Why Every Indian Needs Personal Accident Insurance

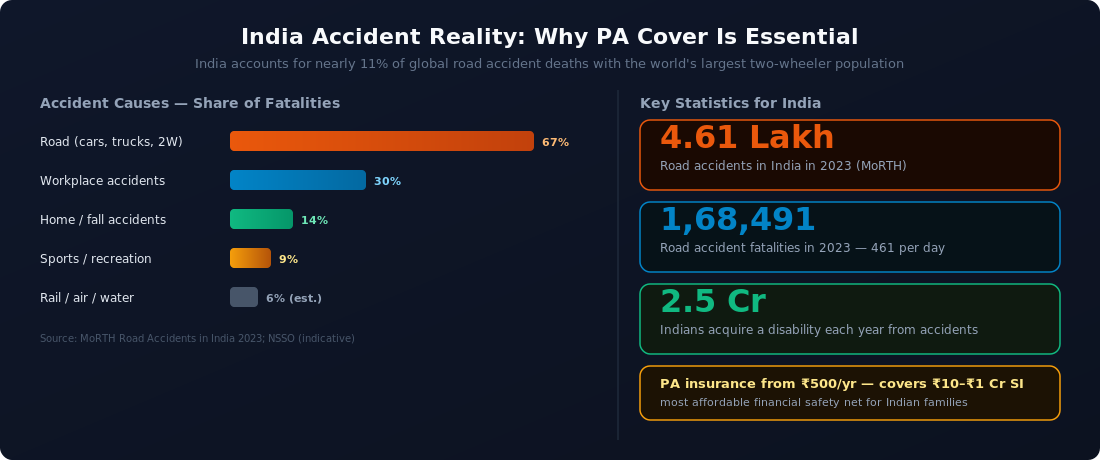

Every 90 seconds, a road accident occurs somewhere in India. In 2023, the Ministry of Road Transport and Highways recorded 4.61 lakh road accidents, claiming 1,68,491 lives — that is 461 deaths every single day. Add workplace accidents, falls at home, sports injuries and industrial incidents, and the number of Indians who suffer disabling injuries each year runs into crores.

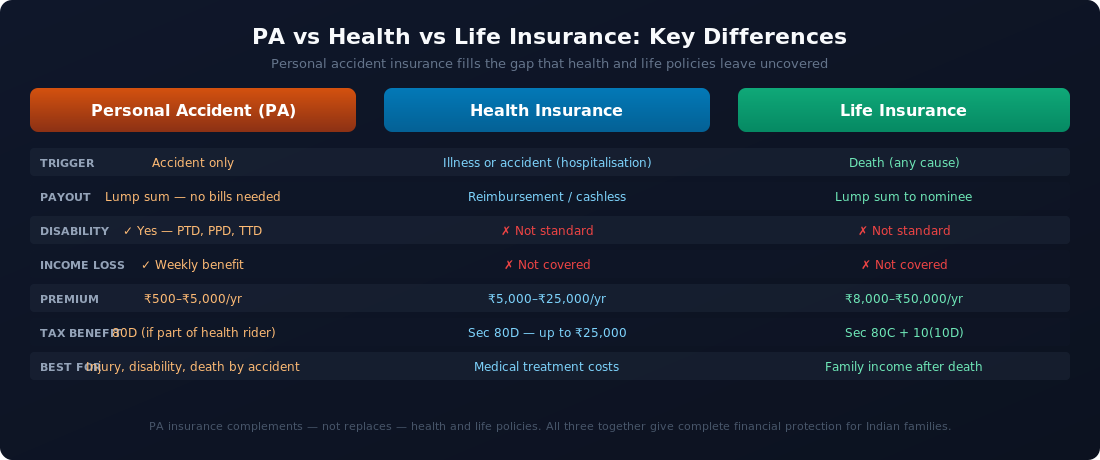

Most of these families had no financial safety net. When the primary earner is killed or disabled in an accident, the household faces a dual crisis: the loss of income and the surge in medical expenses — simultaneously. Health insurance may cover the hospitalisation bill. Life insurance may eventually pay a death claim. But neither covers the months or years of lost income while the injured person cannot work, or the lump-sum replacement for a limb or a lost career.

Personal accident (PA) insurance is designed to fill exactly this gap. It is a standalone indemnity product — governed by IRDAI — that pays fixed benefits directly to the insured or their nominee when an accident causes death, disability or hospitalisation. No surveys of subjective symptoms, no loss assessor visits, no claim ratio scrutiny. The trigger is objective: an accident occurred, and a defined outcome resulted.

