When a Mumbai-based software consultancy shipped an accounting module with a date-calculation bug that wiped out a client's quarterly reconciliation, the client's loss ran to ₹1.8 crore. The consultancy had excellent technical staff, a solid delivery track record — and no Professional Indemnity insurance. The resulting legal battle took three years and cost the firm its biggest contract and, ultimately, one of its founding partners. India's services economy now generates over $340 billion annually. From Bengaluru software houses to Delhi law firms, from Hyderabad CAs to Mumbai architects — every advice-giving business carries a legal exposure that general liability cover was never designed to address. Professional Indemnity (PI) insurance, also called Errors & Omissions (E&O) insurance, exists precisely for this gap.

What is Professional Indemnity Insurance?

Professional Indemnity (PI) insurance — known as Errors & Omissions (E&O) insurance in North America — is a liability cover that protects businesses and individuals against claims arising from professional mistakes, negligent advice, errors, omissions, or failures in professional services. It is distinct from general public liability insurance, which covers physical injury or property damage caused to third parties. PI insurance covers the purely economic losses a client suffers because of something you advised, designed, coded, certified, or failed to catch.

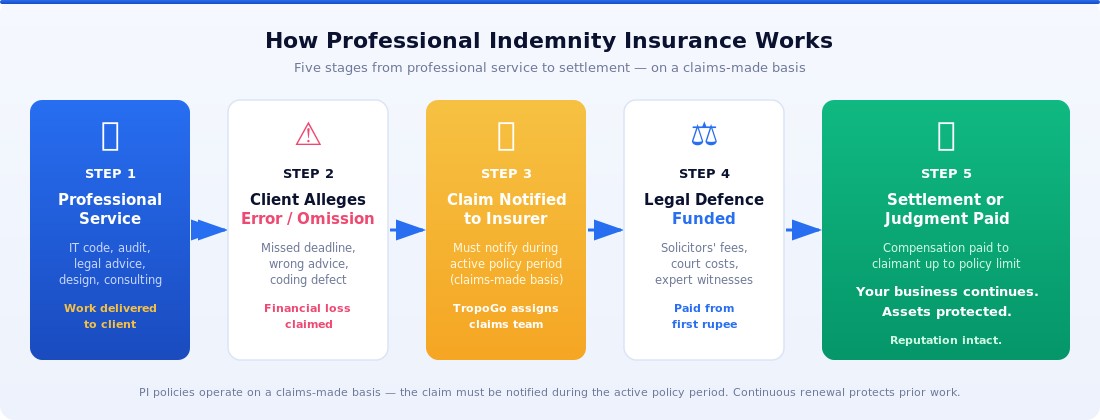

A PI claim arises when a client alleges that your professional work fell below the expected standard of care — and that the shortfall caused them a quantifiable financial loss. The policy responds in two ways: it funds your legal defence (solicitors' fees, court costs, expert witnesses) and, if the claim succeeds, pays the compensation awarded or agreed in settlement up to the policy limit.

How Professional Indemnity Insurance Works

PI policies in India are written on a claims-made basis — unlike property insurance, which covers losses that occur during the policy period, a claims-made PI policy covers claims that are made and notified during the policy period, regardless of when the underlying work was done. This distinction matters enormously: if you let a policy lapse, you can lose cover for work done years earlier. TropoGo's PI policies include a retroactive date that protects prior work as long as cover is maintained continuously.

Coverage typically includes:

Legal defence costs — solicitors' fees, barrister fees, court costs, paid from the first rupee even if the claim is ultimately dismissed

Compensation and settlements — amounts paid to the claimant if liability is established, up to the policy limit

Inquiry and disciplinary costs — ICAI disciplinary hearings, bar council proceedings, DGCA or IRDAI investigations arising from professional work

Defamation arising from professional communications — libel or slander in the course of delivering professional services

Coverage does not include fraud or intentional wrongdoing, criminal fines and penalties, bodily injury or property damage (covered by separate public liability), or claims arising from known circumstances at the time of policy inception.

Who Needs PI Insurance in India?

India's service economy spans professions where PI exposure is material and growing:

IT and Software Companies. India exports over $245 billion in software services annually. Any defect in code, data migration error, or system failure can trigger client claims running to crores — especially under SLAs with liquidated damages clauses. NASSCOM estimates that data security incidents and software failures are now among the most common sources of B2B commercial disputes in Indian IT.

Chartered Accountants and Tax Professionals. ICAI's code of conduct does not yet mandate PI cover, but the Institute's own indemnity fund acknowledges the risk. Audit mistakes, incorrect tax advice, and filing errors can expose individual CAs to multi-crore claims well in excess of their annual fee income. With the Income Tax Department's increased audit scrutiny and the Goods and Services Tax regime's complexity, errors are both more likely and more consequential.

