What is Satellite Insurance? Protecting Your Space Assets

19 May 2026 | 7 min read

Protect your satellite from launch to end-of-life with India's specialist space insurer

Launch risk, in-orbit hull loss, third-party liability and pre-launch covers — satellite insurance built for Indian operators under IN-SPACe, NSIL and IRDAI frameworks.

On 23 August 2023, Chandrayaan-3’s Vikram lander touched down near the Moon’s south pole. India became the fourth country to land on the Moon — and the first to land near the pole. Within weeks, IN-SPACe had received over 80 new applications from private Indian companies seeking authorisation to operate satellites and launch vehicles. The message was clear: India’s space sector had entered a new era, and the assets at stake — satellites worth hundreds of crores of rupees — needed protecting with the same rigour as any other high-value infrastructure.

This guide explains what satellite insurance is, how it works across the full satellite lifecycle, what the Indian regulatory framework requires, and how TropoGo helps Indian operators secure the right cover.

What is satellite insurance?

Satellite insurance is a specialist class of cover that protects the financial value of a satellite and the legal liabilities its operator carries — from the moment it leaves the factory floor to the end of its operational life in orbit. Unlike standard property insurance, satellite policies must account for the extreme environment of space: launch vibration and acoustic shock, radiation degradation, micrometeorite and debris impact, and the absolute impossibility of repair once the asset is in orbit.

The global satellite insurance market handles roughly $700–800 million in annual premiums. In India, the market is at a nascent but fast-accelerating stage: the opening of the sector to private operators under the Indian Space Policy 2023 has created an entirely new class of insurable risk — domestic startups launching their own satellites on domestically developed rockets, with Indian entities carrying the insurable interest and the regulatory obligation to be covered.

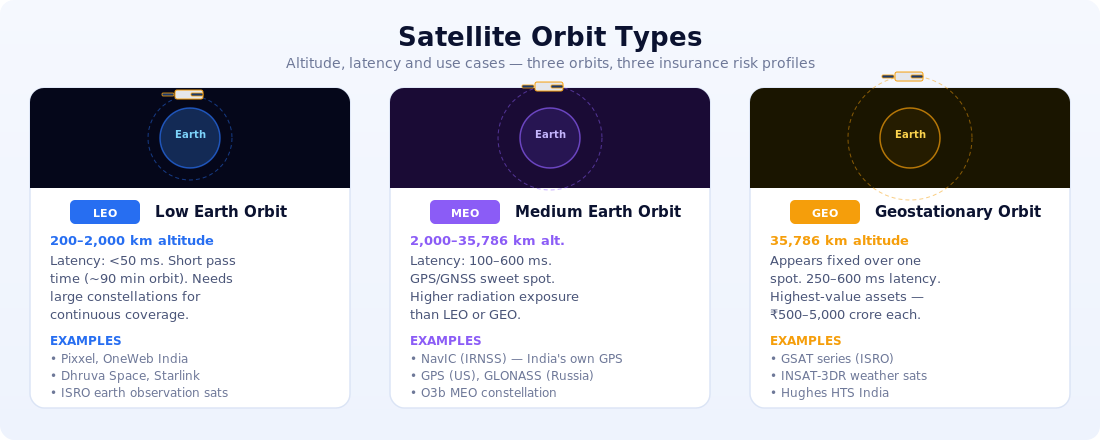

The three orbits — and why orbit determines insurance risk

The type of orbit a satellite occupies fundamentally shapes its insurance risk profile. There are three primary orbital regimes:

Low Earth Orbit (LEO) — 200 to 2,000 km altitude. This is where Earth observation satellites, remote sensing platforms and most constellations operate. Indian startups like Pixxel, GalaxEye and Dhruva Space have their assets here. LEO satellites move fast (one orbit every 90 minutes), face the highest atmospheric drag, and are most exposed to collision with orbital debris — there are over 27,000 catalogued debris objects. LEO insurance premiums have risen sharply over the past five years as constellation density increases.

Medium Earth Orbit (MEO) — 2,000 to 35,786 km altitude. Navigation satellites orbit here. India’s NavIC constellation, operated by ISRO, occupies this band. MEO assets are fewer in number, face lower debris density, but cross the Van Allen radiation belts — a significant cause of satellite component degradation.

