What is Theft and Burglary Insurance and Who Needs It?

20 May 2026 | 7 min read

Protect your stock, cash and premises — specialist theft and burglary cover for India's retailers, jewellers and businesses

From neighbourhood kirana stores to large warehouses — IRDAI-approved all-risk cover against theft, burglary, robbery and cash losses across India's ₹13 lakh crore retail sector.

India's retail sector crossed ₹13 lakh crore in annual turnover in 2024, and it shows no signs of slowing. From Mumbai's Zaveri Bazaar and Delhi's Chandni Chowk to single-owner kiranas and sprawling warehouse parks on the outskirts of Pune and Chennai, Indian businesses hold vast quantities of stock, cash and equipment every single day. And every single day, thousands of those businesses lose some of it to theft, burglary or robbery — often without any meaningful financial protection.

The National Crime Records Bureau (NCRB) reported more than 3.8 lakh property-crime cases across Indian cities in 2023 alone, and industry surveys suggest actual losses — including unreported incidents — are several times higher. Yet fewer than 12 percent of Indian SMEs carry a standalone theft and burglary policy. For most, the first theft is also the last lesson: stock gone overnight, a cash drawer cleaned out, a smashed showcase in a jewellery shop on a Monday morning.

Theft and burglary insurance is the specialist cover designed for exactly this exposure. It pays to replace or restore whatever was stolen or damaged during a break-in, and it extends to cash-in-safe, cash-in-transit, fixtures and the structural damage that accompanies most forced entries. This guide explains what the policy covers, who needs it most in India, and how to choose the right sum insured before the loss happens — not after.

What is Theft and Burglary Insurance?

Theft and burglary insurance is a property-specific policy that indemnifies a business against the loss of stock, cash, trade equipment, fixtures and fittings caused by theft, burglary, robbery, housebreaking or any attempted version of these acts. Unlike a standard fire policy — which covers destruction by fire or allied perils — a theft policy responds to the specific peril of a person unlawfully taking or attempting to take property, with or without the use of force.

In India, the policy is governed by the IRDAI standard wordings and is typically issued either as a standalone theft and burglary policy or as part of a broader Standard Fire and Special Perils + Burglary package. The insurer pays the market value of stolen goods (or reinstatement cost if agreed at inception), the cost of repairing damage done to the building during forced entry, and — under endorsed extensions — cash losses and transit exposures.

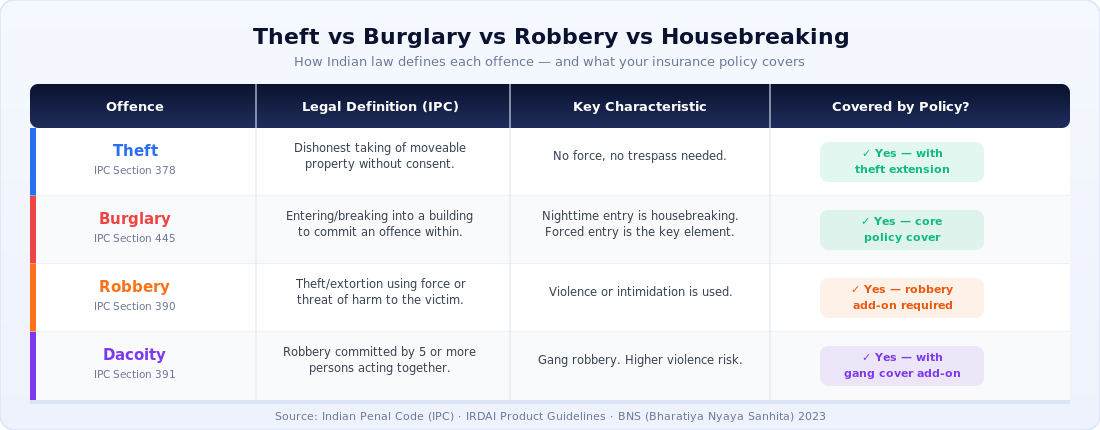

Theft vs Burglary vs Robbery vs Dacoity — What Does Indian Law Say?

These four terms are not interchangeable. Each has a precise definition under the Indian Penal Code (IPC), and insurers apply those definitions when assessing claims. Understanding the difference matters when you choose your cover.

Practically speaking: if your shop is broken into at night and stock is taken, that is burglary (IPC §445). If a courier carrying your cash receipts is waylaid and robbed at gunpoint, that is robbery (IPC §390). Both are covered by a well-structured theft and burglary policy with the right endorsements. Dacoity — robbery by five or more persons — is sometimes excluded or sub-limited in standard wordings, so check your policy schedule carefully.

What Does Theft and Burglary Insurance Cover?

The scope of cover under an Indian theft and burglary policy typically includes six main heads of loss:

Stock and inventory: Goods held for sale, raw materials and work-in-progress stolen or damaged during a break-in. Sum insured should reflect peak stock levels — especially important for retailers ahead of Diwali, Eid or wedding season.

