Every time you take your car, bike or truck out on an Indian road, you're legally required to carry one thing beyond your driving licence: a valid motor insurance policy. Yet millions of vehicle owners treat insurance as a box-ticking exercise, buying the cheapest third-party cover they can find and never thinking about it again — until an accident forces them to.

India's roads recorded over 1.68 lakh road accident deaths in 2024, according to the Ministry of Road Transport and Highways. Behind each statistic lies a family dealing with loss, repair bills, or a protracted legal battle. Motor insurance is the financial layer that separates a manageable crisis from a catastrophic one — for you, your family, and the third party involved.

What is Motor Insurance?

Motor insurance is a contract between you and an insurer: you pay a premium, and in return the insurer covers specified financial losses arising from your vehicle — damage, theft, or liability to a third party. In India, the legal framework is the Motor Vehicles Act, 1988, which makes third-party (TP) insurance compulsory for every vehicle using a public road. The Insurance Regulatory and Development Authority of India (IRDAI) regulates all motor insurance products, sets TP premium rates, and mandates minimum cover limits.

Unlike health or life insurance, motor insurance covers an asset — your vehicle — and the liabilities it can create. It bridges the gap between the cost of an accident and what you can reasonably afford to pay out of pocket.

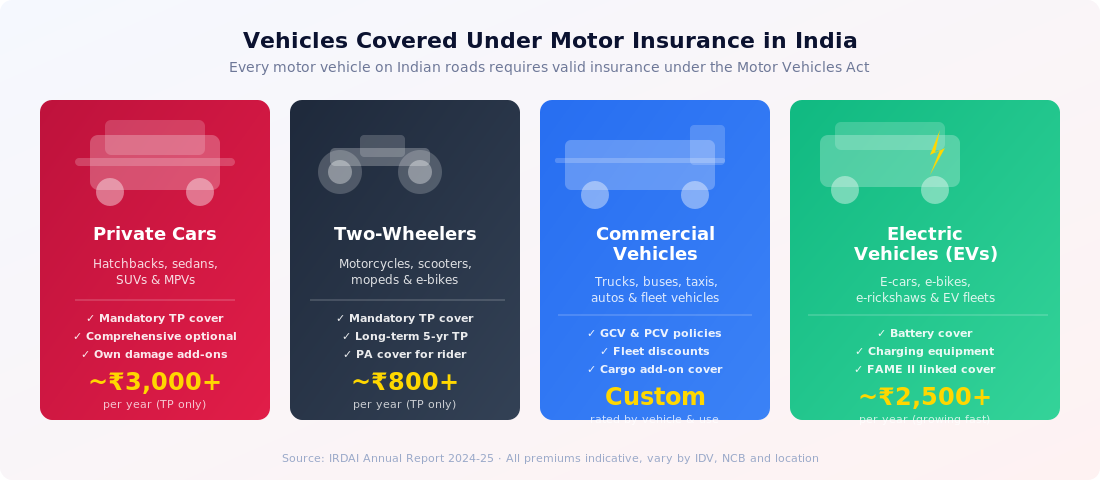

Types of Vehicles Covered Under Motor Insurance

The Motor Vehicles Act applies to every mechanically-propelled vehicle on Indian roads. That means private cars, two-wheelers (motorcycles, scooters, e-bikes), commercial goods vehicles (trucks, tempos, pick-ups), passenger-carrying vehicles (buses, taxis, auto-rickshaws), and the rapidly growing category of electric vehicles. Each segment has its own policy structure and premium band.