Geostationary Orbit (GEO) — 35,786 km altitude. Communication satellites occupy a fixed position above the equator. ISRO’s GSAT series — used for broadband, television and disaster management — sits here. GEO satellites are the most expensive (₹500–2,000 crore each), have the longest designed lifespans (12–15 years), and carry the highest insured values. A GEO slot is also a finite resource: losing a satellite to an in-orbit failure means losing the slot, potentially worth as much as the satellite itself.

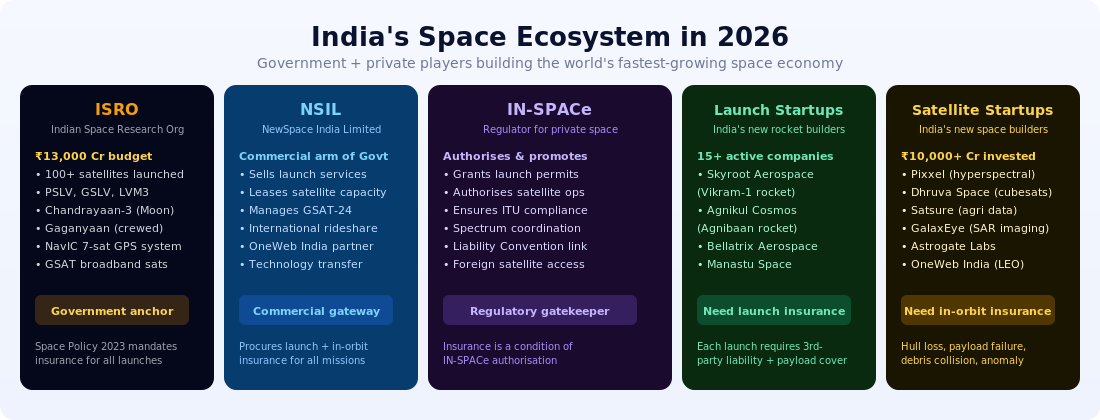

India’s space ecosystem — who needs satellite insurance?

The Indian space ecosystem has expanded dramatically since the sector was opened to private participation in 2020. The entities that need satellite insurance span the full value chain:

ISRO and NSIL are the anchor institutions. NSIL (NewSpace India Limited) is the commercial arm that handles launch services, satellite manufacturing and in-orbit leasing. Its missions — including the launch of commercial foreign satellites on PSLV and LVM3 — carry multi-hundred-crore insured values and require both launch and third-party liability cover.

IN-SPACe authorised operators are private Indian companies that have received regulatory clearance to operate satellites. Under IN-SPACe’s authorisation conditions, all operators must demonstrate adequate insurance as a precondition for receiving their operating permit. This is not optional guidance — it is a hard regulatory requirement.

Launch vehicle startups including Skyroot Aerospace (which launched Vikram-S, India’s first private rocket, in 2022) and Agnikul Cosmos (which tested AgniKul One in 2024) are developing small launch vehicles. Every launch requires third-party liability insurance to cover potential damage to third parties on the ground or in orbit.

Satellite application startups including Pixxel (hyperspectral Earth observation), GalaxEye (SAR + optical fusion), Dhruva Space (satellite platforms and launch services) and SatSure (agricultural analytics from satellite data) represent the downstream economy built on satellite data. Many of these companies have their own satellites in orbit — or will shortly — and need in-orbit coverage. See our guide to underwater drone insurance for how specialist insurance is similarly essential for India’s marine technology sector.