What is Personal Accident Insurance?

Personal accident insurance is a contract between you and an IRDAI-regulated insurer under which the insurer agrees to pay pre-defined lump sums or allowances if you suffer accidental bodily injury resulting in death, disability or hospitalisation. The policy does not reimburse medical bills (that is the job of a health insurance policy) — it pays a capital sum based on the severity of the outcome, regardless of actual medical costs.

This distinction is important. If a self-employed carpenter loses his dominant hand in a table-saw accident, a health insurance policy might reimburse his surgery. But his PA policy pays him — say, 50% of the sum insured — as a one-time lump sum that he can use for home modification, retraining, EMI payments, or his children's school fees. No bill required.

Six Core Benefits Explained

1. Accidental Death Benefit

If the insured dies as a direct result of an accident, the full sum insured is paid to the nominee. There is no surrender value, no waiting period and no contestability clause. Death must occur within a policy-defined period of the accident (typically 12 months). The benefit covers road, rail, air, and workplace accidents, as well as accidental drowning, electrocution, and falls — anywhere in India and, under most policies, worldwide.

2. Permanent Total Disability (PTD)

If the accident leaves the insured permanently unable to work or perform basic activities of daily living — for example, loss of both hands, both feet, sight in both eyes, or total paralysis — 100% of the sum insured is paid. IRDAI has standardised the PTD definition, and most insurers align to the prescribed schedule.

3. Permanent Partial Disability (PPD)

Partial disability is proportional. IRDAI's schedule defines the benefit percentage for each specific loss: loss of one arm at the shoulder = 70% of sum insured; loss of one leg below knee = 50%; loss of sight in one eye = 50%; loss of one thumb = 25%; and so on. This granular benefit structure means a taxi driver who loses a finger in an accident still receives a meaningful payout reflecting the actual impact on his livelihood.

4. Temporary Total Disablement (TTD) — Weekly Benefit

If the accident temporarily prevents the insured from working — a construction worker with a broken leg, a software developer with a fractured wrist — a weekly benefit (typically 1% of sum insured per week) is paid for up to 100 weeks. This is the closest equivalent to income replacement insurance that personal accident policies offer, and it is a critically underutilised benefit.

5. Hospitalisation Daily Allowance

Many PA policies include a daily cash allowance — typically ₹500 to ₹5,000 per day — for every day spent admitted to a hospital as a direct consequence of an accident. This is distinct from health insurance's hospitalisation reimbursement: it is a flat cash payment, not a bill reimbursement, and it can be used for anything — travel expenses for family, special diet, loss of daily wages for a small trader.

6. Children Education Fund

In the event of the insured's accidental death or permanent total disability, many policies pay an education benefit for up to two dependent children. This ensures that a tragic accident does not also cut short the children's schooling — a detail that makes personal accident insurance uniquely family-centric in its design.

The Scale of India's Accident Problem

India accounts for approximately 11% of global road accident deaths despite having only 1% of the world's vehicles. The data from the Ministry of Road Transport and Highways (MoRTH) for 2023 is stark: 4.61 lakh accidents, 1,68,491 deaths, and over 4.5 lakh persons grievously injured. Beyond roads, the National Crime Records Bureau data shows lakhs of accidental deaths from falls, drowning, and fire each year.

For working-age adults — the 18–55 age group — accidents are the leading cause of unplanned financial disruption. Unlike illness, which often shows warning signs, accidents are instantaneous. A PA policy's lump-sum benefit can be arranged and paid out within 7 to 15 working days of claim submission — far faster than the months-long processing of a typical life insurance death claim.

PA Insurance vs Health Insurance vs Life Insurance

A question we frequently hear at TropoGo: "I already have a health insurance and a term plan — do I really need PA cover too?" The answer is almost always yes, and the comparison table below explains why.

Health insurance reimburses your medical bills. Life insurance pays your nominee after you die. PA insurance does something different: it compensates you — while you are still alive — for the economic impact of disability and lost earning capacity. It also pays faster and with less documentation than either alternative. The three products are complementary, not competing.

Who Should Buy Personal Accident Insurance in India?

