What is Home Insurance and Why Every Homeowner Needs It

21 May 2026 | 7 min read

Protect your home, contents and liability — specialist home insurance for India's homeowners, tenants and housing societies

Fire, earthquake, flood or theft — IRDAI-approved structure, contents and liability cover for your most valuable asset. One claim should not cost you a lifetime of savings.

Rakesh Sharma had lived in his three-bedroom flat in Navi Mumbai for eleven years. He had paid off most of the home loan, furnished it carefully, and watched its value climb with the city. Then one July morning, the overhead water tank on the terrace burst. Within an hour, the ceiling had collapsed in two rooms, soaking the flooring, furniture, and his daughter's laptop. The repair bill came to ₹6.8 lakh. His bank account had ₹2.1 lakh in it. He had no home insurance.

Rakesh's story is not unusual. India's urban housing stock is worth an estimated ₹200 lakh crore — yet fewer than one in three homeowners carries any property insurance cover. Most people insure their car and their health. Almost nobody insures the building they live in or the contents inside it. That changes the moment something goes wrong — and in India, with its seismic zones, monsoon seasons, cyclone coastlines, and urban theft rates, something eventually always goes wrong.

What is Home Insurance?

Home insurance is a financial product that protects the physical structure of your home, its contents, and your legal liability to third parties — all under a single IRDAI-regulated policy. It pays you back when your home is damaged by fire, flood, earthquake, theft, cyclone, or accident, so you can rebuild or replace without draining savings built over a lifetime.

In India, home insurance is offered by general insurance companies licensed by the IRDAI. It is not mandatory (unlike vehicle insurance), but most lenders require borrowers to hold it as a condition of the home loan — though the cover is often limited to the structure only, and only for the loan tenure. A comprehensive home insurance policy goes far further: it covers tenants, housing-society members, and freehold owners alike, and it can be tailored with add-ons covering everything from jewellery to solar panels.

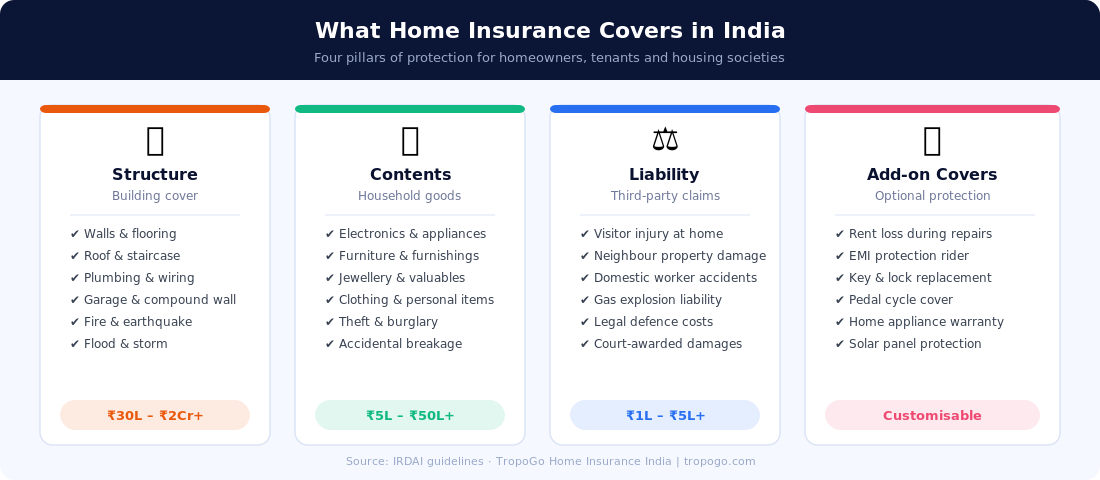

The Four Pillars of Home Insurance Cover

A well-structured home insurance policy rests on four pillars:

Structure cover — pays for the cost of rebuilding or repairing the physical building: walls, roof, flooring, plumbing, electrical wiring, staircases, compound walls and fixed fittings. The sum insured should reflect the rebuild cost (not the market value), which for a typical 1,200 sq ft Mumbai flat can range from ₹35 lakh to ₹80 lakh depending on construction quality.

Contents cover — reimburses you for household goods destroyed or stolen: electronics, appliances, furniture, clothing and declared valuables such as jewellery. Most policies cover on an indemnity (depreciated) basis; a few offer reinstatement (new-for-old) cover at a higher premium.

Liability cover — protects you if a visitor is injured on your premises, a domestic worker suffers an accident, or a plumbing failure damages a neighbour's property. Legal defence costs are also covered. Sums typically range from ₹1 lakh to ₹5 lakh.

