What is Crop Insurance and How It Protects Farmers in India

21 May 2026 | 8 min read

Protect your harvest before the season ends — PMFBY, WBCIS and private crop insurance for India's farmers and agri-businesses

Drought, flood, pest, hailstorm — government-subsidised cover at 1.5–5% premium, with direct claim credit to your bank account. One bad season should not end a lifetime of farming.

In September 2023, farmers in Nashik district woke to fields stripped bare by unseasonal heavy rains — grapes on the vine, ready to harvest, destroyed overnight. Those enrolled in the Pradhan Mantri Fasal Bima Yojana (PMFBY) received claim amounts directly in their bank accounts within weeks. Those who were not enrolled had nothing. The difference between those two groups — insured and uninsured — is the difference between a setback and a catastrophe. It is also the difference that crop insurance is designed to make.

Indian agriculture feeds 1.4 billion people and employs nearly half the workforce. Yet it operates under a constant threat from weather, pests and market forces that no individual farmer can fully control. India's annual agricultural losses to weather-related events average ₹50,000–₹80,000 crore — a number that dwarfs the entire group health insurance market. Crop insurance is not an add-on for progressive farmers. It is the financial foundation without which sustainable farming — and sustainable rural credit — cannot function.

This guide explains the four types of crop insurance available in India, what they cover, how claims work, who regulates them, and how to choose the right cover for your farm, FPO or agri-business.

What is Crop Insurance?

Crop insurance is a financial protection mechanism that compensates farmers for losses in crop yield, crop revenue or specific named perils (drought, flood, pest, hail, fire) that occur during a growing season. Unlike life or health insurance — which cover events that happen to a person — crop insurance covers the biological and meteorological risk of agricultural production itself.

In India, crop insurance operates through two primary structures. The first is yield-based insurance (PMFBY), where the trigger is a shortfall in the average yield of a defined area (a block, taluka or district) compared to a historical threshold yield. The second is weather-index or parametric insurance (WBCIS), where the trigger is an objective weather parameter — rainfall below X mm, temperature above Y°C — measured at an IMD reference weather station, without requiring any field assessment of crop damage.

Both structures are governed by the Ministry of Agriculture and Farmers' Welfare, regulated by IRDAI, and implemented through empanelled general insurance companies. The government subsidises the premium — sometimes by as much as 98% — leaving the farmer to pay only 1.5–5% of the sum insured, depending on the crop type.

Types of Crop Insurance in India

India's crop insurance ecosystem currently offers four distinct product types, each targeting a different risk or farming segment:

The Pradhan Mantri Fasal Bima Yojana (PMFBY) is the flagship scheme, covering all food crops, oilseeds and commercial crops on a comprehensive yield-guarantee basis. It reached 5.5 crore farmer applications in Kharif 2023, making it one of the world's largest agricultural insurance programmes by headcount.

The Weather Based Crop Insurance Scheme (WBCIS) uses automated weather station data to trigger payouts — no field survey required, no crop-cutting experiments, no delay waiting for revenue officials to complete assessments. This makes it particularly valuable for horticulture and high-value crops where a 30-day claim settlement delay can mean a business closure.

For non-loanee farmers (those without Kisan Credit Cards), voluntary enrolment under PMFBY has been available since 2020, when the government made the scheme optional for loanee farmers and created specific outreach programmes to bring non-borrower cultivators into the system.

What Does Crop Insurance Cover?

A comprehensive PMFBY or WBCIS policy protects against six major categories of agricultural risk:

Pre-sowing and prevented sowing losses: If adverse weather prevents you from sowing at the start of the season, PMFBY pays 25% of the sum insured as a prevented-sowing benefit — acknowledging that the loss begins before the crop is even in the ground.

Standing crop losses (mid-season): The main yield-guarantee component. If the average yield in your notified area falls below the threshold yield (typically the 7-year average), all enrolled farmers in that area receive a proportional indemnity payment.

Post-harvest losses (14-day window): Losses that occur after cutting and bundling — while the harvested crop lies in the field waiting to be threshed — due to cyclone, hailstorm or unseasonal rain. Coverage continues for 14 days post-harvest.