Legal Professionals. Indian law firms face increasing malpractice claims as clients grow more sophisticated. A missed limitation period, incorrect contract drafting, or erroneous legal opinion can create liability that far exceeds the original retainer. The Consumer Protection Act 2019 confirmed that legal professionals are not exempt from its jurisdiction, opening the door to commission-forum claims.

Architects and Engineers. The Bureau of Indian Standards and state building departments create detailed design standards. An error in structural calculations or building code compliance can cause catastrophic client losses during construction — and structural failures can result in both civil claims and criminal proceedings.

Medical Professionals. Doctors, diagnostic centres, and hospitals face negligence claims under both tort law and the Consumer Protection Act 2019, which expanded the scope of medical negligence claims significantly. Claims now reach district consumer forums for amounts up to ₹1 crore, and state and national commissions for larger amounts.

Management Consultants and Financial Advisors. Strategy advice, M&A due diligence failures, and investment recommendation errors are growing sources of claims as India's corporate governance culture matures and clients become more willing to pursue professional liability in court.

Benefits of Professional Indemnity Insurance

Protects business continuity when a large claim arrives — without PI cover, a single ₹1 crore claim can threaten the survival of a mid-sized professional firm

Funds legal defence costs from the first rupee, even for claims that are ultimately dismissed

Contractually required by many enterprise clients — multinationals and listed companies routinely make PI cover a pre-condition for vendor empanelment

Signals professional accountability to clients, counterparts, and regulators

Protects personal assets of partners and directors in LLPs and partnerships where personal liability can arise

Challenges and Common Mistakes

Awareness gap: Fewer than 12% of Indian professionals carry PI cover, despite rapidly rising litigation in consumer forums and civil courts

Underinsurance: Professionals often choose policy limits based on premium cost rather than actual exposure — a ₹25 lakh limit is meaningless against a ₹2 crore SLA breach claim

Claims-made confusion: Professionals who switch insurers without maintaining the retroactive date can lose cover for years of prior work

Policy lapses: A single missed renewal can create an uncovered gap for all work done in prior years, since PI operates on a claims-made (not occurrence) basis

India's Regulatory Framework for PI Insurance

India's regulatory landscape for professional liability is evolving rapidly across four key frameworks:

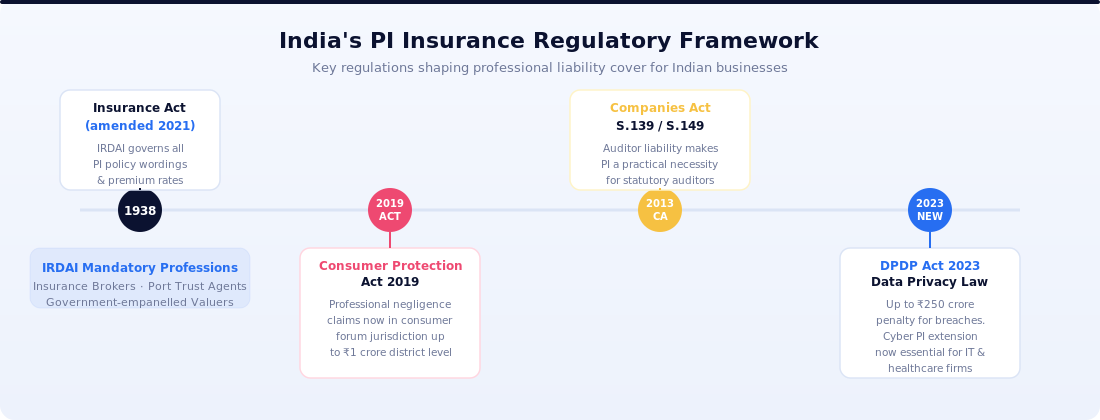

IRDAI and the Insurance Act 1938 (amended 2021). The Insurance Regulatory and Development Authority of India governs all PI policy wordings and premium rates. All PI policies must be filed with and approved by IRDAI before they can be sold. IRDAI mandates PI cover as a licence condition for insurance brokers — and similar requirements apply to certain government-empanelled valuers and port trust agents.

Consumer Protection Act 2019. This legislation dramatically expanded the scope of professional negligence claims, explicitly bringing deficiency in professional service within consumer forum jurisdiction. Claims up to ₹1 crore go to district commissions; larger claims proceed to state and national commissions. The Act's speed and low cost of filing has made consumer forum claims the preferred route for clients pursuing professional negligence in India.

Companies Act 2013 (Sections 139 and 149). Auditor liability provisions — including the concept of auditor independence and the consequences of signing off on incorrect financial statements — make PI cover a practical necessity for statutory auditors, not just a prudent option. The Ministry of Corporate Affairs' aggressive stance on audit quality means that auditors face genuine personal liability risk.