Cash in safe: Currency and negotiable instruments locked in an approved safe on the premises. Most policies specify a minimum safe rating (e.g., Class 1 or Class 2 under IS 6756); a substandard safe may reduce or void this section.

Cash in transit: Cash, cheques and demand drafts being physically transported between your premises and the bank. Typically endorsed separately and covers the specific route and persons named in the schedule.

Fixtures, fittings and trade equipment: Shelving, display cases, machinery, refrigeration units and other non-stock property belonging to the business and used in its trade.

Damage caused by forced entry or exit: The structural cost of repairing doors, locks, windows, grilles and ceilings broken during the act of burglary — often the most expensive single-loss item in a small retail theft.

Fidelity / employee dishonesty (optional extension): Losses caused by a trusted employee misappropriating cash or stock. This extension requires separate underwriting and disclosure of internal controls.

Who Needs Theft and Burglary Insurance in India?

Almost any business that holds physical goods, cash or valuable equipment on its premises should consider this cover. Six industry segments account for the majority of claims in India:

Retailers and kirana stores: High daily cash turnover, limited overnight security and stock that is easy to move makes the corner store one of the most frequent claimants. Even a single overnight break-in can cost ₹5–15 lakh in stolen FMCG goods and smashed display units.

Jewellers and bullion traders: The single highest-value risk in Indian retail. A single jewellery heist in a Tier 2 city can result in losses of ₹50 lakh to several crore. IRDAI requires specialist underwriting for gold and precious stones above defined thresholds.

Hotels and hospitality businesses: Guest valuables, bar stock, kitchen equipment, linen stores and front-desk cash all create meaningful theft exposure. Most hotel standard fire policies do not automatically extend to guest property theft.

Warehouses and logistics hubs: Large volumes of third-party goods held under bailee liability. A single warehouse break-in can trigger multiple downstream claims from cargo owners, making this one of the most complex theft risks to manage.

Manufacturing units: Raw material stores, finished goods awaiting dispatch, and expensive tooling are all vulnerable — particularly in peri-urban industrial estates that lack 24/7 guard patrols.

Pharmacies and medical suppliers: Scheduled drugs and medical devices carry high street value, making pharmacies disproportionately targeted. Regulatory obligations also require that stolen Schedule H or Schedule X drugs be reported to State Drug Controllers.

Key Benefits of Theft and Burglary Insurance

Full stock reinstatement: Replaces stolen inventory at current market value so you can reopen quickly without depleting working capital.

Damage cover included: Pays for structural repairs that a standard fire policy typically excludes.

Cash protection: Covers safe and transit exposures that are invisible to most property policies.

Business continuity: Some policies include a business interruption extension that compensates for lost gross profit during the period needed to repair or restock.

Affordable for SMEs: Premiums start at ₹3,000–₹8,000 per annum for a small kirana store, making it one of the most cost-effective risk transfers available to Indian small businesses.

IRDAI-approved wordings: Standard policy language ensures consistent claims handling across insurers.

Common Challenges and Exclusions to Watch

Unexplained stock shortages: Pilferage or shrinkage discovered during a stocktake — without any evidence of forced entry — is almost always excluded. The policy requires a verifiable event, not a general shortfall.

Insider theft without fidelity extension: Standard policies exclude theft by employees unless the fidelity or employee dishonesty extension is specifically added.

Underinsurance: Many businesses set their sum insured at book value rather than replacement cost, and then discover a significant shortfall at the time of claim. Average clauses apply; if you're insured for 60% of value, you recover only 60% of any loss.

Security warranty breaches: Policies impose minimum security standards — approved locks, alarm systems, grilles. Failing to maintain these can void your claim. Always read the security warranties in your policy schedule.

Currency or precious metal sub-limits: Cash and jewellery often carry sub-limits well below the total sum insured. Confirm these match your actual holdings.

Regulatory Framework — IRDAI and Standard Wordings

Theft and burglary insurance in India operates under the IRDAI's File and Use product framework. Insurers are permitted to offer either the standardised Burglary Insurance Policy (as notified) or an approved package policy that bundles fire and burglary perils. The IRDAI's General Insurance Council coordinates market-level data on theft and crime statistics that inform premium rate filings.

Key regulatory milestones shaping the current product landscape:

2019 — IRDAI Sandbox RegulationsEnabled insurtechs to pilot usage-based and IoT-triggered theft policies — connecting alarm activations directly to claim notifications.

2022 — Bima Sugam InitiativeIRDAI's digital insurance marketplace push accelerated online issuance of SME theft policies, reducing policy acquisition time from days to minutes.

2023 — IRDAI Consolidated RegulationsConsolidated product regulations clarified sum insured methodology for stock-in-trade, requiring insurers to offer agreed-value options for high-value inventory classes.

2024 — Bima VistaarThe flagship rural insurance scheme is expected to bundle basic theft cover for agricultural produce stores and rural SMEs — extending protection to India's underserved hinterland businesses.

Protect your stock, cash and premises

IRDAI-approved theft and burglary cover tailored for Indian retailers, jewellers, warehouses and SMEs. Get an instant quote from TropoGo's specialist team.