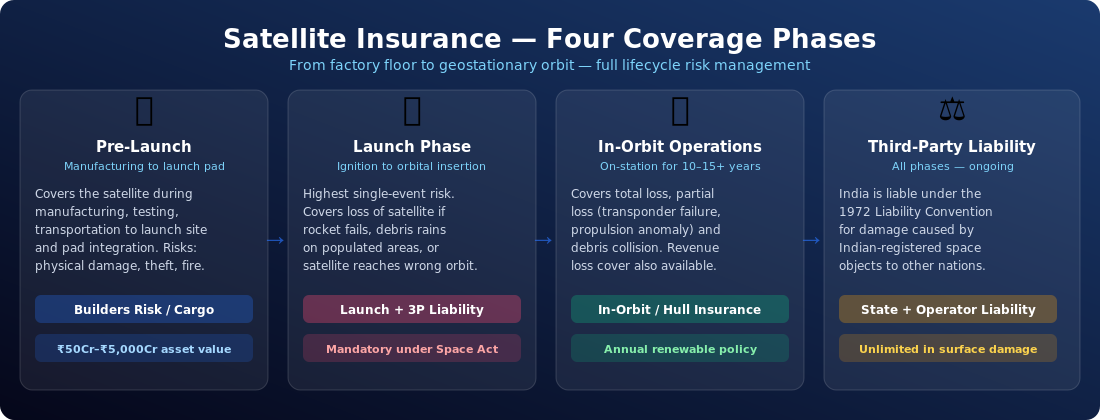

The four phases of satellite insurance

ROVs, AUVs and USVs — India's underwater tech for oil, gas, defence and port surveys.

Phase 1 — Pre-launch (terrestrial risk). Before the satellite reaches the launch pad, it sits in a manufacturing facility and integration hall. Pre-launch insurance covers the satellite against fire, flood, earthquake, theft, accidental damage during transport, and handling errors during integration. This phase can last 18–36 months for a complex satellite. Premiums are relatively modest — typically 0.5–1.5% of the satellite’s value per annum — because the risks are well-understood conventional property risks.

Phase 2 — Launch insurance. The highest-risk moment in a satellite’s life is the 10–15 minutes of launch. Launch insurance covers total or partial loss during launch and the early orbit phase (typically the first 180 days after separation). “Total loss” means the satellite is destroyed or stranded in an unusable orbit. “Partial loss” covers scenarios where the satellite reaches orbit but with degraded capability — e.g., a solar panel that fails to deploy fully, reducing power and therefore operational life. Launch insurance premiums range from 5–15% of the satellite’s insured value, depending on the launch vehicle’s track record.

Phase 3 — In-orbit insurance. Once the satellite is operational, in-orbit insurance covers it against on-orbit failure from any cause: component failure, software anomaly, debris impact, fuel depletion, attitude control loss and end-of-life anomalies. Premiums are typically 1.5–4% of the satellite’s insured value per annum, rising as the satellite ages. A satellite with five years of remaining life commands a lower premium than one in the final year before planned decommissioning.

Phase 4 — Third-party liability. Under the 1972 Convention on International Liability for Damage Caused by Space Objects, the “launching state” (India) bears absolute liability for damage caused by its space objects on Earth’s surface or in flight. For damage caused in orbit, liability applies where the launching state is at fault. India’s Space Policy 2023 passes this liability through to private operators via IN-SPACe: every authorised operator must hold third-party liability cover. This protects against scenarios such as satellite debris striking another operator’s satellite in orbit, or a re-entering satellite fragment causing ground damage.

What satellite insurance covers — the six key lines

Pre-launch property all-risks — manufacturing facility, integration hall, transport and pad damage prior to liftoff.

Launch and early orbit (LEOP) insurance — total or partial loss during launch vehicle flight and the critical early orbit phase.

In-orbit hull all-risks — on-orbit failure from any cause, including debris collision, component anomaly and solar storm damage.

Third-party liability — damage caused by the satellite (or its debris) to third parties on the ground or in orbit, satisfying India’s obligations under the 1972 Convention and IN-SPACe authorisation conditions.

Loss of revenue / business interruption — compensation for lost commercial revenue during a period when the satellite is unable to provide its contracted services due to a covered in-orbit event.

Anomaly investigation costs — engineering and legal costs incurred in investigating an in-orbit anomaly, even where the anomaly does not result in a total or partial loss claim.

Need satellite insurance for your Indian space mission?

TropoGo works with Lloyd’s syndicates, IRDAI-registered carriers and IN-SPACe-aware brokers to structure cover across all four mission phases.

Why insurance is the foundation of any space mission

In the terrestrial economy, insurance is something businesses buy after they have started operating. In the space economy, insurance is a precondition for operating at all. No Indian bank will finance a ₹200 crore satellite manufacturing programme without evidence of pre-launch insurance. No IN-SPACe authorisation will be granted without third-party liability cover. No international launch provider will accept a payload without proof of insurance. And no B2B customer will sign a multi-year satellite data contract with a startup that cannot demonstrate financial resilience in the event of an on-orbit anomaly.

