professionals and creditors under the Insolvency and Bankruptcy Code 2016.

Is Your Board Protected From Personal Liability?

TropoGo structures D&O programmes for listed companies, PE-backed startups, private firms and specialty sectors — including aviation and financial services boards across India.

D&O is not legally mandatory for most Indian companies, but it is effectively required in several situations. SEBI's LODR regulations encourage listed companies to disclose D&O arrangements. Most institutional investors (PE, VC) require D&O as a condition of investment. Independent directors of listed companies increasingly refuse board appointments without adequate D&O coverage, given the personal liability exposure under the Companies Act 2013 and SEBI regulations.

What is the difference between Side A and Side B D&O coverage?

Side A covers individual directors directly when the company cannot or will not indemnify them — for example, when the company is insolvent or when indemnification is legally prohibited. It is the most personal and critical section of a D&O policy. Side B covers the company itself when it indemnifies a director — the insurer reimburses the company for costs it has paid on behalf of the director. Both sections typically operate within the same policy limit, though standalone Side A-only policies with separate limits are available for independent directors.

Does D&O cover SEBI investigations and regulatory proceedings?

Yes. Standard D&O policies in India cover legal defence costs for SEBI investigations, show-cause notices, and adjudication proceedings. Many policies also cover MCA, RBI, IRDAI, CCI, and Income Tax investigations. Importantly, D&O covers defence costs from the point of investigation — not just when a formal prosecution or civil lawsuit is filed. This "investigation cost" cover is particularly valuable in India because regulatory investigations frequently precede formal legal proceedings by months or years.

Can independent directors of Indian listed companies get D&O coverage?

Yes — and independent directors should insist on D&O coverage before accepting board appointments. Unlike executive directors, independent directors typically lack employment contracts that provide indemnification, making Side A D&O coverage particularly important. Many institutional investors and governance advocates recommend that independent directors seek written confirmation of D&O policy terms — including the limit, insurer credit rating, and Side A availability — before joining a listed company board in India.

Does D&O cover claims under the Insolvency and Bankruptcy Code (IBC)?

Standard D&O policies cover claims brought by Resolution Professionals or creditors against former directors for wrongful conduct during the period leading up to insolvency — including fraudulent trading (Section 66 IBC) and preferential transactions (Section 43 IBC). However, if actual fraud is proved in court, D&O coverage terminates for that specific director. TropoGo's D&O products include specific IBC exposure endorsements tailored to India's insolvency landscape.

How much D&O insurance does my company need and how do I get a quote?

D&O limits in India typically range from ₹5 crore to ₹100 crore for unlisted companies, and USD 10–50 million for listed companies — depending on market capitalisation, sector, debt level, and regulatory exposure. Premium rates vary significantly by company profile. TropoGo's specialists can assess your board's specific liability exposure and source competitive D&O quotes from leading Indian and international insurers. Visit our D&O insurance page to learn more.

Every director and officer of an Indian company — from a listed conglomerate to a PE-backed startup — carries personal financial risk that extends to their own assets. A D&O policy is not just an insurance purchase; it is a governance commitment that protects the quality of your board, enables the recruitment of strong independent directors, and demonstrates to investors, lenders, and regulators that your company takes corporate accountability seriously.