The Two Core Policy Types

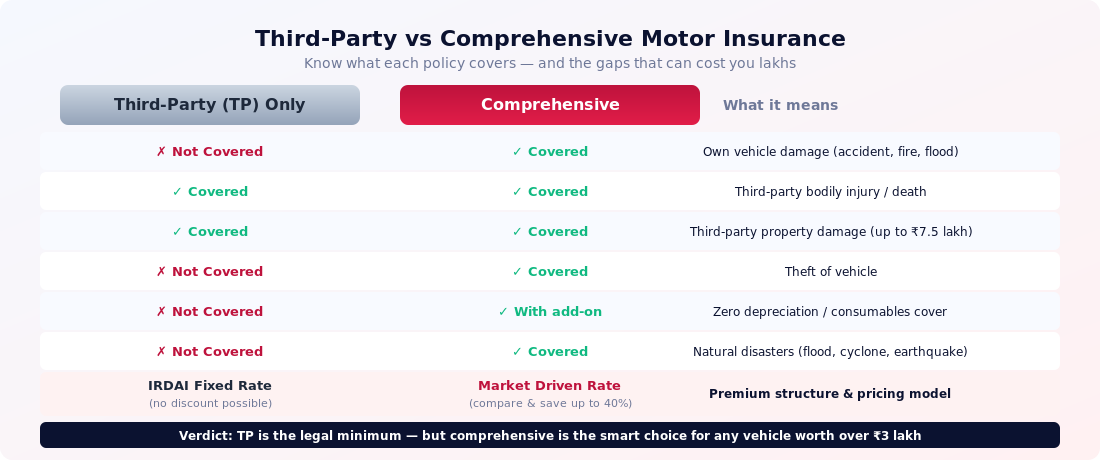

All motor insurance products in India rest on two foundations: third-party (TP) cover and own-damage (OD) cover. TP cover is mandatory; OD is optional but strongly advisable for any vehicle with meaningful market value.

Third-Party Only (TP): Covers your legal liability for injury, death, or property damage caused to a third party. IRDAI fixes TP premiums annually — you cannot shop around on price for this component.

Comprehensive (TP + OD): Combines mandatory TP cover with protection for your own vehicle — from accidents, fire, flood, earthquake, cyclone, theft, and vandalism. OD premiums are market-driven, so comparing insurers can save you 20–40%.

Standalone OD Policy: Introduced by IRDAI in 2019, this lets you decouple OD cover from TP — useful if your TP is bundled into a long-term policy from a dealership but you want to switch OD insurers.

Key Add-On Covers Worth Knowing

A comprehensive base policy covers a lot, but add-ons let you patch the gaps that matter most for your vehicle and how you use it. The most popular add-ons in India include:

Zero Depreciation (Nil Dep): Eliminates depreciation deductions at claim time — critical for vehicles under 5 years old where parts depreciate fast.

Engine & Gearbox Protection: Standard policies exclude engine damage from water ingression (a very real risk during Mumbai or Chennai monsoons). This add-on fills that gap.

Return to Invoice (RTI): In a total loss or theft, your insurer pays the original purchase invoice value, not the depreciated IDV.

Roadside Assistance (RSA): 24/7 helpline for towing, flat tyres, fuel delivery, and lockout — particularly valuable on highways or late at night.

Consumables Cover: Pays for nuts, bolts, engine oil, coolant and other consumables replaced during repairs — normally excluded from base policies.

Personal Accident (PA) Cover: ₹15 lakh PA cover for the owner-driver is now compulsory. You can extend it to unnamed passengers as an add-on.

How Motor Insurance Premiums Are Calculated

Your premium has two components. The TP premium is IRDAI-fixed and depends only on your engine displacement (for private cars) or gross vehicle weight (for commercial vehicles). The OD premium is based on your vehicle's Insured Declared Value (IDV) — essentially its current market value after depreciation — multiplied by the insurer's base rate, then adjusted for your No-Claim Bonus (NCB), add-ons, and any applicable discounts.

NCB is the single biggest lever a careful driver has. You earn a discount on OD premium for every claim-free year: 20% after year one, scaling up to 50% after five consecutive claim-free years. A 50% NCB on a comprehensive policy for a mid-segment car can save you ₹4,000–₹8,000 per renewal — worth protecting by not claiming for minor scratches or small dents.