TropoGo’s satellite insurance solutions are structured around the four phases above, with policies that can be placed on a phase-by-phase basis or as an integrated programme covering the full lifecycle. Key underwriting considerations include: satellite manufacturer track record, launch vehicle heritage, orbit and mission type, satellite age and technology generation, propellant reserves and manoeuvring capability, and alignment with IN-SPACe’s insurance mandates.

India’s satellite insurance regulatory framework

IN-SPACe is the single-window regulator for private space activities. Its authorisation framework requires all private satellite and launch operators to hold insurance as a condition of their operating permit, with minimum liability cover levels set on a mission-by-mission basis.

IRDAI governs the Indian insurance market. Under its speciality risk framework, Indian-registered carriers can lead or participate as co-insurers on satellite risk. In practice, most large Indian satellite programmes are placed with Lloyd’s of London syndicates with dedicated space underwriting desks, with Indian carriers co-insuring to meet IRDAI’s localisation objectives.

Department of Space / MoCA oversees India’s obligations under the four UN Space Treaties. The 1972 Liability Convention is the most commercially significant: it creates absolute state liability for surface damage and fault-based liability for in-orbit damage, and directly drives the third-party liability insurance requirement for all IN-SPACe authorised operators.

The outlook for Indian satellite insurance

The global space insurance market is projected to grow from $8.4 billion in 2024 to $44 billion by 2033, driven primarily by commercial LEO activity. India is expected to account for a growing share as its domestic industry matures. The government’s target of increasing India’s share of the global space economy from 2% to 10% by 2030 implies a five-fold expansion — every new IN-SPACe authorisation is a new insurable interest and a new liability obligation.

Is satellite insurance mandatory in India?

Yes. The Indian Space Policy 2023 and IN-SPACe’s authorisation conditions require all private launch operators and satellite operators to hold third-party liability insurance as a condition of their operating permit. NSIL requires launch insurance for all missions it handles commercially. While specific minimum limits are set by IN-SPACe on a mission-by-mission basis, the principle that every launch must be insured is firmly established in Indian space law.

What does launch insurance cover?

Launch insurance covers the total or partial loss of a satellite if the launch vehicle fails to deliver it to the intended orbit. “Total loss” means the satellite is destroyed or reaches an orbit from which it cannot be recovered. “Partial loss” means the satellite reaches orbit but is damaged or reaches an anomalous orbit that reduces its useful life. Third-party liability within the launch policy covers debris damage to third parties on the ground or in the air.

How is satellite insurance priced?

Premiums are calculated as a percentage of the insured value. Launch insurance typically costs 5–15% of the satellite’s value depending on the launch vehicle’s track record. In-orbit insurance costs 1.5–4% per annum, rising with satellite age. Key pricing factors include launch vehicle heritage, satellite manufacturer track record, orbit type, satellite age, remaining propellant, technology generation and coverage limits.

What is the 1972 Liability Convention and how does it affect Indian operators?

The 1972 Convention on International Liability for Damage Caused by Space Objects makes the launching state (India) absolutely liable for damage caused by its space objects on Earth’s surface or to aircraft in flight. For in-orbit damage, liability applies where the launching state is at fault. India’s Space Policy 2023 passes this liability to private operators via IN-SPACe — meaning private Indian space companies must hold insurance that backstops India’s international treaty obligations.

Can Indian insurance companies underwrite satellite risk?

Yes, with co-insurance and reinsurance support. IRDAI’s speciality risk framework allows Indian carriers to lead or co-insure space missions. In practice, most large Indian satellite programmes are placed with Lloyd’s of London syndicates that have specialist space underwriting teams, with Indian carriers participating as co-insurers. TropoGo acts as the specialist broker coordinating Indian and international capacity for Indian operators.

Does satellite insurance cover debris collisions?

In-orbit insurance typically covers debris collision as a cause of loss — if a catalogued or uncatalogued debris object strikes the satellite, the resulting damage or total loss is covered under the all-risk in-orbit policy. Third-party liability insurance covers the situation where debris from your satellite damages another operator’s asset. With over 27,000 catalogued debris objects in orbit, collision risk is one of the fastest-growing concerns in space underwriting. TropoGo’s satellite insurance covers both sides of this risk.

India’s space sector is at an inflection point. The companies that succeed will be those that plan their insurance as carefully as they plan their orbital mechanics — because without cover, no bank will finance the satellite, no IN-SPACe authorisation will be granted, and no mission can proceed.