Optional add-ons — extend the policy to cover rent loss while repairs are underway, key-and-lock replacement, pedal cycles, home appliances, EMI protection, or solar panels. These are underwritten individually and priced at a small additional premium.

India's Home Insurance Landscape — Risk, Coverage and Key Insurers

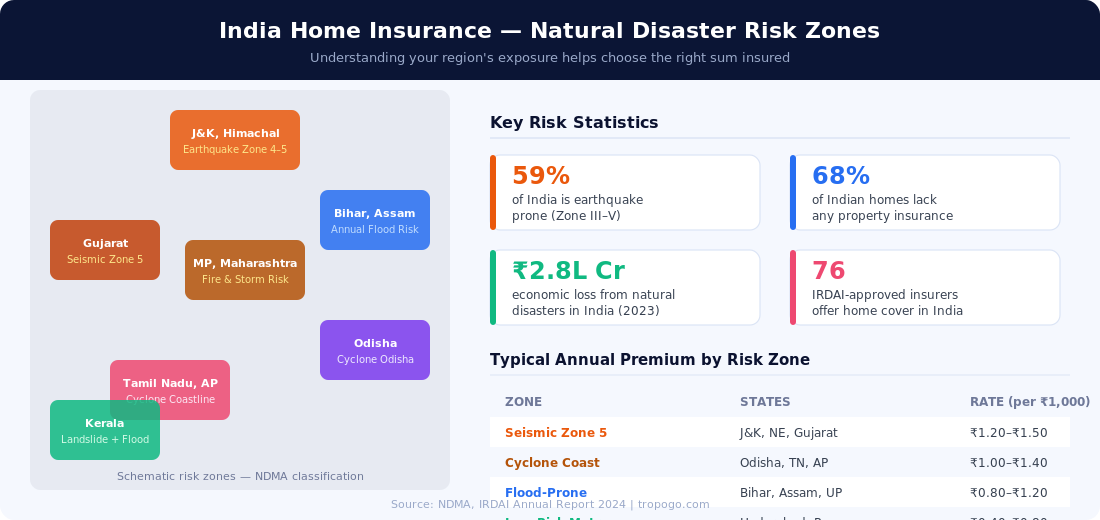

India's property risk landscape is highly regional. The Himalayan belt, Gujarat, and the northeastern states sit in earthquake Seismic Zone 4 or 5. The Odisha, Andhra Pradesh, and Tamil Nadu coastlines face frequent cyclones. Bihar, Assam and eastern Uttar Pradesh see annual flooding. Kerala combines landslide risk with extreme rainfall. A home insurance policy priced for Hyderabad's relatively benign risk environment is not the same as one for a ground-floor flat in Surat's flood-prone Old City.

Major IRDAI-licensed insurers offering home cover in India include New India Assurance, United India Insurance, Bajaj Allianz, HDFC Ergo, ICICI Lombard, Tata AIG, SBI General, and Reliance General. Speciality platforms like TropoGo bundle expert advice with access to insurers covering high-value properties, heritage structures, and housing-society blanket policies. Premiums typically range from ₹2,000–₹5,000 per year for a standard urban flat with ₹50 lakh structure cover — a fraction of one EMI on a home loan.

Benefits of Home Insurance

Financial resilience after a disaster. The average earthquake loss for a Zone-5 household runs to several lakh rupees. Without insurance, recovery means liquidating savings or taking on debt. With insurance, the payout arrives within 15–30 days of a valid claim.

Contents replacement at scale. A single room fire can destroy ₹8–12 lakh of electronics, furniture and clothing. Contents cover replaces or repairs every item without you having to fund the loss from savings.

Liability shield. A domestic worker fracturing a wrist on a slippery floor can result in a ₹1–2 lakh medical and compensation claim. Liability cover absorbs that without dispute.

Loan-linked protection. If a structure is severely damaged and the home loan remains outstanding, insurance ensures you can repair or rebuild without defaulting — protecting your credit score along with your home.

Peace of mind on travel. Many policies cover theft of contents even during extended absences, giving urban professionals and NRIs confidence that their home is protected while they are away.

Tax benefit. Premiums paid on home insurance can form part of a landlord's rental income deduction under Section 24(a) of the Income Tax Act — an often-overlooked benefit for property investors.

Challenges and What to Watch For

Under-insurance is pervasive. Many homeowners set the sum insured at the loan outstanding rather than the rebuild cost. When a claim is lodged, the insurer applies average (proportional reduction), leaving the owner to fund the shortfall.