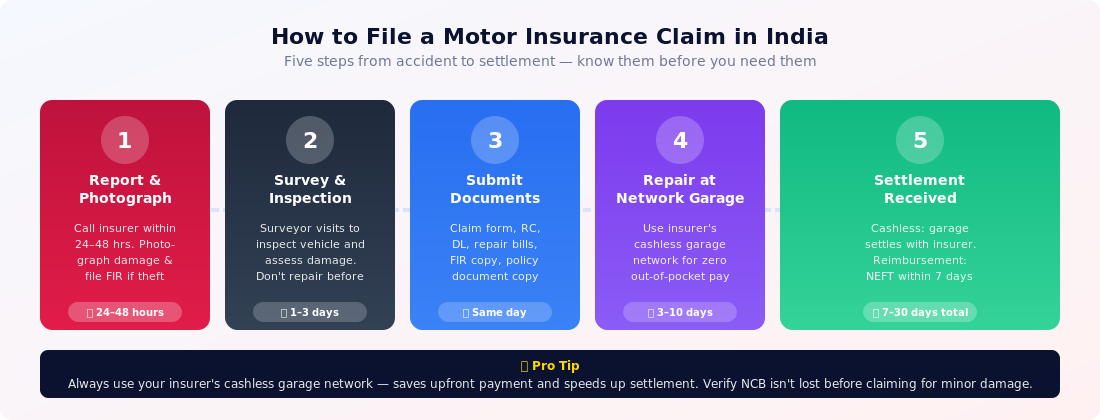

The Claims Process: What to Expect

Motor insurance claims in India follow a well-defined path. Understanding it in advance removes the stress of navigating it after an accident.

The key principle is to notify your insurer within 24–48 hours of an incident. For theft, you must also file an FIR and provide a copy to the insurer. For cashless claims, stick to the insurer's authorised garage network — this eliminates upfront payment and typically speeds up settlement significantly.

Motor Insurance for Electric Vehicles

EV insurance follows the same legal framework but has important differences. IDV calculation must include the battery pack (by far the most expensive component). Several insurers now offer battery-specific cover addressing degradation and accidental damage. IRDAI's 2023 circular clarified that EV batteries can be covered either as part of the vehicle IDV or under a separate add-on, giving policyholders flexibility. As India's EV fleet crosses 5 crore registered vehicles, EV-specific products from insurers like HDFC Ergo, Bajaj Allianz, and Tata AIG are becoming more nuanced and competitive.

IRDAI Regulations You Should Know

India's motor insurance landscape is tightly regulated. Key rules that directly affect you as a vehicle owner include:

Mandatory TP cover: Driving without valid TP insurance carries a fine of ₹2,000 for the first offence and ₹4,000 for repeat offences under the 2019 Motor Vehicles Amendment Act.

Long-term TP policies: Since September 2018, new private cars must carry a 3-year TP policy and new two-wheelers a 5-year TP policy at time of purchase.

Compulsory PA cover: Owner-drivers must carry a ₹15 lakh Personal Accident cover (or be covered under a stand-alone PA policy).

Third-party property damage cap: TP property damage liability is currently capped at ₹7.5 lakh per incident.

NCB portability: Your NCB follows you when you switch insurers at renewal — it belongs to the owner, not the policy.

Is Your Vehicle Covered the Right Way?

Third-party insurance is the minimum — but it won't pay a rupee when your own vehicle is damaged or stolen. TropoGo's motor insurance specialists help you compare comprehensive policies, protect your NCB, and get the right add-ons for Indian road conditions.

Most Indian vehicle owners buy insurance to avoid a challan. The smarter framing is risk transfer: you're paying a known premium to eliminate an unknown, potentially ruinous liability. A single accident on a busy urban road can generate third-party injury claims of ₹25–₹50 lakh at the Motor Accident Claims Tribunal (MACT). Without a valid TP policy, that liability is yours personally.