Localised calamities: Hailstorm, landslide and inundation assessed on an individual farm basis (not area-average). One of the most practically important extensions, because localised events that don't trigger area-level average yield shortfalls often cause 100% damage on individual farms.

Wild animal attacks: In notified areas, PMFBY may cover crop damage from wild animals (elephants, nilgai, wild boar) under an add-on module, addressing one of the most underinsured risks in forest-fringe farming communities.

Prevented sowing / planting risk: For plantation crops covered under R-WBCIS, adverse weather at the sowing/planting stage triggers a partial payout without requiring a full-season yield assessment.

₹2.36 lakh croreTotal claims paid under PMFBY since launch in 2016 — the largest agricultural insurance claim payout programme in Indian history (as of FY2024)

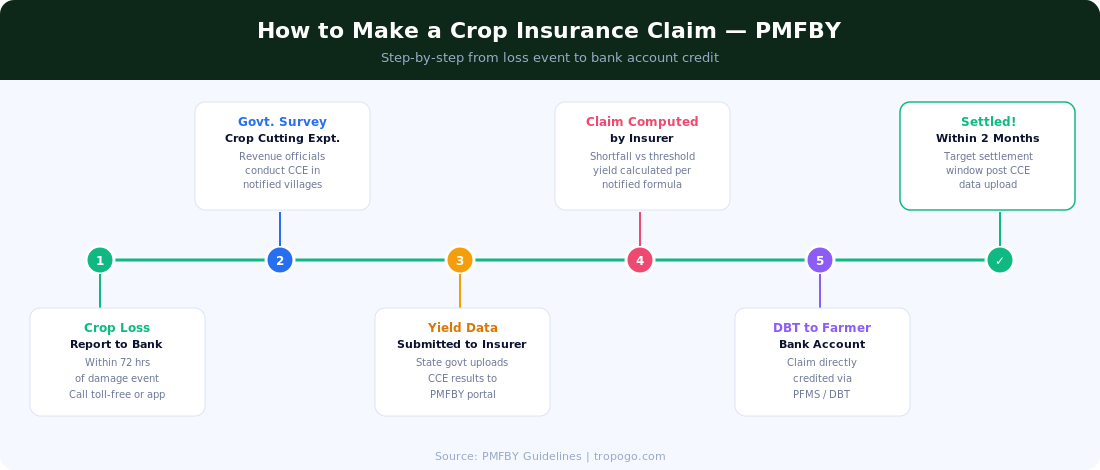

How the Claims Process Works

One of the most common reasons Indian farmers avoid crop insurance is a belief — often based on real past experiences with older schemes — that claiming is complicated and payment is slow. PMFBY has restructured the claims process significantly since 2020:

The key reforms that have improved claim experience include: mandatory linkage of farmer accounts to Aadhaar and Jan Dhan bank accounts for direct benefit transfer; the WINDS (Weather Information Network Data Systems) project that is automating weather data collection; and a 12% penal interest charge on insurers who delay claim settlement beyond the specified window — giving companies a financial incentive to process claims promptly.

For WBCIS-style weather index claims, the process is even simpler: no farm visit, no crop-cutting, no loss assessment. The weather station triggers a payout automatically when the parameter breaches the threshold. This is the direction the industry is moving — and it is particularly well-suited to India's large number of small and marginal farmers who lack the documentation and negotiating capacity to manage complex indemnity claims.

Key Benefits of Crop Insurance for Indian Farmers

Affordable premium: Farmers pay only 1.5% for Rabi food crops, 2% for Kharif food crops and oilseeds, and 5% for annual commercial/horticultural crops. The state and central government share the remaining premium subsidy — often absorbing 80–95% of the actuarial rate.

Access to credit: Loanee farmers enrolled in PMFBY often find that their bank requires them to take crop insurance as a condition of the Kisan Credit Card loan. This actually protects both the farmer and the lender — insured farmers are less likely to default after a crop failure.

Direct bank credit: Claims are paid via DBT (Direct Benefit Transfer) directly to the farmer's linked bank account — no intermediaries, no commission leakage, no delays at the panchayat or mandi level.

Livestock and equipment extensions: Private crop insurance programmes offered by TropoGo and empanelled insurers extend cover beyond the standing crop to livestock, agri equipment, storage structures and post-harvest storage losses — building a comprehensive agri-financial safety net.