Digital Personal Data Protection Act 2023 (DPDP Act). India's first comprehensive data privacy law creates penalties of up to ₹250 crore for data breaches. IT companies, healthcare providers, and financial services firms that handle personal data as part of their professional services now face a new category of regulatory and civil liability. TropoGo's PI policies include a Cyber and Data Liability extension that covers regulatory investigation costs, notification costs, and third-party claims arising from data privacy incidents — directly aligned with the DPDP Act's requirements.

India's services economy is worth $340 billion — and growing. One uninsured PI claim can undo years of hard work.

TropoGo's PI policy is designed for the full spectrum of Indian professional services businesses — from solo CAs and boutique law firms to 500-person IT services companies. Cover includes six essential components:

Professional Negligence Cover — errors, omissions, and breaches of professional duty, including incorrect advice, defective work product, and failure to meet professional standards

Legal Defence Costs — full coverage from the first rupee, even for claims that are ultimately dismissed, including solicitors' fees, barrister fees, court costs, and expert witness fees

Cyber and Data Liability Extension — privacy breaches and data incidents arising from professional work, aligned with India's DPDP Act 2023, covering regulatory investigation costs and third-party data claims

Loss of Documents — physical and digital document loss or destruction, including client records, contracts, and professional files held in the course of business

Defamation Cover — libel and slander arising from professional communications, including reports, opinions, and advice given to clients or third parties

Retroactive Coverage — prior work protected from the agreed retroactive date, provided cover is maintained continuously, preventing uncovered gaps for earlier professional engagements

Outlook: Why PI Insurance Will Become Non-Negotiable

India's professional services sector is set to double in the next decade, driven by digital transformation, increasing sophistication of clients, and the deepening integration of Indian service providers into global supply chains. Three forces are simultaneously increasing PI exposure: the DPDP Act's data liability framework (effective from 2024 for most entities), the Consumer Protection Act's expanded and fast jurisdiction, and the growing contractual expectation from multinational clients that Indian vendors carry PI cover at defined minimum limits.

Law firms, IT companies, CAs, and architects that treat PI as an optional cost rather than a foundational operating requirement will find themselves increasingly locked out of enterprise contracts, exposed to existential claims, and at a competitive disadvantage against better-protected rivals. The question is not whether a professional mistake will happen — it is whether your business is positioned to survive when it does.

Frequently Asked Questions

What is the difference between Professional Indemnity and General Liability insurance?

General liability covers physical injury or property damage to third parties — for example, if a visitor trips and falls at your office. Professional Indemnity covers purely financial losses a client suffers because of your professional advice, work product, or failure to perform. They cover entirely different risks; many businesses need both policies running concurrently.

Which professions are required to hold PI insurance in India?

IRDAI mandates PI cover for licensed insurance brokers as a condition of their licence. Certain government-empanelled valuers and port trust agents also face mandatory requirements. Even where cover is not legally mandated — as it is not yet for IT companies, CAs, or architects — enterprise clients, particularly multinationals and listed companies, routinely make PI cover a contractual pre-condition for vendor empanelment.

What does 'claims-made' basis mean, and why does it matter?

A claims-made policy covers claims reported to the insurer during the policy period, even if the underlying work was done earlier. If you let your policy lapse, you lose cover for all prior work from the retroactive date. This is why continuous renewal and maintaining the retroactive date are critical for PI policyholders. TropoGo advisors help clients structure retroactive cover from the date their business was founded, ensuring no prior work is left unprotected.

Does PI insurance cover cyber breaches under India's DPDP Act?

Standard PI policies cover professional errors — including those that lead to a data breach as a consequence of professional negligence. TropoGo's PI policies include an optional Cyber and Data Liability extension that covers regulatory investigation costs, notification costs, and third-party claims arising from data privacy incidents, aligned with India's DPDP Act 2023 requirements for businesses handling personal data.

What policy limit should an Indian professional carry?

Policy limits should reflect the largest single contract value you handle, the maximum client loss you could theoretically cause, and any minimum limits required by client contracts. As a starting point: IT firms should carry ₹2 crore per claim and ₹4 crore aggregate as a minimum; CAs and law firms ₹1 crore per claim. TropoGo advisors can review your contract portfolio and recommend appropriate limits based on your specific professional exposure.

How do I get Professional Indemnity cover from TropoGo?

Visit TropoGo's Professional Indemnity Insurance page. Complete a short proposal form — details of your profession, annual turnover, number of professionals, and largest contract value. TropoGo's specialist team reviews your profile, provides a competitive quote, and issues a policy document digitally, with cover effective from the date of binding.

India's $340 billion services economy runs on professional expertise — and every expert can make a mistake. The businesses that will thrive are those that plan their PI cover as carefully as they plan their service delivery, because without it, one claim can cost everything.