PA insurance is relevant for almost every earning adult in India, but certain groups face disproportionately high risk:

Daily commuters — India's roads killed 461 people a day in 2023; anyone who drives, rides, or takes public transport to work has meaningful accident exposure

Self-employed and gig workers — delivery riders, auto drivers, freelancers and daily-wage workers have no employer-provided disability protection; a PA policy may be their only income safety net

Manual and industrial workers — construction workers, factory floor employees and electricians face workplace accident risks that are statistically much higher than office workers

Sports and adventure enthusiasts — skiers, cyclists, trekkers and martial arts practitioners can add a sports extension to their PA policy for activities excluded from standard cover

Frequent travellers — PA policies can be extended internationally, and many group travel policies bundle PA cover for overseas trips

Parents and family breadwinners — the children's education fund benefit and the nominee lump-sum payout make PA cover a family financial planning tool, not just a personal one

How to Choose the Right Sum Insured

The sum insured on a PA policy should reflect your annual income and your financial obligations. A common rule of thumb is to insure for 5 to 10 times your annual income, so that the PTD or accidental death benefit provides meaningful replacement. For a salaried professional earning ₹12 lakh per year, a sum insured of ₹60–₹1 crore is appropriate. For a self-employed tradesperson earning ₹4 lakh per year, a ₹20–₹40 lakh cover is a sensible starting point.

At TropoGo, our PA policies start from as little as ₹500 per year for basic cover, with premium rates rising proportionally to the sum insured and any add-on benefits selected. An individual policy for a 35-year-old with ₹50 lakh sum insured typically costs ₹3,000–₹6,000 per year — less than a monthly mobile bill for protection that could replace years of lost income.

What PA Insurance Does Not Cover

Standard personal accident policies in India exclude injuries arising from self-inflicted harm, participation in criminal activity, war or nuclear events, influence of alcohol or drugs, and pre-existing physical conditions that directly caused the accident. Some policies exclude certain high-risk occupations (mining, oil rigs, aviation crew) or charge higher premiums for these categories. Always read the policy schedule and insurer-specific exclusions before buying.

TropoGo Specialist Cover

Accidents Don't Give Warning. Your Cover Should Be Ready.

IRDAI-regulated · From ₹500/yr · Lump sum paid in 7–15 days

What is personal accident insurance and what does it cover?

Personal accident (PA) insurance pays a lump sum or defined benefit if you suffer accidental death, permanent disability, partial disability or hospitalisation. Unlike health insurance, it pays regardless of actual medical costs — a fixed benefit based on the severity of the outcome. Core covers include accidental death (100% sum insured to nominee), permanent total disability (100%), permanent partial disability (25–75%), hospitalisation daily allowance, weekly temporary disablement benefit, and a children's education fund.

How is PA insurance different from health insurance?

Health insurance reimburses hospitalisation bills (cashless or reimbursement). PA insurance pays a fixed lump sum irrespective of medical bills. PA insurance also covers disability and lost income — benefits that standard health policies do not provide. The two are complementary: health insurance pays the hospital, PA insurance replaces your income and compensates for disability.

How much sum insured should I choose for PA insurance?

A common guideline is 5–10 times your annual income. For a professional earning ₹12 lakh per year, a sum insured of ₹60 lakh to ₹1 crore is appropriate. For daily wage earners, even ₹10–₹25 lakh provides meaningful protection. TropoGo offers policies from ₹500/year for entry-level cover, scaling with sum insured and add-on benefits chosen.

Does PA insurance cover road accidents and two-wheeler accidents?

Yes. Road accidents — whether you are a car driver, two-wheeler rider, pillion passenger, cyclist or pedestrian — are covered under standard personal accident policies in India. Road accidents account for 67% of accidental fatalities in India, making this the most commonly triggered benefit. The policy covers accidents across India and, under most policies, worldwide.

How fast are PA insurance claims settled?

Personal accident claims are typically settled within 7 to 15 working days for straightforward cases where documentation is complete — including the accident report, medical certificate, and disability assessment if applicable. This is significantly faster than most health or life insurance claims, because the trigger is objective (the accident occurred and the outcome is documented) rather than requiring subjective medical review.

Can I buy PA insurance online through TropoGo?

Yes. TropoGo offers IRDAI-regulated personal accident insurance starting from ₹500 per year. You can compare plans, choose your sum insured, add optional benefits like hospitalisation allowance or children's education fund, and complete the purchase online in minutes. Get your PA cover here →

India's roads, workplaces and homes are more dangerous than most people acknowledge. A personal accident policy costing less than ₹6,000 a year can replace years of lost income, pay a disabled family member's rehabilitation costs, and ensure your children continue their education if the worst happens. It is arguably the highest-value insurance product available to working Indians — and one of the most underutilised.