FPO and corporate agri cover: Farmer Producer Organisations and agri-corporates sourcing from contract farmers can take a group crop insurance policy that covers the aggregate production of their entire supplier base — aligning insurance with the supply chain structure of modern Indian agriculture.

Challenges in India's Crop Insurance Ecosystem

Area-average trigger vs. individual loss: The biggest structural weakness of PMFBY's yield-guarantee model. A farmer who loses 100% of their crop because a hailstorm hit their field specifically — but neighbouring fields were unaffected — may receive zero claim if the area-average yield remains above threshold. The localised calamity extension addresses this partially, but awareness and enrolment in that add-on remain low.

Crop-cutting experiment delays: CCEs require physical field visits by revenue officials, and delays in completing and uploading CCE data are the single biggest cause of claim settlement delays. The WINDS automation project and satellite-based remote sensing are being rolled out to reduce dependence on manual CCEs.

Low voluntary enrolment: Since PMFBY became voluntary for loanee farmers in 2020, enrolment among non-borrower cultivators has been slow. Small and marginal farmers — who need the protection most — are the hardest to reach through bank-led distribution.

Sum insured adequacy: The sum insured under PMFBY is calculated as the cost of cultivation notified by the state government — which is often lower than the actual market cost of inputs. Farmers who invest heavily in quality seed, fertiliser and irrigation find that even a 100% claim payout does not cover their actual losses.

Regulatory Framework — Ministry of Agriculture & IRDAI

Crop insurance in India operates under a dual oversight structure. The Ministry of Agriculture and Farmers' Welfare sets scheme design, premium subsidy rates, notified crops and areas, and sum insured methodology. IRDAI licenses and supervises the implementing insurance companies, approves product wordings and monitors solvency standards.

Key regulatory milestones since PMFBY's 2016 launch include the 2020 PMFBY restructuring (making loanee enrolment voluntary, increasing state flexibility in scheme adoption), the 2022 expansion of the localised calamity add-on, and the 2023 WINDS project mandate requiring all states to operationalise automated weather station networks by 2025–26. In parallel, IRDAI's Bima Vistaar initiative is creating a simplified, bundled rural insurance product that includes crop, life and property cover in a single low-premium package targeted at India's underinsured rural households.

Protect your harvest before the season begins

PMFBY-enrolled and private crop insurance for Indian farmers, FPOs and agri-businesses. Yield-based, weather-index and livestock cover — structured to your crop, season and state.

TropoGo's agricultural insurance programme for Indian farmers, FPOs and agri-corporates covers six distinct risk layers, structured to complement the government PMFBY base cover with the gaps that scheme leaves unaddressed:

PMFBY enrolment and facilitation: For loanee and non-loanee farmers, TropoGo's partner network facilitates PMFBY enrolment through the national crop insurance portal — ensuring correct crop, area and sum insured registration before the cutoff date for each Kharif and Rabi season.

Top-up yield cover: A private parametric or indemnity top-up layer that covers the gap between the PMFBY notified sum insured (cost of cultivation) and the farmer's actual investment or market-linked crop value — particularly relevant for export-quality produce and contract farming arrangements.

Weather-index cover (standalone): For farmers in states that have not notified WBCIS, or for crops not covered under government schemes, standalone weather-index policies covering rainfall, temperature, frost and humidity — issued directly by IRDAI-empanelled private insurers.

Livestock insurance: Covers cattle, buffaloes, sheep, goats and poultry against death from accident, disease or natural disaster — protecting the complementary income stream that most farm households depend on alongside crop revenue.

Agricultural equipment insurance: Tractors, harvesters, drip irrigation systems, solar pumps and cold storage equipment — covered against mechanical breakdown, accidental damage and theft. Critical for the 8.4 million custom hiring centres and FPO equipment pools that support India's smallholder farmers.

Post-harvest and warehouse storage insurance: Covers stored grain, pulses, oilseeds and horticulture produce against fire, flood, pest infestation and structural collapse while held in a warehousing facility — bridging the gap between harvest and market sale.