A comprehensive policy with the right add-ons goes further — protecting your vehicle's value, covering monsoon flood damage (increasingly common across Indian metros), and ensuring that a stolen vehicle doesn't leave you with a loan to repay on a vehicle you no longer own.

TropoGo's motor insurance platform covers the full spectrum of motor vehicles with specialist products for private cars, two-wheelers, commercial fleets, and electric vehicles. Key covers include:

Mandatory Third-Party Liability: Legally compliant TP cover with IRDAI-regulated premiums for all vehicle categories.

Comprehensive Own Damage: Accidental damage, fire, flood, earthquake, cyclone, theft and malicious acts — protecting your vehicle's full IDV.

Zero Depreciation Cover: Full parts replacement value at claim time — no deductions for depreciation on your vehicle's components.

Engine & Gearbox Protect: Covers hydrostatic lock and consequential damage from water ingression during monsoon flooding.

EV Battery Cover: Dedicated protection for EV battery packs including accidental damage and manufacturing defect coverage.

Fleet & Commercial Cover: Tailored GCV and PCV policies for commercial operators with fleet discounts and driver PA cover.

Frequently Asked Questions

Is motor insurance mandatory for all vehicles in India?

Yes. The Motor Vehicles Act, 1988, makes third-party insurance compulsory for every mechanically-propelled vehicle operating on a public road — private cars, two-wheelers, three-wheelers, commercial vehicles, and electric vehicles alike. Driving without valid TP insurance is a punishable offence with fines of up to ₹4,000 and possible suspension of driving licence.

What is the difference between third-party and comprehensive motor insurance?

Third-party (TP) insurance covers your legal liability for injury, death or property damage caused to others — it does not pay for damage to your own vehicle. Comprehensive insurance combines TP cover with own-damage (OD) cover, protecting your vehicle against accidents, theft, fire, flood, and natural calamities. Comprehensive premiums are market-driven, so comparing quotes can save you 20–40%.

What is IDV and how does it affect my premium?

IDV (Insured Declared Value) is the current market value of your vehicle after depreciation — essentially the maximum amount your insurer will pay in a total loss or theft claim. A higher IDV means better protection but a slightly higher OD premium. Underinsuring your vehicle to save on premium can leave you short by lakhs at claim time. Always insure at the correct IDV.

What is No-Claim Bonus (NCB) and can I transfer it?

NCB is a discount on your OD premium for each claim-free year — starting at 20% after year one and scaling to 50% after five claim-free years. It belongs to the policyholder (not the vehicle), so you can transfer it when buying a new car or switching insurers. NCB is lost if you make a claim, which is why many owners pay small repairs out-of-pocket to protect it.

Does motor insurance cover flood damage during monsoon?

A standard comprehensive policy covers damage from natural calamities including floods, cyclones, and earthquakes. However, engine damage caused by water ingression (hydrostatic lock) is typically excluded from the base policy. To cover this common monsoon risk in cities like Mumbai, Chennai, and Bengaluru, you need an Engine & Gearbox Protection add-on. Check your policy schedule carefully.

How do I choose the right motor insurance policy in India?

Start with your vehicle's age and value. For new vehicles under 5 years old, comprehensive cover with zero depreciation and engine protection add-ons makes financial sense. For older vehicles worth under ₹2 lakh, basic TP-only may suffice. Always compare OD premiums from at least 3 insurers (TP rates are fixed), check the cashless garage network in your city, and review the claim settlement ratio before buying. TropoGo's motor insurance page makes comparison quick and jargon-free.

Motor insurance isn't just a legal requirement — it's the foundation of financial safety for every Indian vehicle owner. Whether you drive a hatchback in Gurugram, run a fleet of trucks in Rajasthan, or recently bought an electric car in Pune, the right policy protects both your asset and your liability exposure. Don't wait for an accident to find out you're underinsured.