Why Insurance is the Foundation, Not an Afterthought

Most Indian SME owners believe they are too small to be targeted, or assume that CCTV and a padlock are sufficient deterrents. Neither assumption holds. Professionally equipped thieves bypass both in minutes. Insurance does not prevent theft, but it guarantees that a single criminal event does not become a permanent business closure.

TropoGo's specialist theft and burglary programme for Indian businesses includes six distinct cover modules, structured to match your actual risk profile:

Stock-in-trade cover (replacement value): Pays the current retail replacement cost of stolen goods — not the historic purchase price. Essential for retailers whose margins depend on restocking at today's prices.

Cash-in-safe extension: Covers currency and negotiable instruments held in an approved GODREJ, OZONE or equivalent Class 2 safe, up to the declared limit in the schedule.

Cash-in-transit cover: Protects cash being physically carried to or from your bank, typically for declared routes and the named persons responsible for the transit.

Fixtures and fittings reinstatement: Pays for display counters, refrigeration units, CCTV hardware and other trade fixtures that are damaged or stolen during a forced entry — at new-for-old replacement value.

Damage by forcible entry: Meets the full cost of repairing structural damage — broken doors, shattered glass, forced grilles — inflicted during the act of burglary, regardless of whether any stock was actually taken.

Fidelity and employee dishonesty extension: Covers loss of money or property caused by fraud, embezzlement or dishonesty by your own staff — subject to disclosure of your internal cash-handling and approval controls.

Outlook — What's Next for Theft Insurance in India

India's rapid urbanisation and the expansion of organised retail into Tier 2 and Tier 3 cities is creating new theft exposures. As distribution networks lengthen and more valuable goods move through peri-urban warehouses, cargo-in-transit and premises-based theft risks are growing in tandem.

Technology is reshaping the product: IoT-enabled alarm systems that feed directly into insurers' claims platforms, real-time CCTV monitoring linked to policy activation, and AI-driven inventory reconciliation tools that can identify a theft event within minutes. By 2027, industry analysts expect IoT-triggered theft policies — where the alarm itself initiates a provisional claim — to account for more than 15 percent of new SME theft policy sales in urban India.

For now, the simplest step remains the most important: make sure your sum insured reflects your actual peak-stock holding, not last year's book value. A ₹40 lakh stock holding insured for ₹15 lakh is not insurance — it's a co-insurance arrangement where you carry the larger share of the risk yourself.

Frequently Asked Questions

Does a standard fire policy cover theft and burglary in India?

No. The Standard Fire and Special Perils Policy (SFSP) covers fire, explosion, flood, earthquake and allied perils — but theft and burglary are explicitly excluded. You need a separate standalone Burglary Insurance Policy, or a package policy that specifically bundles both fire and burglary sections. Always check the policy schedule to confirm burglary cover is included before assuming it is.

What is the difference between a burglary policy and a theft policy?

In Indian insurance practice, "burglary" technically requires evidence of forcible and violent entry or exit — meaning a lock was broken, a window was smashed or a seal was cut. "Theft" is broader and includes any dishonest taking, even without force. Many policies are branded as "Theft and Burglary" to cover both scenarios. Always read the operative clause to confirm which perils are included under your specific policy wording.

How is the sum insured calculated for stock?

Stock sum insured should reflect the maximum value of goods held on your premises at any one time — not the average. For seasonal businesses (jewellers before Dhanteras, electronics retailers before Diwali), this means insuring for the peak-stock figure even if that level is only reached for a few weeks each year. Underinsuring against your peak exposure will trigger the average clause at claim time, reducing your recovery proportionally.

Are employee theft and pilferage covered?

Standard theft and burglary policies exclude loss caused by your own employees. To cover employee dishonesty, you must add a Fidelity Guarantee extension or take out a separate Employee Dishonesty policy. This extension requires you to disclose your internal cash-handling procedures, approval hierarchies and any prior incidents. Premiums are typically 15–25 percent higher with this extension added.

What security measures does my insurer require?

Most IRDAI-approved theft policies impose minimum security warranties: approved deadlock cylinders on all access points, grilles or laminated glass on ground-floor windows, a monitored alarm system for sums insured above ₹25 lakh, and an approved safe for cash holdings. Failing to maintain these warranties — even if your insurer never inspected the premises — can result in a claim being repudiated. Always keep documentation of your security maintenance.

How do I get specialist theft and burglary cover for my business in India?

TropoGo offers IRDAI-approved theft and burglary insurance tailored for Indian retailers, jewellers, warehouses and SMEs. Cover can be structured to include stock at replacement value, cash-in-safe, cash-in-transit, fixtures reinstatement and employee dishonesty — all on a single policy schedule. Get an instant quote or speak to a specialist at TropoGo Theft and Burglary Insurance.

Theft and burglary insurance is not a luxury for large retailers — it is table-stakes protection for any Indian business that holds stock, cash or valuable equipment. One break-in, one overnight loss, one smashed showcase is all it takes to wipe out months of margin. TropoGo's specialist cover ensures that when the worst happens, your business keeps going.