Outlook — Technology and the Future of Indian Crop Insurance

Three converging trends will reshape crop insurance in India over the next five years. First, satellite-based remote sensing: ISRO's crop mapping technology, integrated with the Agristack digital farmer registry, is enabling insurers to assess crop health at the individual plot level using NDVI (Normalised Difference Vegetation Index) readings — moving crop insurance from area-average indemnity to plot-level precision indemnity.

Second, agri-fintech integration: Digital platforms like DeHaat, Ninjacart, Gramophone and AgriBazaar are embedding insurance at the point of input purchase or produce sale — making enrolment a one-tap step rather than a separate bank visit. This is expected to bring 1–2 crore new non-loanee farmers into crop insurance coverage by 2027.

Third, parametric innovation: Private insurers, backed by reinsurers like Swiss Re and Munich Re, are developing increasingly granular parametric products — covering specific growth-stage weather events (unseasonal rains at flowering, cold spells at fruit set) that the area-average PMFBY framework cannot address. These products are initially targeting export-grade horticulture clusters in Maharashtra, Andhra Pradesh, Karnataka and Punjab, where the per-acre investment justifies a higher private premium.

Frequently Asked Questions

Is crop insurance compulsory for farmers in India?

No — since 2020, crop insurance under PMFBY became voluntary even for loanee farmers (those with Kisan Credit Cards), reversing the earlier mandatory enrolment policy. Non-loanee farmers have always had the option to enrol voluntarily. However, some state governments and banks may still require insurance as a loan condition. Voluntary enrolment is strongly recommended given the scale of weather-related agricultural losses in India.

What is the difference between PMFBY and WBCIS?

PMFBY (Pradhan Mantri Fasal Bima Yojana) is a yield-guarantee scheme where the trigger is a shortfall in the average yield of a notified area, measured through crop-cutting experiments conducted by revenue officials. WBCIS (Weather Based Crop Insurance Scheme) is a parametric scheme where the trigger is an objective weather parameter — rainfall, temperature, humidity — measured at an IMD reference station, with automatic payout when the threshold is breached. WBCIS typically pays faster because it does not require field assessments.

How is the crop insurance claim amount calculated?

Under PMFBY, the claim per farmer = (Threshold Yield − Actual Yield) ÷ Threshold Yield × Sum Insured. For example, if the threshold yield is 2,000 kg/hectare, actual yield is 1,200 kg/hectare, and sum insured is ₹40,000/hectare, the claim = (800 ÷ 2,000) × ₹40,000 = ₹16,000/hectare. Under WBCIS, the payout is determined by the deviation of the weather parameter from the strike level, multiplied by a pre-defined payout rate per unit of deviation.

When must I notify the insurer of a crop loss?

Under PMFBY, you must notify the insurer, bank or district agriculture office within 72 hours of a localised calamity event (hailstorm, inundation, landslide) for the individual farm loss assessment to be activated. For area-average yield claims, individual notification is not required — the state government's crop-cutting experiment data automatically triggers the claim for all enrolled farmers in the affected notified area.

Can FPOs and agri-companies take group crop insurance?

Yes. Farmer Producer Organisations, contract farming companies and agri-processors sourcing from multiple farmers can take group crop insurance policies that aggregate the yield exposure of their entire supplier base. This allows professional agri-businesses to manage their procurement risk at the portfolio level — protecting both their own margin and the financial stability of their farmer suppliers. TropoGo structures customised group crop insurance for FPOs of all sizes.

How do I enrol in crop insurance if I do not have a Kisan Credit Card?

Non-loanee farmers can enrol directly through the national crop insurance portal (pmfby.gov.in), through a designated bank, or through a Common Service Centre (CSC) in their village. You will need your Aadhaar number, bank account details, land records (7/12 extract or equivalent) and crop sowing details. TropoGo's agri insurance specialists can guide you through the enrolment process — get in touch at TropoGo Crop Insurance.

India's farmers carry the nation's food security on their shoulders — and increasingly, they do it under the threat of weather patterns that are growing more volatile every decade. Crop insurance is not a guarantee against loss. It is a guarantee that a loss does not become the end of the farm. Whether you are a smallholder cultivating two acres of paddy in Odisha, a horticultural entrepreneur managing grape vineyards in Nashik, or an FPO aggregating 500 farmer members in Madhya Pradesh, TropoGo's crop insurance specialists are here to help you find the right cover before the next season begins.