Exclusions matter. Standard policies exclude wilful destruction, wear and tear, war, nuclear perils, and some policies exclude flood unless specifically added. Read the policy wording, not just the marketing sheet.

Contents valuation is tricky. Claiming for jewellery requires a valuation certificate. Electronics claims require purchase receipts or a valuer's report. Keep digital copies of all purchase documents in cloud storage.

Tenant vs. owner cover. A tenant can insure contents and liability but not the structure (owned by the landlord). Ensure both parties hold appropriate policies — a landlord's structure policy will not cover a tenant's stolen laptop.

Regulatory Framework — IRDAI and RBI Guidelines

The Insurance Regulatory and Development Authority of India (IRDAI) governs all home insurance products under the Insurance Act, 1938 and subsequent IRDAI (General Insurance — Products) Regulations. Key regulatory provisions include:

Policyholder protection: IRDAI mandates that all general insurers maintain a claims settlement ratio above 80%. Grievance redressal is handled by the Insurance Ombudsman, with 17 offices across India for policyholder complaints.

Standardised Bharat Griha Raksha policy: In 2021, IRDAI introduced the Bharat Griha Raksha (BGR) — a standardised home insurance product that all general insurers must offer. BGR covers the structure (and optionally contents) at defined minimum sums, making comparison shopping straightforward for first-time buyers.

RBI home loan linkage: The Reserve Bank of India's master circular on housing finance requires lenders to facilitate (though not compel) home insurance at disbursement. Banks and HFCs typically bundle single-premium policies into the loan, which borrowers should review carefully to ensure the sum insured is adequate.

State government schemes: Several states run property protection schemes for BPL households — Odisha's Biju Pucca Ghar and West Bengal's Gariber Ghar provide modest catastrophic cover alongside construction grants — alongside mainstream IRDAI-regulated policies for all other homeowners.

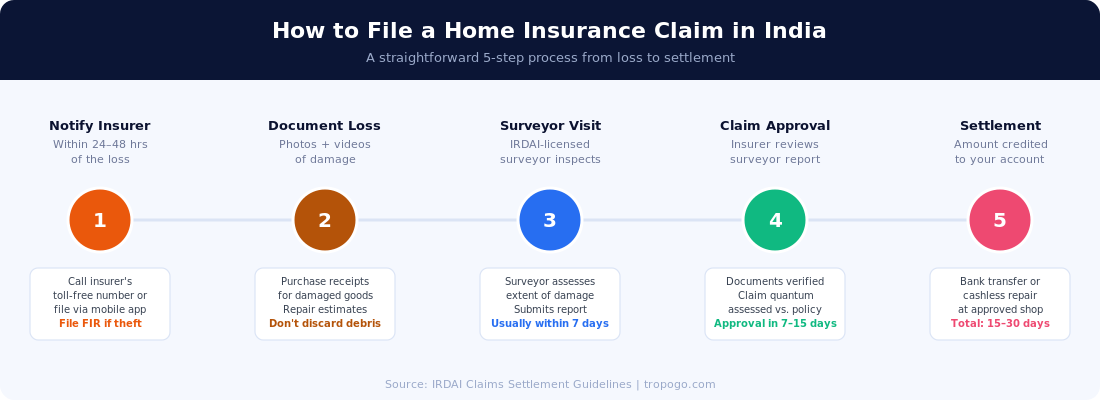

How to File a Home Insurance Claim

Filing a home insurance claim in India follows a defined process. The moment you discover damage, notify your insurer within 24–48 hours — this is a policy condition, not a formality. If the cause is theft or burglary, file an FIR with the local police station before contacting the insurer. As you wait for the surveyor, photograph and video everything: the damage, the point of entry, and any damaged items. Do not dispose of debris or commence repairs until the IRDAI-licensed surveyor has inspected the site and submitted their report. The entire process — notification to settlement — typically takes 15–30 days for straightforward claims. Disputes can be escalated to the Insurance Ombudsman for free adjudication.

Why Home Insurance is the Foundation, Not an Afterthought

For most Indian families, the home is 60–80% of their total net worth. Yet it is the last asset to be insured. The logic of "it won't happen to me" has been disproved for thousands of families by the 2001 Gujarat earthquake (20,000 deaths, ₹21,000 crore losses), the 2015 Chennai floods (₹15,000 crore), and annual cyclone seasons along both coastlines.

Is your home and its contents fully protected?

TropoGo's specialist advisors help you choose the right structure sum insured, select contents cover for your actual household assets, and add relevant riders — from rent loss to jewellery all-risk.

A comprehensive home insurance policy from TropoGo provides the following layers of protection — structured to Indian risk conditions and IRDAI-approved cover at premiums designed for Indian homeowners:

Structure cover up to ₹2 crore+ — rebuild cost basis, covering fire, earthquake, flood, cyclone, storm, subsidence, landslide, explosion and aircraft impact

Contents all-risk cover — electronics, appliances, furniture, clothing and declared jewellery, including accidental breakage and theft

Third-party liability — protection against claims for bodily injury or property damage caused from your home, including domestic worker accidents

Rent loss cover — alternative accommodation costs while the home is uninhabitable during insured repairs

EMI protection rider — loan repayment cover if the home is rendered temporarily uninhabitable

Heritage property specialist underwriting — for pre-1947 bungalows, farmhouses and heritage structures where standard policies undervalue unique construction materials

The Outlook — India's Home Insurance Opportunity

India's home insurance penetration is under 1% of GDP — compared to 3–4% in developed markets. The combination of rapid urbanisation, rising middle-class home ownership (particularly in Tier 2 cities), IRDAI's Bharat Griha Raksha standardisation, and InsurTech platforms offering instant digital quotes is beginning to close this gap. Between 2020 and 2024, home insurance premium income in India grew at 14% CAGR — the fastest-growing segment in general insurance. For homeowners who act now, the window to lock in lower premiums before risk-based pricing adjustments is open.

Frequently Asked Questions — Home Insurance India

Is home insurance mandatory in India?

Home insurance is not legally mandatory for individual homeowners or tenants. However, most banks and housing finance companies require borrowers to hold at least a structure insurance policy as a condition of the home loan. For housing societies, many state co-operative housing acts require blanket structure cover. Even where not mandated, home insurance is strongly advisable given the high natural disaster risk across most Indian states — from seismic zones in the Himalayas to cyclone coastlines in the south.

What is the difference between structure and contents insurance?

Structure insurance covers the physical building — walls, roof, flooring, plumbing, wiring and fixed fittings — against perils like fire, earthquake, flood and cyclone. The sum insured should reflect the rebuild cost, not the market value of the property. Contents insurance covers movable items inside the home: electronics, furniture, appliances, clothing and declared valuables like jewellery. A tenant who does not own the building can buy contents insurance independently. A homeowner should ideally hold both. The IRDAI's standardised Bharat Griha Raksha policy offers structure and contents in a bundled product.

How is the sum insured calculated for home insurance?

The structure sum insured is calculated on the basis of the reinstatement (rebuild) cost — the cost per square foot to demolish and rebuild to the same specification, multiplied by the built-up area. In 2025, this ranges from ₹1,800–₹3,500 per sq ft in Tier 1 cities depending on construction quality. Avoid the common mistake of using market value or the outstanding loan as the sum insured. Market value includes land (which cannot be destroyed), and the loan balance may be far less than the rebuild cost. TropoGo advisors can provide a free rebuild-cost estimate before you buy.

Does home insurance cover earthquake damage?

Yes — earthquake cover is included as a standard peril in most home insurance policies in India, including the IRDAI-standardised Bharat Griha Raksha. Given that 59% of India's land area falls in Seismic Zone III–V, earthquake cover is one of the most critical features to verify when comparing policies. Note that premiums are higher in Seismic Zone 4–5 areas (J&K, Gujarat, northeastern states, parts of Uttarakhand and Himachal Pradesh) than in lower-risk zones. Some older, budget policies list earthquake as an optional add-on — always confirm before buying.

Can a tenant buy home insurance?

Yes — tenants can and should buy a contents and liability home insurance policy even though they do not own the building. A tenant's policy covers all movable belongings inside the rented property (electronics, furniture, clothing, valuables) against theft, fire and accidental damage, and provides liability protection if a visitor is injured or a neighbouring property is damaged. The landlord is responsible for insuring the structure. Both policies are distinct, separately underwritten, and should be held simultaneously for complete protection.

How do I get the right home insurance cover from TropoGo?

TropoGo's specialist advisors help Indian homeowners, tenants and housing societies choose the right structure sum insured (using current rebuild-cost data), select contents cover appropriate to their actual household assets, and add relevant riders like rent loss or jewellery all-risk. The process is fully digital — get a quote, compare policies from IRDAI-approved insurers, and receive your policy document within minutes. Visit tropogo.com/other-insurance/home-insurance to protect your home today.

Your home is your family's most valuable asset. Do not leave it unprotected. Get a home insurance quote from TropoGo's specialist team and choose IRDAI-approved cover that matches your actual risk — structure, contents, liability and more.